ServiceNow earnings recap

ServiceNow beat Q4 expectations and guided FY 2026 subscription revenue above consensus, but the stock still traded down about 10% after hours. Is that justified, or might this be a great opportunity to buy?

First things first. The key numbers.

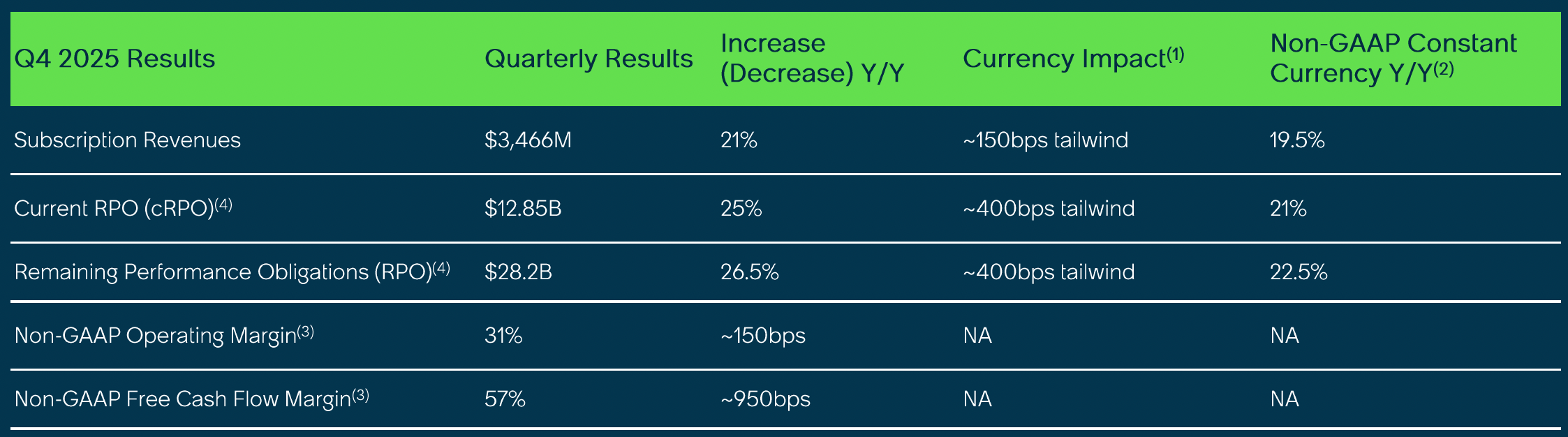

1 - Key numbers

- Total revenue was $3.568B vs $3.53B expected (beat)

- Adjusted EPS was $0.92 vs $0.88 expected (beat)

- Subscription revenue was $3.466B, up 21% year over year

- cRPO was $12.85B, up 25% year over year

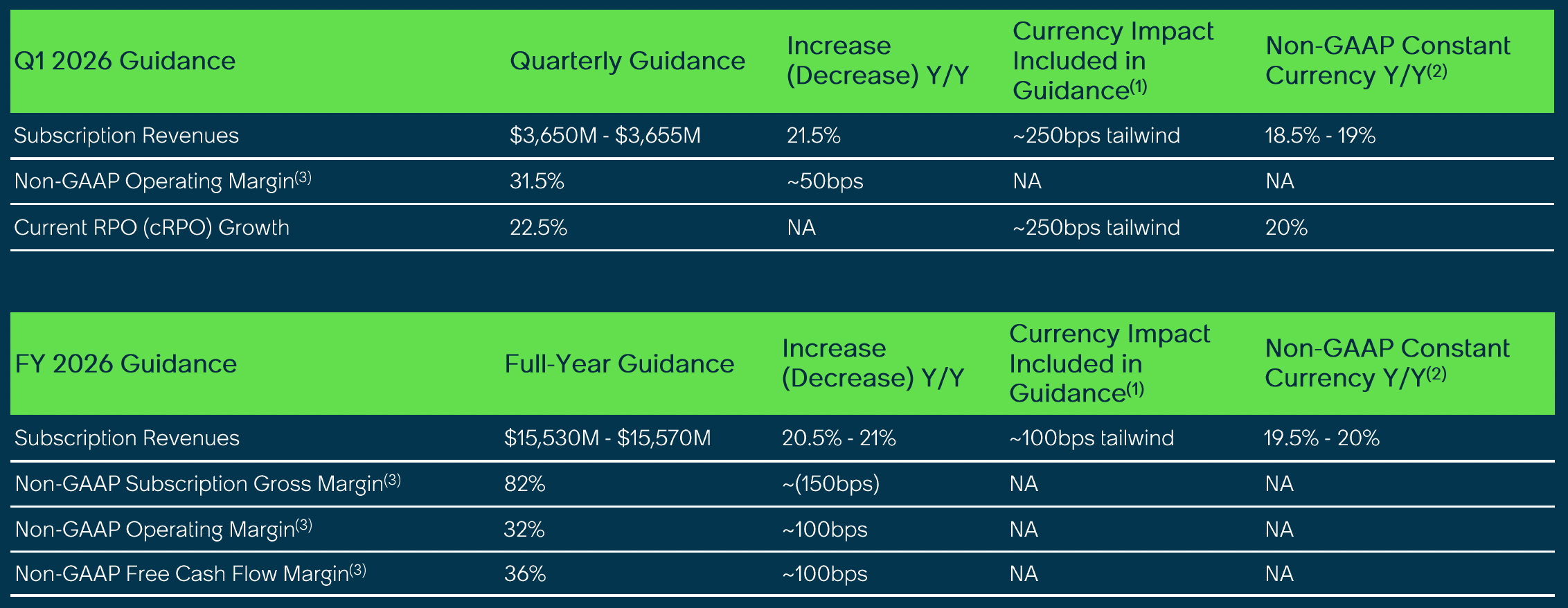

Outlook vs expectation

Q1 subscription revenue guide was $3.650B to $3.655B vs $3.57B expected. FY 2026 subscription revenue guide was $15.53B to $15.57B versus $15.21B expected.

All in all, a double beat and a guidance raise. So why did the stock drop after hours? I read this as a high bar setup. Investors wanted a bigger upside surprise, likely driven by clearer AI upsell impact, while also worrying about acquisitions and the broader software tape.

2 - ServiceNow AI nuggets

Let’s start with a quote from CEO Bill McDermott on AI: "AI doesn’t replace enterprise orchestration. It depends on it."

ServiceNow’s main AI product suite is Now Assist. It layers generative AI and agent style capabilities on top of ServiceNow workflows. The goal is to help users draft, summarize, classify, route, and resolve work inside the Now Platform. Faster ticket resolution, better self service and more automation for common tasks. Some important highlights:

- Now Assist surpassed $600M in ACV 1

- Now Assist net new ACV in Q4 2025 was more than 2x year over year

- 35 deals over $1M in Q4 tied to Now Assist net new ACV

- AI Control Tower 2 deal volume nearly tripled quarter over quarter

💡

1 ACV is short for annual Contract Value, which is the average yearly revenue per customer.

💡

2 AI Control Tower is ServiceNow’s centralized layer for AI governance and oversight inside the Now Platform. It gives an enterprise one place to see and manage its AI across the organization.

What I shared in this article: when you introduce a new product suite, it needs time to scale. It rarely shows up as an immediate step change in revenue in a quarter or two. But the market is like a junky that's looking for instant gratification. That’s usually a net benefit for long term investors who can let adoption compound while the market still has to figure it out.

Right now, the market is unanimously downvoting software stocks, despite strong performance and no signs of AI eating their lunch. On the contrary.

3 - Possible reasons for the sell-off

- Deceleration anchoring: The market may be anchoring to constant currency deceleration, not the headline beat. Q1 implies 18.5% to 19% subscription growth in constant currency, down slightly from 19.5% in Q4.

- Acquisition risk: Integration and the quality of underlying organic growth may be getting more attention. Some investors will ask what growth looks like without M&A support, especially given the narrative that ServiceNow has been active on deals.

- Sentiment: This might be the biggest driver. Software sentiment feels extremely fragile. It reminds me of 2022, where anything that isn’t a blowout gets punished. Those periods can create great long term setups, but they can feel (very) uncomfortable in the moment.

4 - Management highlights

AI platform narrative: McDermott framed ServiceNow as the "AI control tower" for enterprises and emphasized accelerating net new business and strong platform activity. Now Assist momentum was called out as meaningful.

Large deal and enterprise momentum

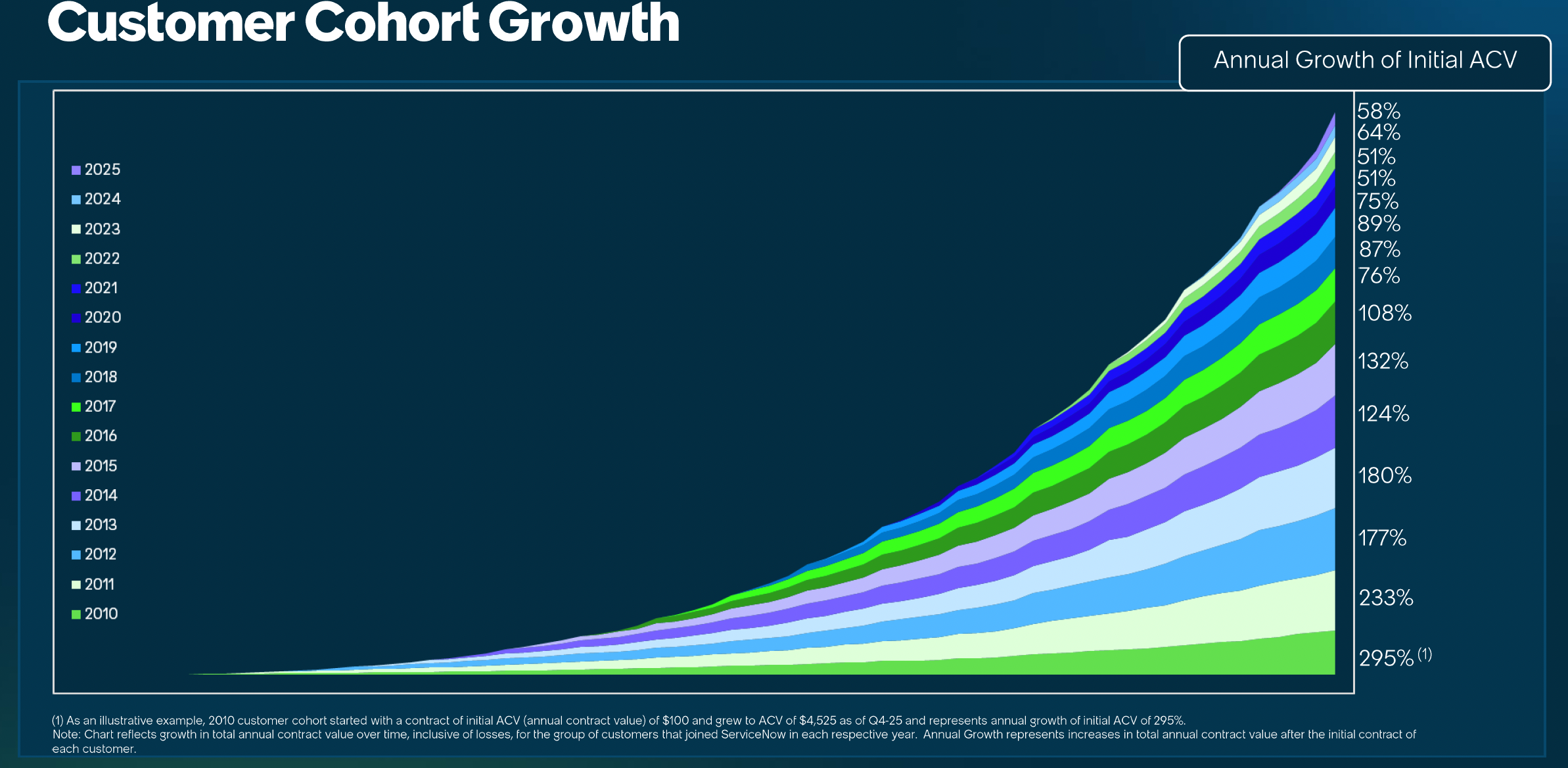

ServiceNow reported 244 transactions over $1M in net new ACV, up nearly 40% year over year. Customers with more than $5M in ACV rose to 603, up about 20% year over year. What their customer cohort looks like as of Q4 2025:

Capital return support

The board authorized an additional $5B for buybacks, plus an imminent $2B accelerated repurchase, with an explicit goal of managing dilution.

5 - My take

If you strip it down, the quarter itself was strong. They beat, they guided above consensus, and the big account indicators stayed healthy. Renewal rate is still a staggering 98%. Now Assist surpassed $600M in ACV with strong demand.

The important nuance is that ACV is not revenue. It is a sales and contract metric. But even as a directional indicator, it matters because it shows AI is becoming a real expansion lever.

If you compare it to the FY 2026 subscription revenue guide of about $15.5B, $600M in AI ACV is already meaningful. It is still early, but it is no longer trivial.

The market wants to see re acceleration and they want it NOW (hehe, see what I did there). Jokes aside, that’s not how product ramping works. It needs time. I do think the stock can stay under pressure until AI and acquisition activity translate into cleaner, sustained growth signals that remove any doubt.

Final verdict

Thesis is very much on track. The sell off looks more like a sentiment driven move than fundamentals deteriorating. For patient investors who can sit through volatility, this could be an attractive spot to accumulate and let the business compound over time.

In the short run, the market is a voting machine but in the long run, it is a weighing machine ~ Bejamin Graham

As always, none of this is financial advice. Always do your own due diligence before making an investment decision that fits your own risk tolerance and time horizon.

Written by

Sign-up

And receive the latest visuals and articles straight to your inbox

Member discussion