ServiceNow earnings review: what moved the stock

This was a mixed quarter for ServiceNow, but it wasn't about the quarter itself as much as the broader picture; a shift in the dynamics of SaaS. What the market was looking for was a clear signal that AI is a tailwind to enterprise software and it didn't get that. At least not to the extend the market was expecting. Instead, it got declining margins and a slight revenue acceleration. But does that warrant a 17% stock drop?

1. What ServiceNow Does

ServiceNow is an enterprise software platform that automates and orchestrates workflows across IT, HR, security, customer service, and increasingly, AI agents. Think of it as the operating system for how large companies get things done internally. They make money primarily through subscription contracts, and the stickiness of the platform is exceptional: once a company builds its core processes on ServiceNow, ripping it out is very hard.

2. Key Numbers

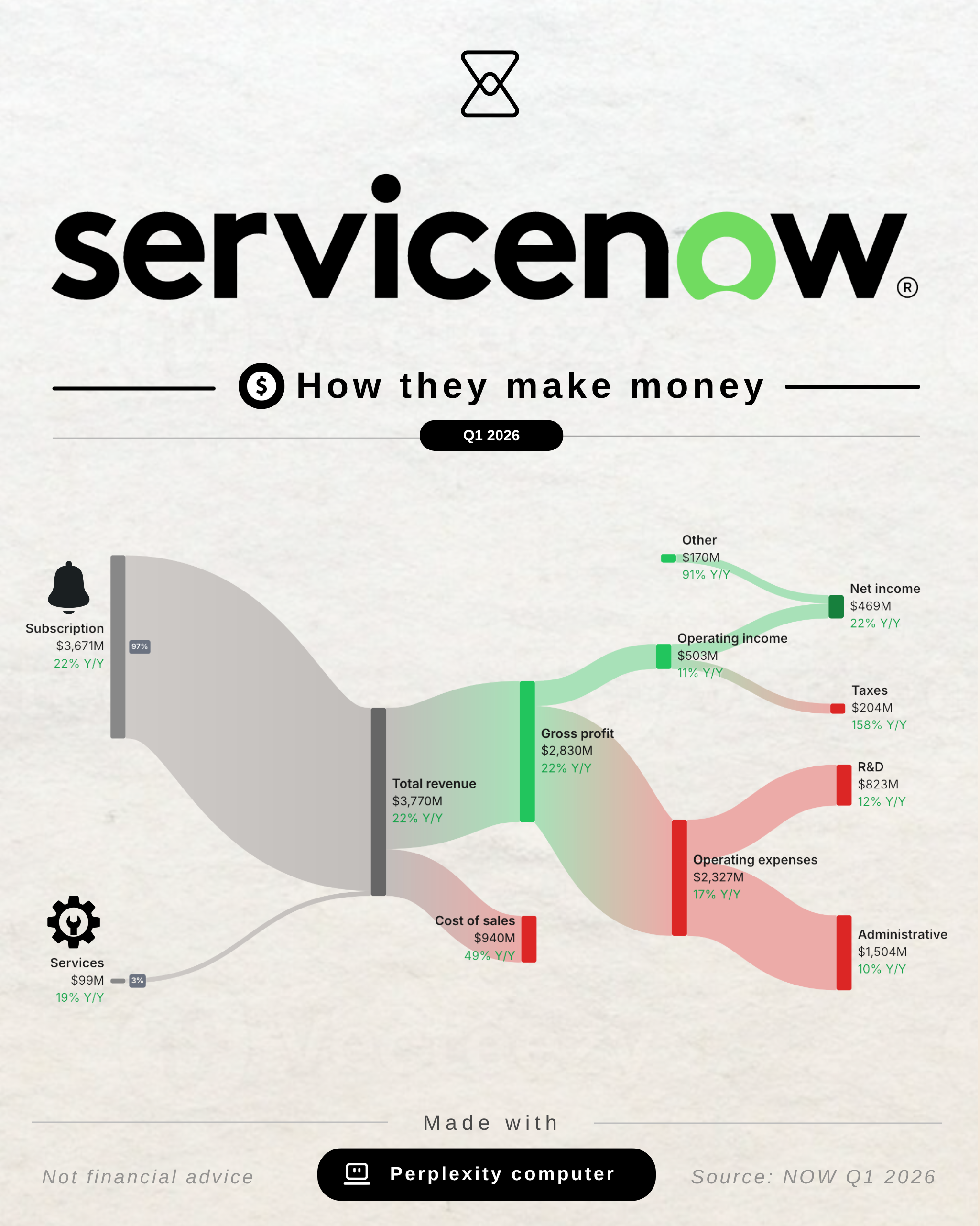

Q1 2026 Results

- Subscription revenues: $3.671B, up 22% year over year; 19% in constant currency (cc) above the high end of guidance

- cRPO (current remaining performance obligations, the best forward-looking demand signal): $12.64B, up 22.5% reported, 21% cc, beating guidance by 100 basis points

- RPO (total backlog): $27.7B, up 25% year over year

- Non-GAAP operating margin: 32%, 50 basis points above guidance

- Non-GAAP free cash flow margin: 44%

- Renewal rate: 97%, down from 98% the prior year

- Customers generating over $5M in annual contract value: 630, up 22% year over year

- 16 deals greater than $5M in net new ACV; 5 deals greater than $10M

- New logo ACV growth: over 50% year over year, including largest new logo ever at over $15M

Full Year 2026 Guidance (updated)

- Subscription revenues: $15.735B to $15.775B, representing 20.5% to 21% cc growth; includes 125 basis points contribution from Armis

- Non-GAAP subscription gross margin: 81.5% (down from prior 82.0% guide)

- Non-GAAP operating margin: 31.5% (down from prior 32.0% guide)

- Non-GAAP free cash flow margin: 35% (down from prior 36% guide)

3. Outlook

Q2 2026 guidance

- Subscription revenues: $3.815B to $3.820B, 21% to 21.5% cc growth

- cRPO growth: 19.5% cc

- Non-GAAP operating margin: 26.5%, a 300 basis point year-over-year step-down, primarily from Armis integration costs

Strip out the Armis contribution (roughly 125 basis points) and apply a normal 100 basis point beat, and Q2 subscription revenue growth implies approximately 19.75% to 20.25% cc on an organic basis. That's a modest acceleration from Q1's 18% organic print. Nothing dramatic, but directionally it moves the right way. It would be a lot worse if NOW materially decelerated.

The cRPO picture here is important. Strip Armis (125 basis points) and apply the usual cushion, and organic cRPO growth in Q2 guidance implies roughly 18.3% cc. That's softer than Q1's organic cRPO of approximately 20% cc, which reinforces why the market didn't cheering for this quarter.

Another interesting signal is what management said qualitatively. Gina Mastantuono: "We will lay out our long-range plan and when we expect to see that flywheel of AI consumption." Bill McDermott committed to showing revenue acceleration, margin expansion, and SBC reduction at the May 4th Financial Analyst Day. "We are going to show you just how big this company is going to be in the next few years."

My take: great promises, now deliver on them. They have been bullish on AI for a while but the revenue needle hasn't moved materially. It moved, just not by a lot (yet).

4. Business highlights

Seat-based vs. usage-based: a structural shift

One of the most important strategic data point this quarter wasn't the revenue number. It was this: 50% of net new ACV is now coming from non-seat-based pricing, including consumption tokens, infrastructure, hardware, and connectors. NOW is in the middle of repricing itself from a seat-based company to a usage based model. However; margins took a hit because of it. And I think that's an important reason for the sell-off; the high margin profile of SaaS businesses is on the line; costs for a usage based model are higher vs a seat-based model. You can already see that in the cost of sales numbers, which is up +40% YoY.

The positive side of a usage based model is that it moves the ceiling higher; seat-based software scales with employee count. Usage-based software scales with how much work gets done. As AI agents start resolving tens of thousands of tickets autonomously, the number of "seats" becomes less relevant.

AI revenue: aspirational, but grounded

Now Assist is on a trajectory to exceed $1B in ARR this year. McDermott noted $1.5B "is on the table" for 2026.

I would treat it as an upper-case scenario. If they hit it, that implies roughly 10% of the business will be AI token-derived by year-end, growing approximately 150% year over year. That would be, at least in my view, be a material inflection in the story.

Some supportive figures: Q1 saw deals including three or more Now Assist products grow nearly 70% year over year. Thirty-six deals included five or more AI products.

Moveworks integration

Moveworks was integrated into ServiceNow's EmployeeCenter Pro in under three weeks, relaunched as EmployeeWorks in February, and in Q1 alone closed more seven-figure deals than it had in all of the prior year.

Sales CRM

Sales CRM net new ACV grew more than 5x year over year in Q1, with deal count up over 80%. This is a product category where ServiceNow is directly attacking Salesforce's installed base with an AI-native alternative. Legacy CRM was described as: "A category promising a 360-degree view of the customer has left most enterprises spinning in circles."

5. Management commentary

On the Middle East headwind

The 75 basis point Q1 revenue drag from delayed on-premise deals in the Middle East was acknowledged. McDermott: "We just beat and raised. It was a beat and raise, not an excuse." Mastantuono confirmed the full year guidance was not reduced for any potential geopolitical conflict, and the impacted deals are expected to close.

On SBC and shareholder alignment

Management brought up stock-based compensation multiple times during the call. McDermott: "Were taking down SBC because we want to get it down into single digits because we can." The ratio did improve slightly, from 15.2% to 14.8% year over year. But absolute SBC grew 19% year over year to $558M in Q1, up from $470M. Based on management commentary, this should come down.

On the acceleration question

Keith Weiss from Morgan Stanley highlighted the elephant in the room: AI labs are each adding $5B in net new ARR per quarter while ServiceNow is discussing $1.5B for the full year. McDermott: "Get ready for major revenue acceleration." Same as before; bold words, now show it.

6. Margins: why they compressed

First, the migration from owned data centers to hyperscaler-hosted infrastructure. This is a deliberate strategic choice: more flexibility, better global reach, faster AI compute access. But it shifts fixed cost to variable cost and compresses near-term gross margin in the process. It's worth noting that management is treating it as a transition cost.

Second, the ramp of AI workloads. Running inference at scale costs money. As token consumption grows and AI becomes a larger share of the revenue mix, the compute cost embedded in the gross margin line grows with it. And this is exactly the crux; the business model of SaaS is changing and it's uncertain what the margin profile will look like exactly. I believe it's this uncertainty that the market is currently pricing and is one of the main reasons for the sell-off.

7. Acquisition integration

Armis

The revenue contribution of Armis deserves a closer look. The guidance implies approximately 125 basis points of subscription revenue contribution from Armis to the full year.

That's roughly $161M in revenue assumed for 2026, which sits significantly below what one would extrapolate from the December 2025 deal announcement describing Armis as a $340M ARR business growing 50% per year.

Mastantuono acknowledged that her approach to guiding for new acquisitions is "prudent" and that the financial assumptions are sandbagged. She also noted that Armis contracts contain termination-for-convenience provisions, which limits how much revenue can flow into recognized and contracted metrics in the near term.

The revenue contribution from Armis is likely to be meaningfully higher than guided, and the burn rate lower than the implied $325M annually. But it's an important part to watch because they have paid a hefty price for Armis.

8. My take

A valid concern here is that the organic growth rate has been decelerating for four consecutive quarters, moving from the 19.5% to 21.5% cc range last year to approximately 18% organic in Q1. Management's explanation includes legitimate one-timers, the Middle East conflict, the self-hosting-to-hosted transition (which oddly wasn't mentioned this quarter after being flagged last quarter), and M&A timing. Strip those out and you get to roughly 18.75% to 20.25% organic. That's not acceleration, period.

On top of that, margins are contracting due to the shift from seat-based to usage-based and it's unclear what the margin profile will look like exactly.

Then again; transitions like this take time and don't happen overnight. It was a good quarter overall, the AI offerings are scaling and might become ~10% of revenue by the years end. If it does, the stock will likely re-rate and shrug off the AI disruption discount.

So does this all warrant 17% drop? In my opinion it's overdone. But software is in a rough spot right now. I do believe the risk/rewards is attractive here and a lot of downside is priced in. A clear acceleration in the business from here will probably take the stock materially higher. But NOW has to deliver on their promise. Walk the talk.

The analyst day on May 4th is important because the long-range plan they present will set the terms of the debate for the next 12 to 18 months. If the targets are credible and the AI monetization roadmap is clear, the stock could pop. If the targets look like a continuation of the current trajectory with more acquired revenue layered on top, the picture isn't that pretty.

What to watch

- Q2 organic subscription revenue growth rate, adjusted for Armis and Moveworks, to see whether the acceleration management promised actually arrives in the numbers

- The Now Assist ARR trajectory toward the $1.5B aspirational target, with particular focus on renewal and expansion rates within AI-adopting customers

- Armis actual revenue contribution versus the conservative guidance, and whether the burn rate comes in below the implied $325M annually

- Gross retention rate in subsequent quarters; the tick from 98% to 97% is not alarming yet, but it needs watching, especially as AI alternatives proliferate

- SBC in absolute dollar terms; the ratio is improving but the dollar amount needs to flatten and ultimately decline as the acquisition retention grants roll off

That's it for now. Thank you for reading & I hope you found it helpful!

~ Jan

As always, none of this is financial advice. This is simply my breakdown of the quarter and my thoughts on it. Always do your own due diligence before making an investment decision that fits your risk tolerance and time horizon.

Written by

Sign-up

A weekly newsletter for visual learners to help you invest better

Member discussion