Zeta earnings recap Q4 2025

Zeta just reported their 18th consecutive beat and raise quarter. This is their Q4 2025 earnings breakdown.

Zeta crossed a great milestone this quarter: they became profitable on a GAAP basis in Q4, with operating leverage kicking in. Management is now guiding to GAAP net income positive for FY 2026, which I think also changes how the market perceives this name.

1 - Key numbers

- Q4 revenue: $395M, up 25% YoY

- Q4 revenue ex political candidate, LiveIntent, and Marigold Enterprise Business: up 28% YoY

- Q4 GAAP net income: $6.5M, 1.7% margin

- Q4 free cash flow: $55.8M, up 76% YoY, 14.2% margin

Other core metrics

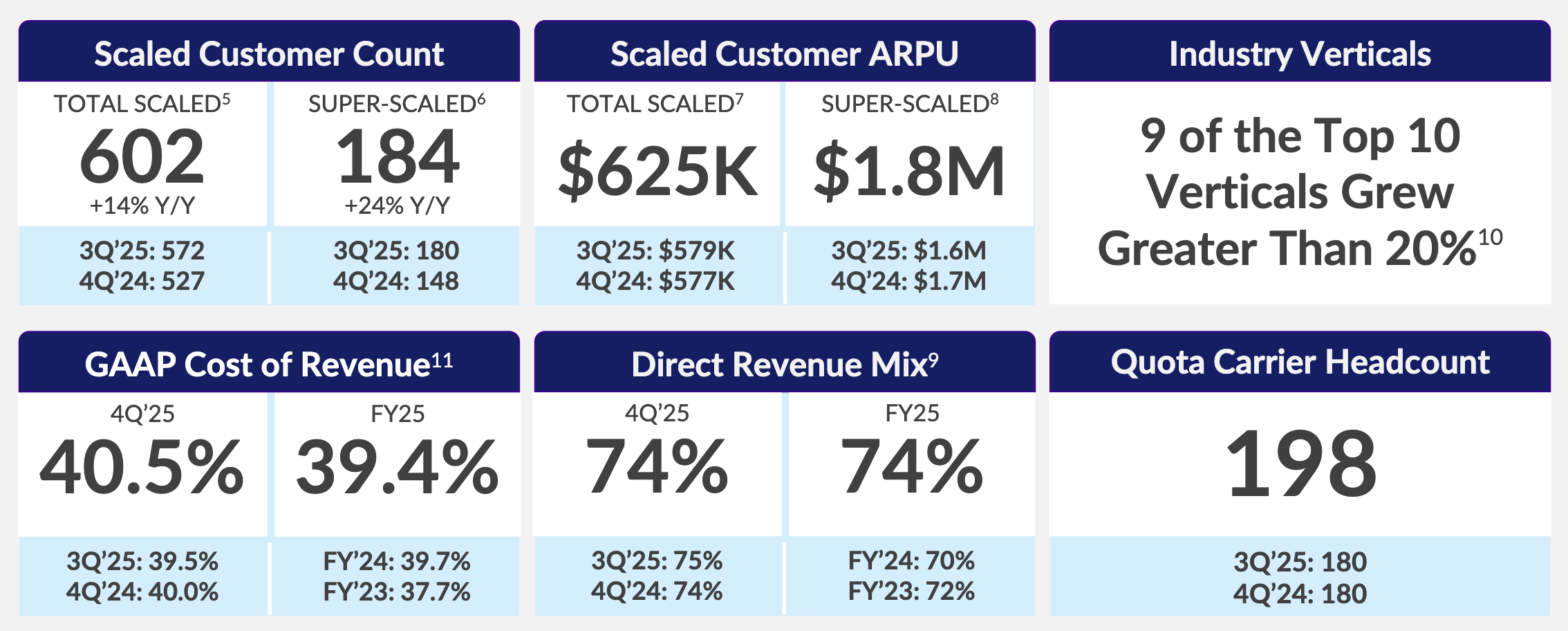

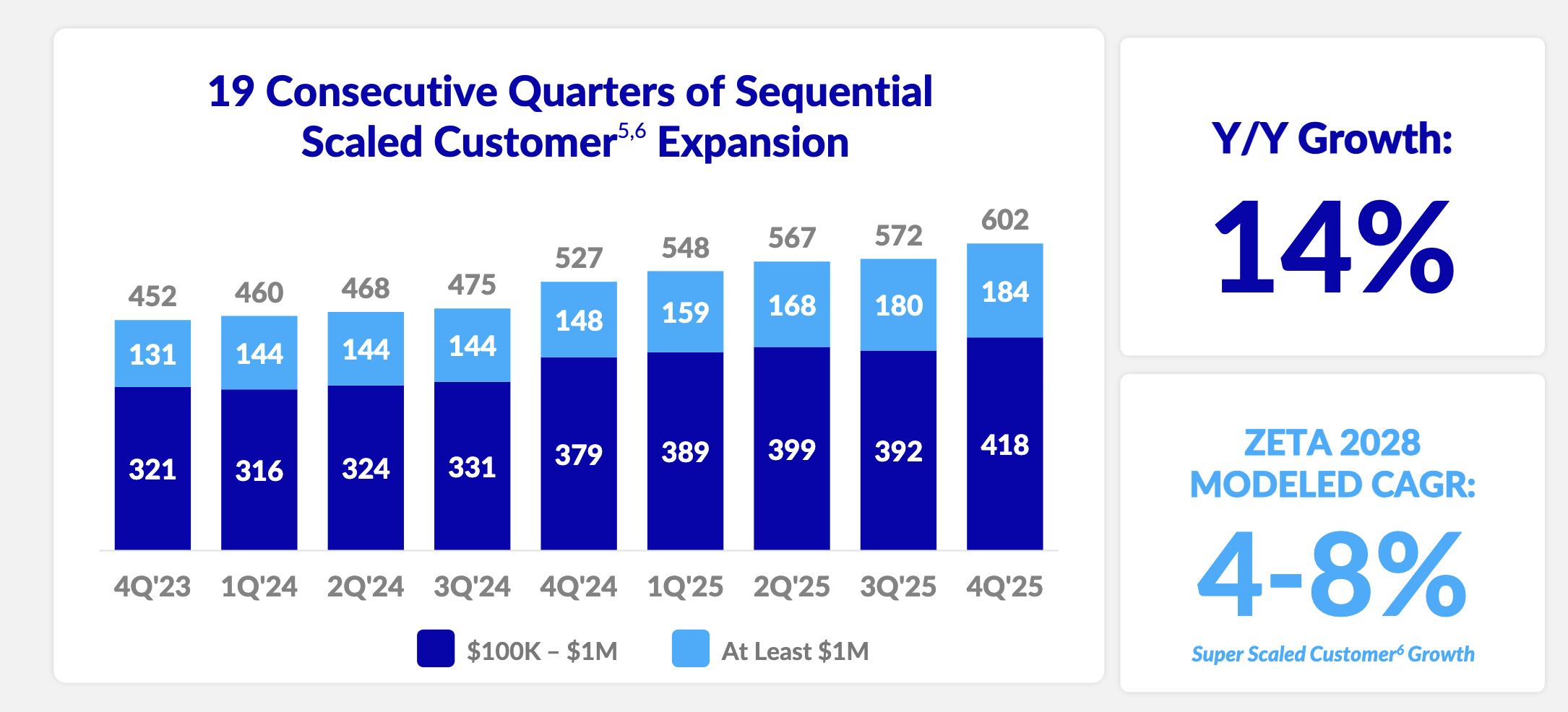

- Scaled customers: 602, up 14% YoY

- Super scaled customers: 184, up 24% YoY

- Net revenue retention: 120% in 2025, up from 114% in 2024

2 - Guidance

Q1 2026 outlook

- Q1 2026 revenue: $369M to $371M

- Q1 2026 adjusted EBITDA: $61.2M to $61.8M

Fiscal year 2026 outlook

- FY 2026 revenue: $1,749M to $1,762M

- FY 2026 adjusted EBITDA: $389.9M to $392.1M

- FY 2026 free cash flow: $230.7M to $231.7M

- FY 2026: guiding to positive GAAP net income

What is baked into these guides:

- Political candidate revenue assumed at $15M in 2026, with $7M in Q3 and $8M in Q4

- Marigold Enterprise Business assumed to contribute at least $190M in 2026 revenue

- Minimal contribution from Athena driven revenue in the 2026 guide

2028 outlook

- Revenue target: $2.3B+

- Adjusted EBITDA target: $573M+

- Zeta 2028 free cash flow target: $371M+

3 - Business highlights

Zeta continues to emphasize their land and expand motion and management gave a few signals that expansion is improving. The clearest one was that the number of scaled customers using more than one use case was up over 80% year over year, which is a great to see because it shows their land and expand strategy is working.

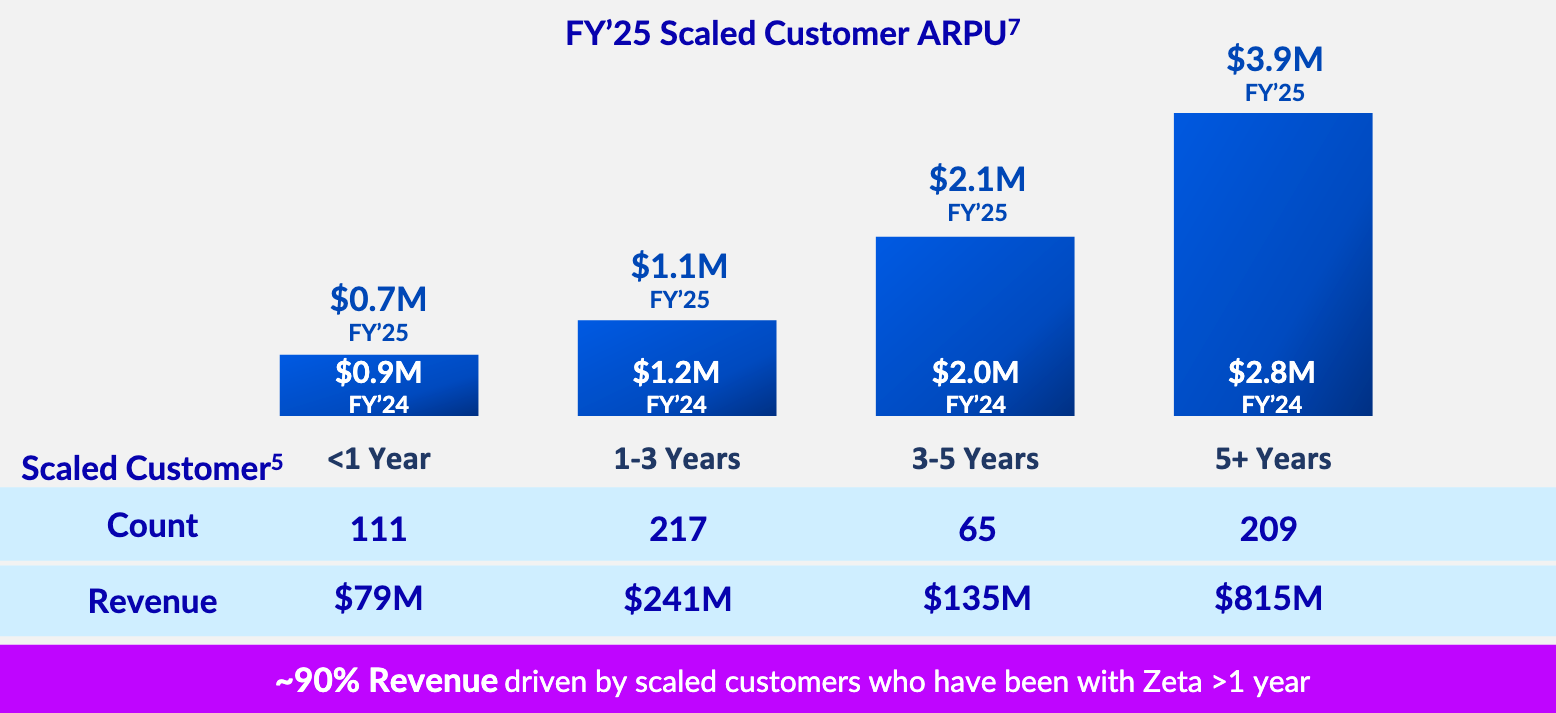

Customers get bigger with time and deeper integration. It also shows in their super scaled customers. Management said customers spending at least $1M annually represented about 70% of revenue in 2020 and are now approaching 90% in 2025.

💡

Zeta on reporting key business metrics: Starting in 2026 they will “exclusively focus quarterly reporting on super scaled customer count and ARPU."

Some of the fastest growing business verticals Zeta called out in their Q4 earnings call:

- Travel and hospitality +105%

- Advertising and marketing +70%

- Automotive +60%

- Consumer and retail +46%.

The Marigold acquisition

CEO and co-founder Steinberg: "The integration is progressing well,” and reiterated that Marigold is expected to be “accretive to free cash flow and adjusted EBITDA in year one.”

Data & Identity

Zeta’s advantage lies in deterministic identity and proprietary data. Steinberg described SuperGraph as “a proprietary, deterministic, identity and relationship graph,” and tied it to why Zeta benefits as personalization moves toward true one to one. The Marigold acquisitions further expands the total dataset Zeta owns which in turn increases value for their customers. And the longer customers stay, the more they spend:

4 - Management commentary

Steinberg on their 18th consecutive beat and raise:

We delivered our eighteenth consecutive beat and raise quarter, and I want to be clear about why this keeps happening. It is not a single product cycle or a favorable compare. It is the compounding effect of a system, proprietary data that improves with every customer interaction, intelligence that sharpens with every decision, and now an interface in Athena that lowers the barriers to enterprise wide adoption

On AI and LLM's:

We view large language models, much like cloud infrastructure, foundational technologies that enable innovation, with real differentiation coming from the tools, workflows, data, and operating systems built on top. Powerful models are only part of the equation. AI is only as effective as the data that fuels it. As personalization moves to true one to one, identity and intent become critical.

Zeta operates across more than 245 million U.S. adults and 535 million globally, with more than 1 trillion signals, the vast majority of which are available only to Zeta.

CFO Chris Greiner on FY 2025:

For the full year 2025, we expanded adjusted EBITDA margins by over 200 basis points, achieved the highest free cash flow margin in our history, generated $199 million in net cash provided by operating activities, and turned GAAP net income positive in Q4, demonstrating the profitability of our growth.

On guidance and Marigold contribution:

Strong pipeline visibility and sales productivity support our confidence in the year ahead, and we continue to guide with planned conservatism of 2% to 5%. Lastly, as we integrate Marigold, we expect to realize further operating leverage.

Additionally, we continue to take a conservative view of Marigold, contributing at least $190 million in 2026 revenue. Lastly, our revenue guidance includes minimal contribution from Athena driven revenue, with its broad based adoption representing incremental consumption revenue upside

Management is known to really sandbag their guidance which also shows in their remarks about conservative guides. They will most likely grow revenue north of 30% for the next few years, even though their 2028 outlook implies 23% growth.

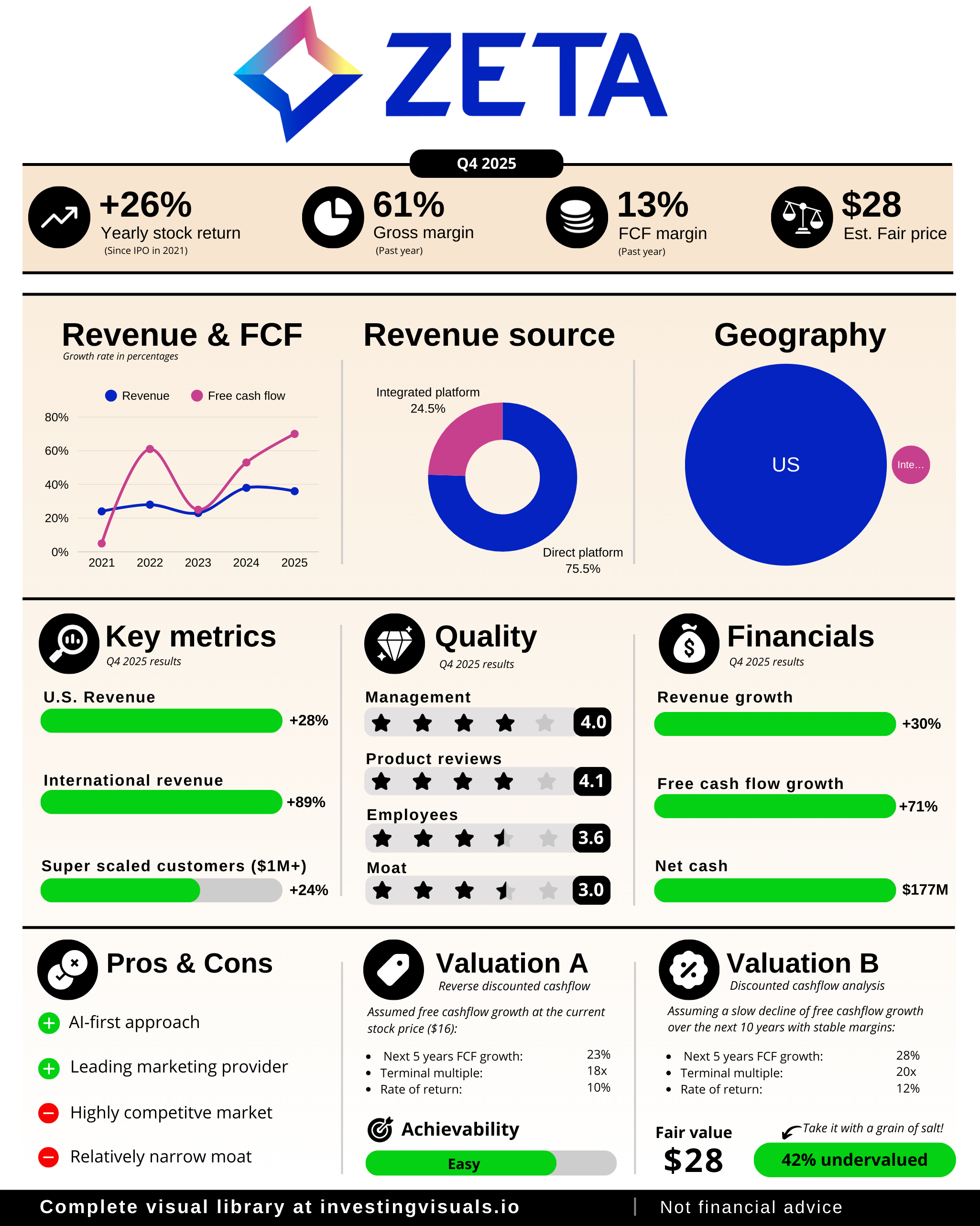

5 - Q4 visualized

My take

What stood out for Zeta in this quarter was the combination of growth, margin expansion, and cash generation. The business also reached positive GAAP net income in Q4, and management is guiding to positive GAAP net income for the full year 2026 which is great to see.

The customer mix continued to shift toward larger, more embedded relationships with super scaled customers growing to 184 (+24%). Net revenue retention improved to 120% in 2025 which is a great sign that existing customers are expanding their usage of Zeta's platform.

Zeta's execution was great this quarter and operating leverage clearly kicked in. Growth is strong, their balance sheet is in good shape and customers continue to spend incrementally more dollars on their platform. But it's also important to keep a close eye on the road ahead and potentials risks along the way.

What to watch from here:

- Whether super scaled customer count and ARPU, which management will focus on going forward, continue to move up together

- Evidence that Athena adoption increases multi use case usage and consumption driven expansion

- The Marigold integration and cross selling into the existing Zeta customer base

- If net revenue retention remains strong, preferable between 115% - 120%

All in all: Zeta posted a very good quarter!

As always, none of this is financial advice. This is simply my breakdown of this quarter and my thoughts about it. Always do your own due diligence before making an investment decision that fits your own risk tolerance and time horizon.

Written by

Sign-up

Get the latest updates and news in your inbox

Member discussion