Rubrik earnings recap Q4 2025

Let's unpack a very strong RBRK quarter, covering the business, outlook, management commentary and making sense of the stock price movement.

What Rubrik does

Rubrik provides cyber resilience and AI operations software. Their platform protects data, identities, and workloads across on premises, cloud, and SaaS environments.

When ransomware hits or AI agents go rogue, Rubrik's proprietary preemptive recovery engine pinpoints the clean state of data and identities to get businesses back online fast.

They make money through subscriptions to Rubrik Security Cloud for cyber resilience and the newly launched Rubrik Agent Cloud for AI agent governance (more on that in the recap as well). What makes them interesting is they're redefining the entire data protection market as an AI enablement play while winning against legacy competitors at a 90% plus rate. You you read my full deep dive below.

Rubrik Deep Dive: A mission-critical cybersecurity company

A crucial player in a world where data breaches and rogue AI agents are not an IF but a WHEN. In this deep dive you’ll learn everything about this unique cybersecurity business, which is operating at the intersection of data and AI.

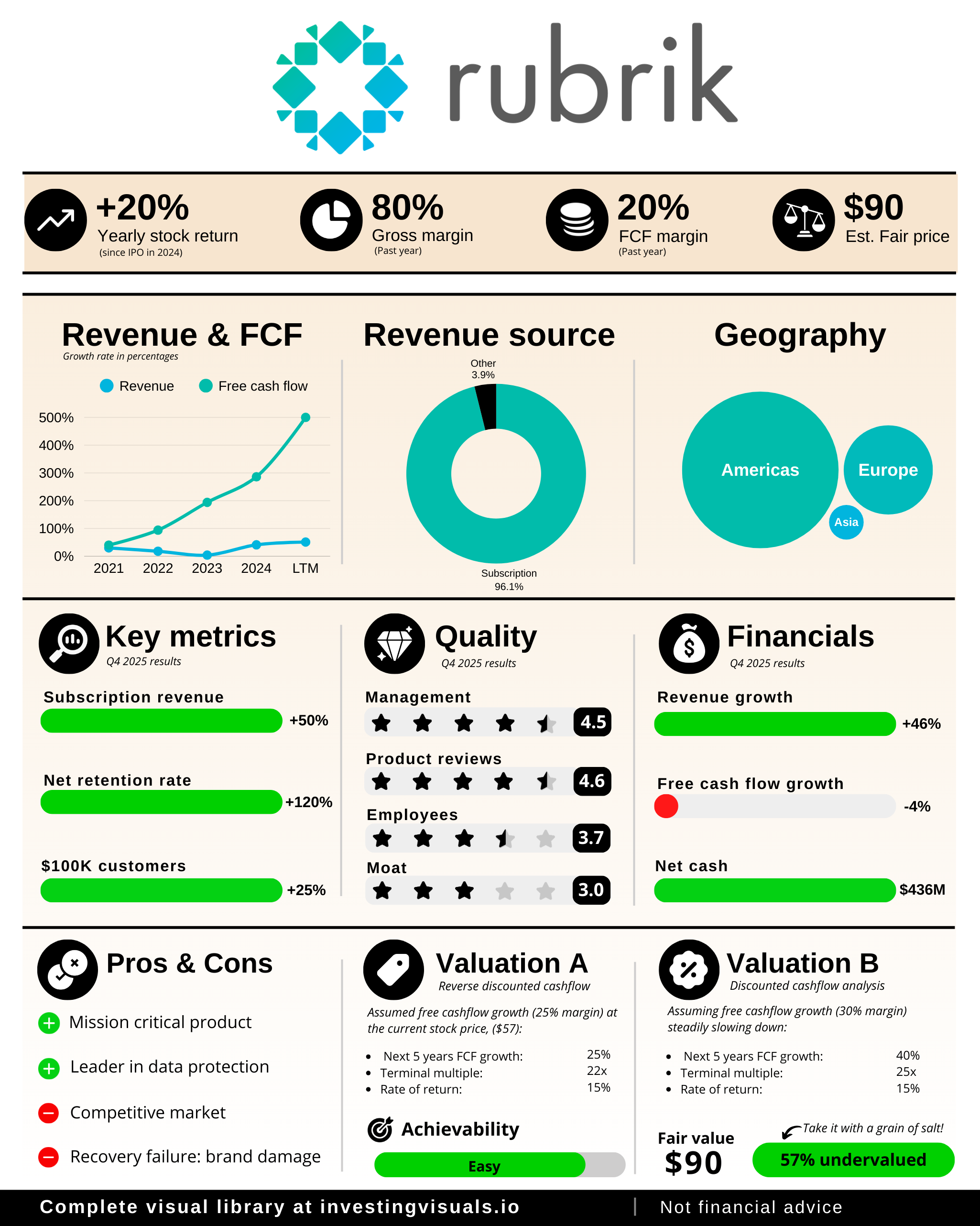

1 - Key numbers

Q4 2025

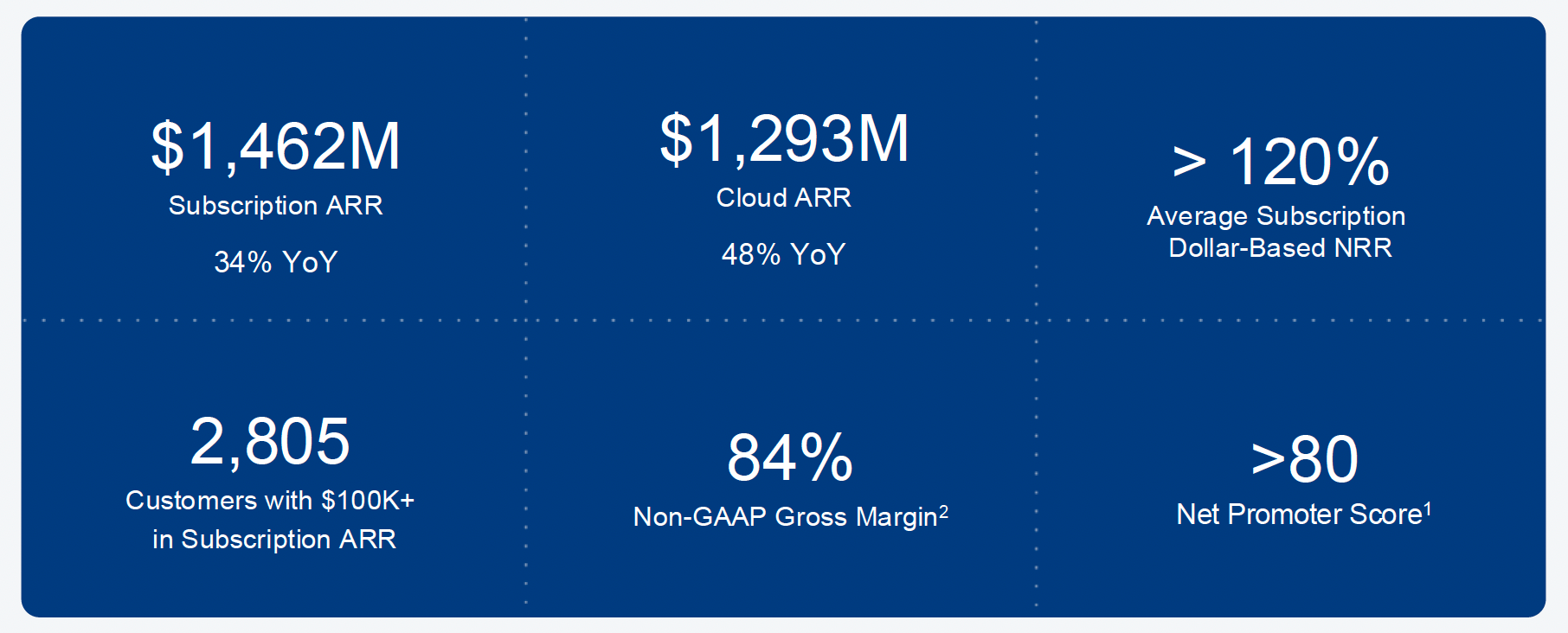

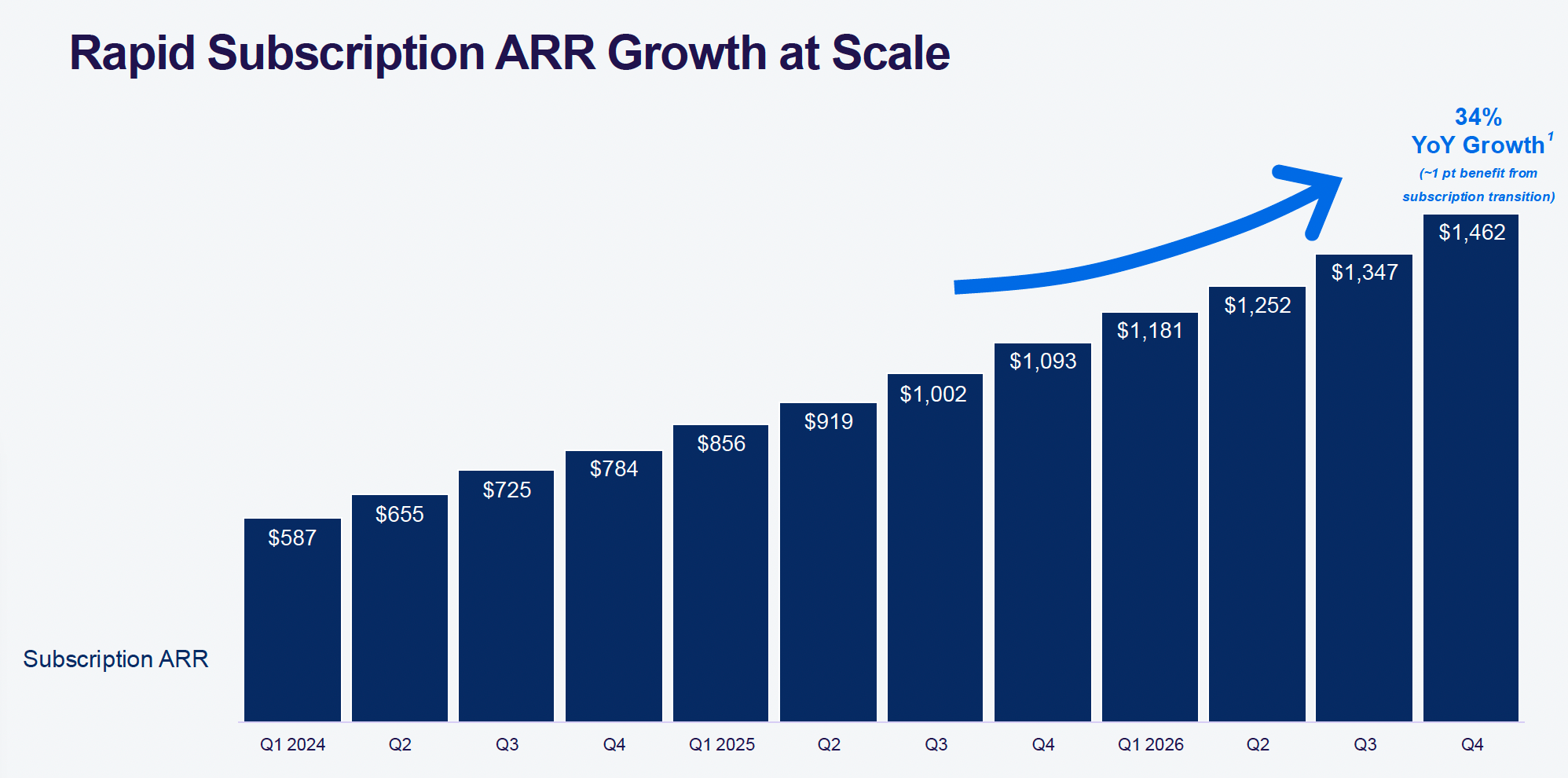

- Subscription ARR: $1.46 billion, up 34%

- Net new subscription ARR: $115 million

- Subscription revenue: $365 million, up 50%

- Total revenue: $378 million, up 46%, 43% normalized for material rights

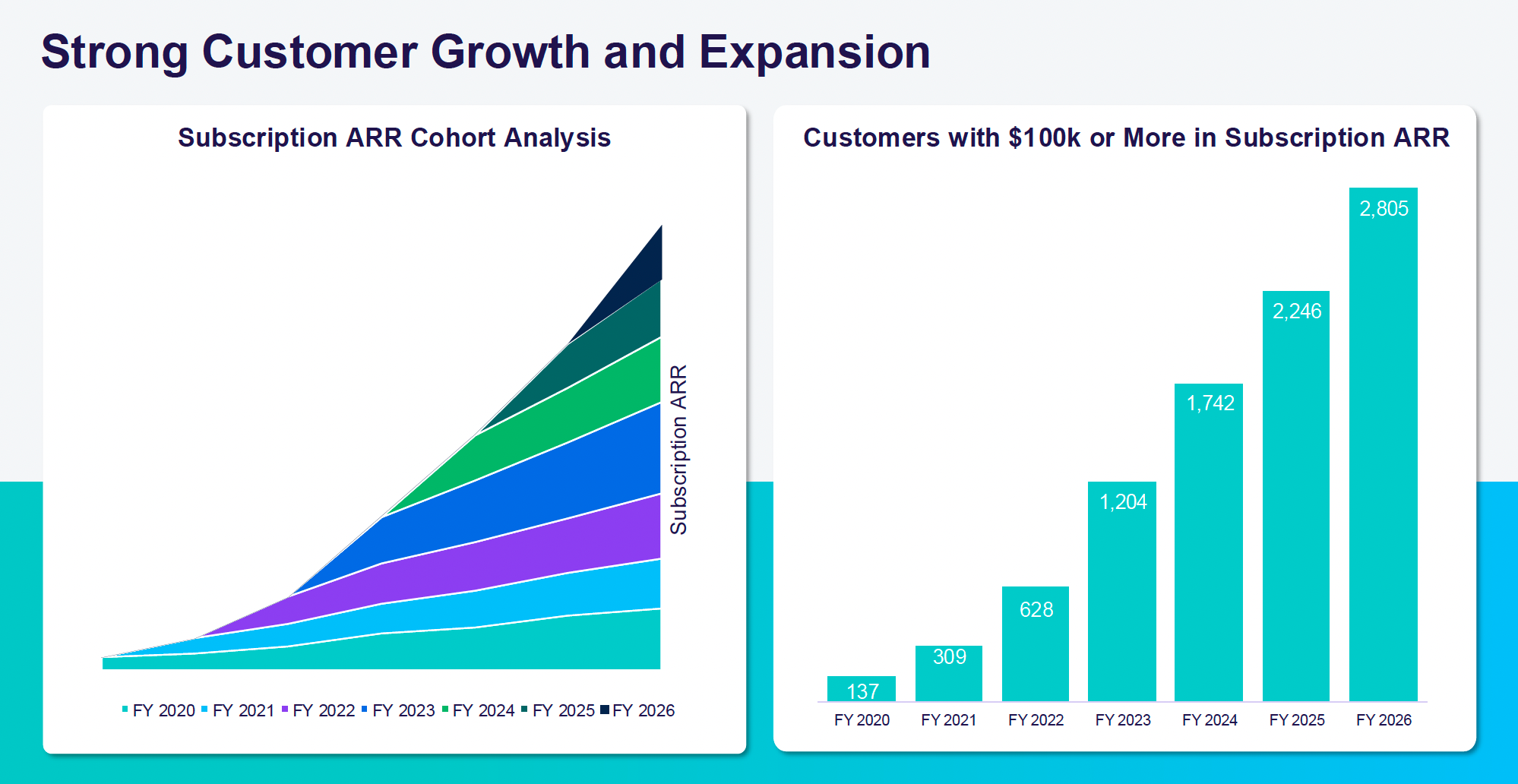

- Customers with $100K plus subscription ARR: 2,805, up 25%

- Added 32 customers with $1 million plus subscription ARR

- Subscription dollar based net retention rate: above 120%

- Cloud ARR: $1.29 billion, up 48%, now 88% of subscription ARR

- Non GAAP gross margin: 84% versus 80% prior year

- Subscription ARR contribution margin: 12%, up 950 basis points

- Free cash flow: $70 million

Full year 2025

- Subscription revenue: $1.26 billion, up 53%

- Total revenue: $1.32 billion, up 48%

- Free cash flow: $238 million versus $22 million prior year

- Non GAAP gross margin: 82.3% versus 78% prior year

- Subscription ARR contribution margin: 12% versus 2% prior year

2 - Outlook

Q1 2026 guidance

- Revenue: $365 million to $367 million, up 31 to 32%, or 36 to 37% normalized for material rights

- Material rights contribution: approximately $4 million

- Non GAAP subscription ARR contribution margin: 10 to 11%

- Non GAAP EPS: negative $0.04 to negative $0.02

- Weighted average shares outstanding: approximately 204 million

Full year 2026 guidance

- Subscription ARR: $1,829 million to $1,839 million, up 25 to 26%

- Revenue: $1,597 million to $1,607 million, up 27 to 28% normalized for material rights

- Material rights contribution: approximately $10 million

- Non GAAP subscription ARR contribution margin: approximately 13%

- Non GAAP EPS: $0.07 to $0.27

- Weighted average shares outstanding: approximately 232 million

- Free cash flow: $265 million to $275 million

The guide assumes modest contribution from Rubrik Agent Cloud in 2026. Management expects 42% of net new subscription ARR in the first half, 58% in the second half. Q1 should contribute around 23% of full year net new ARR.

CFO Kiran Choudary noted:

"We wanna put forward numbers which are based on all the inputs we have today, but want to put forward something we feel really good about in terms of delivering. As we have progressed in the public markets and now entering the third year, it is natural as in other software businesses that the results will tend to converge a little bit closer, more to guidance over time."

3 - Business highlights

The core cyber resilience business is firing on all cylinders. Rubrik displaced legacy vendors and cloud native backup solutions at multiple Fortune 500 accounts this quarter.

A global hospitality company chose Rubrik over deeply entrenched incumbents, projected to save millions by eliminating cloud native backup costs. A European financial services firm selected Rubrik to meet DORA and ECB compliance guidelines, replacing a multi decade legacy provider.

The competitive win rate crossed 90% in Q4. As Bipul put it: "The only deal that we are losing is the fight that we are not in."

Identity recovery keeps scaling

Identity became the fastest growing product in company history. Rubrik crossed 900 customers on identity solutions in Q4, up from 400 in Q3. The product expanded from Active Directory and Entra ID to include Okta this quarter, making Rubrik the only identity recovery platform spanning all three.

A Fortune 500 financial services firm added Okta Recovery along with Identity Resilience and data protection to meet a board mandated sub 48 hour recovery time objective. A major healthcare provider adopted Identity Resilience expecting to cut Active Directory and Entra ID recovery time from over 30 days to under four hours, reducing potential downtime losses estimated at tens of millions daily.

Over 45% of subscription net retention rate in the quarter came from adoption of additional security products, up from 34% a year ago. Over 50% of M365 bookings attached to identity solutions.

Rubrik Agent Cloud launched

The company made Rubrik Agent Cloud generally available just weeks ago after being in beta last quarter. Early proof of concepts are running with Fortune 500 companies and AI first startups.

The product addresses a straightforward problem. AI agents promise 100x productivity but introduce 100x risk as well. Agents assume identities and act on trusted data autonomously. If they hallucinate or get compromised, they can do catastrophic damage in a fraction of the time.

Rubrik Agent Cloud provides visibility into what agents exist, monitoring of what they're doing, real time guardrails to authorize or block agentic interactions, and the ability to rewind and undo destructive actions. The Predibase acquisition brought the LLM fine tuning and inference capabilities needed to use AI to control AI agents dynamically.

Bipul framed it this way: "While AI gives you a better, faster car, you need an intelligent, autonomous driving system for control to steer, change lanes, and brake safely."

Customer interest is focused first on agent inventory and monitoring, second on real time dynamic guardrails. The rewind capability will become critical once enterprises operate agents at scale.

Platform momentum

The company promoted Jesse Green to Chief Revenue Officer this quarter. Green ran Americas the past three years and was essentially CRO in training. Bipul emphasized stability: "The team is stable and in place and executing. The opportunity in front of us with respect to three lines of business, data protection, Identity Resilience, and AI, all three are very exciting."

Rubrik introduced Rubrik Security Cloud Sovereign for customers needing data sovereignty controls in response to evolving geopolitics and regulatory landscapes. They announced Intelligent Business Recovery for Microsoft 365 with automated, business aware recovery. They introduced DevOps Protection for Azure DevOps and GitHub repositories.

Customer expansion remains strong. Large customers with $100K plus ARR now represent 87% of subscription ARR, up from 84% a year ago. The $1 million plus customer base grew over 50%.

4 - Management commentary

Bipul positioned Rubrik as building the most important security and AI operations company for the AI era. He said: "I always am a huge believer in non consensus ideas, and we are building the most important AI company that nobody is focused on."

On the core business:

"We continue to deliver phenomenal results quarter after quarter because we are comprehensively winning against the competition and enabling enterprise AI acceleration. Our competitive win rates have crossed 90% in Q4 as we continue to disrupt the data and identity protection market with our transformative products that deliver comprehensive cyber resilience."

On the AI opportunity:

"When world goes through more AI transformation, it has more data, more software, more cyber threat, larger surface area of attack. More agents means more surface area of attack, more cyber compromise. You need more cyber resilience. You need more cyber recovery."

On durability against AI disruption risk, Bipul was emphatic:

"Rubrik is a very large and complex piece of software, and it is an enterprise scale code with about 12 years of soaking time with thousands of customer feedback and customer use cases in a large enterprise environment that has been built into this. It is not something that you can write code or an LLM can solve. We are the system of record of last resort around data and identity when a large bank or large hospital face a ransomware attack."

Kiran highlighted the path to profitability at scale: "Subscription ARR contribution margin was 12% in the last 12 months, ended January 31st, compared to 2% in the year ago period, an improvement of approximately 950 basis points. The improvement in subscription ARR contribution margin was driven by higher sales, the benefits of scale, and improving efficiencies and management of costs across the business."

5 - My take

This quarter had everything I would want to see as a shareholder. Rubrik growth is top notch, while the legacy competition stalls. They're winning 90% plus of competitive deals. They're expanding operating leverage dramatically. And they're opening new S curves in identity and AI agent governance while the core cyber resilience business still has a very long runway.

The identity product scaled faster than anything in company history. The Agent Cloud launch timing is strong; enterprises want to move fast with AI but are legitimately concerned about agent risk. Rubrik has a unique angle because their platform already understands data, identity, and application context across hybrid environments. Using AI to control AI agents in real time makes sense. The rewind capability is differentiated.

The guide feels a bit cautious which I think is the main reason the stock isn't up +20% or more, which would be reasonable for a quarter like this. The guide implies a slowdown from 34% to 26% which seems material. In reality, I think the actual ARR numbers are likely to be closer to 29%-30%, with management being known to sandbag guidance.

Memory pricing and hardware supply constraints got mentioned on the call, though management said they haven't seen material impact yet. The CRO transition seems smooth but always worth watching. Agent Cloud is very early and competing in a crowded market so it'll be interesting to see how this ramp will go.

If they can continue driving subscription ARR contribution margin higher while growing ARR mid 20s% for a sustained period of time, this becomes a durable compounder. The early results suggest they can.

What I'll be watching

- Agent Cloud traction and customer count in coming quarters

- Identity customer growth and attach rates to core business

- Competitive win rates and legacy vendor displacement momentum

- Free cash flow conversion and capital allocation

What would change my mind

- Competitive win rates declining materially

- Subscription dollar based net retention rate falling below 115%

- Agent Cloud failing to gain traction or getting commoditized quickly

- Margin expansion stalling or reversing

- Material customer churn in the enterprise base

The long term thesis is fully intact. Rubrik built a "bunker" for the AI era and enterprises are happily buying it. The combination of winning the legacy displacement cycle, scaling identity at record pace, and opening the Agent Cloud opportunity creates multiple paths to durable growth. If they execute, this can be become a long term winner in a world where protecting data and governing AI agents was never more important then it is today.

As always, none of this is financial advice. This is simply my breakdown of the quarter and my thoughts on it. Always do your own due diligence before making an investment decision that fits your risk tolerance and time horizon.

Written by

Sign-up

And receive the latest visuals and articles straight to your inbox

Member discussion