Ouster - The eyes of AI

A founder-led business positioned at the rare intersection of robotics, autonomous driving, and physical AI. In this write-up, you'll learn what they do, who runs it, and how all the pieces synthesize into my investment thesis.

Introduction

When I first came across Ouster, it reminded me of an early AXON Axon in term of business trajectory:

- Uniquely positioned in its respective segment

- Started as a hardware business

- Threading software into their stack

- Created a strong interlocking flywheel, resulting in increased customer value, expanding margins and a stock that followed suit

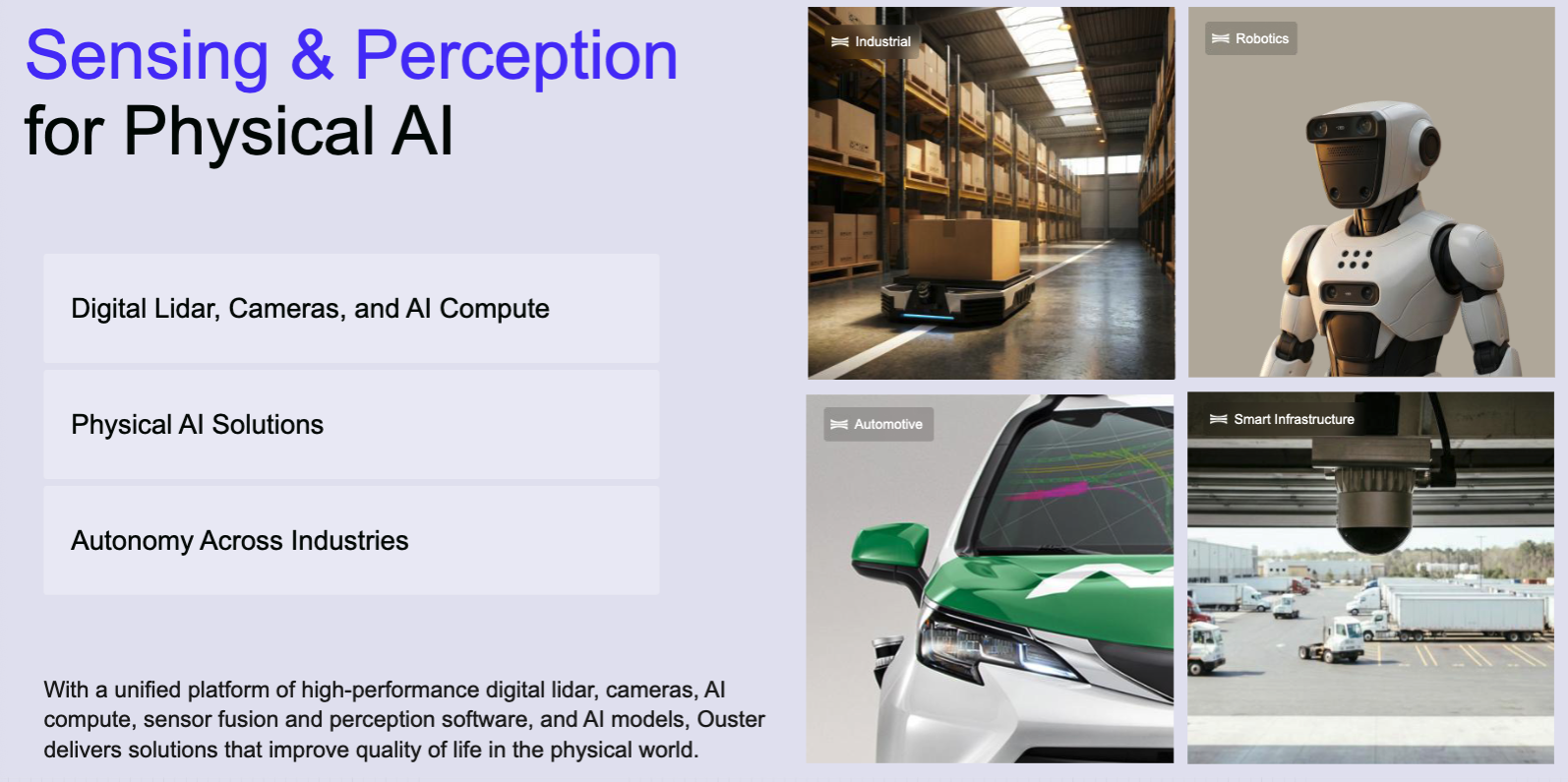

OUST is positioning itself as the physical AI sensing and perception platform, beyond simply being a hardware supplier.

The business recently popped up on my radar after Daniel Koss (@daniel_koss) and PPDD (@usppdd) posted about it on X. What pushed me look into the business deeper, was a combination of things that I love to see:

- Perfectly positioned to benefit from several major durable tech trends:

- The rise of psychical AI

- Autonomous driving

- Drones

- Smart infrastructure

- Robotics

- Founder led with a highly driven and motivated management team

- A strong and innovative company culture

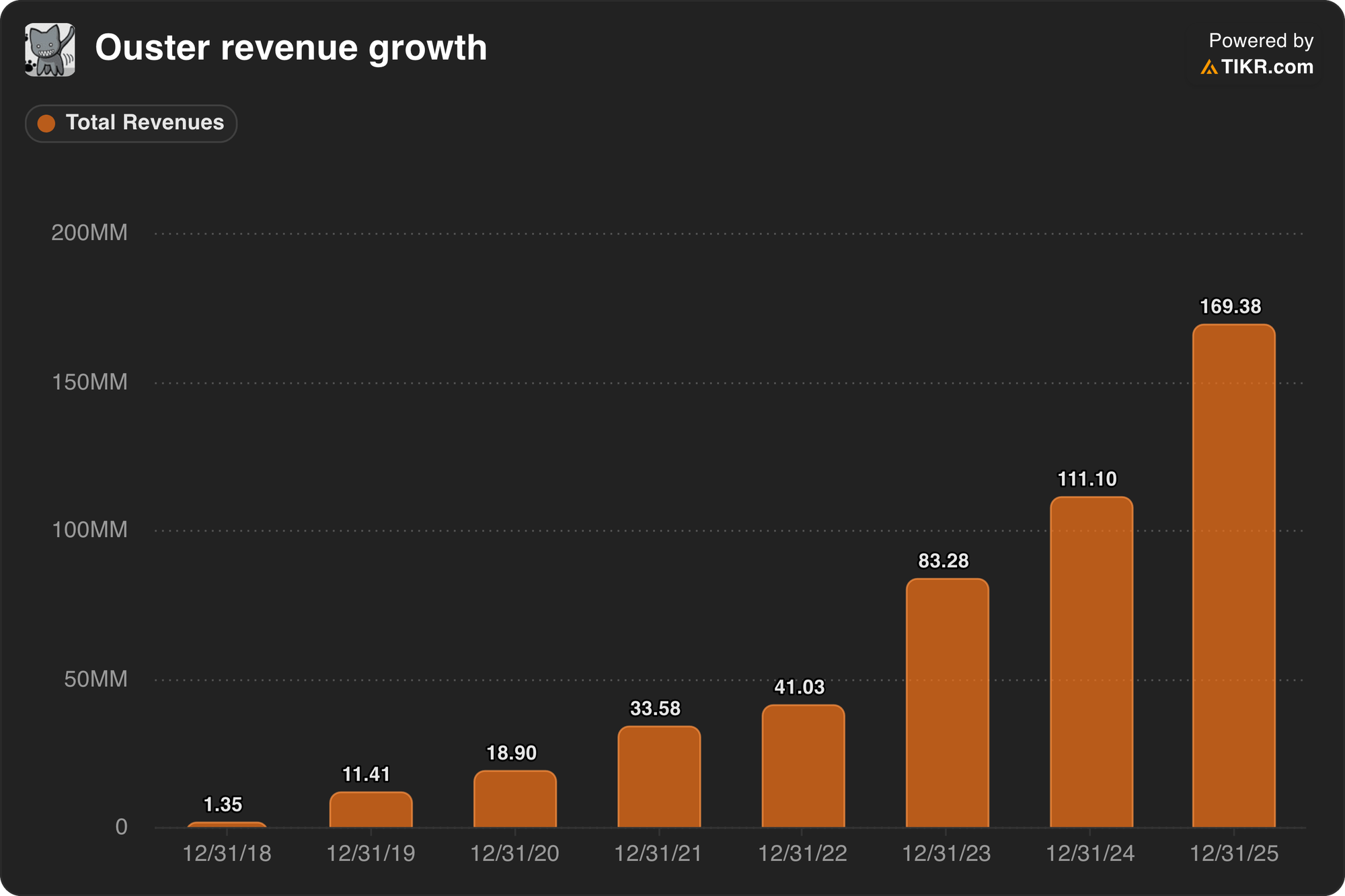

- 12 consecutive quarters of strong revenue growth, gross margins expanding from the high teens to nearly 50% and a strong balance sheet

After this write-up, you'll have a good understanding what Ouster does, who runs the business, how they are positioned within their industry, and how all these pieces synthesize into my investment thesis.

1 - Management

Angus Pacala co-founded Ouster in 2015 and has run it since day one. He hold a BS and MS in mechanical engineering from Stanford, and before Ouster he was Director of Engineering at Quanergy, one of the original solid-state LiDAR companies. I personally always like leaders who have had their fingers in the dirt, so to speak. They know the space what works and what doesn't.

Mark Frichtl is co-founder and CTO and the technical vision behind Ouster. This kind of founder-level technical leadership is what I love to see. Mark holds a Bachelor of Science degree in engineering physics and a Master of Science degree in mechanical engineering from Stanford University.

On the CFO side, Kenneth Gianella joined in April 2025, bringing over 20 years of financial and operational leadership experience. Prior, he was CFO at Quantum Corporation. His track record in scaling global organizations is a positive signal.

In April 2026, Ouster promoted Cyrille Jacquemet to Chief Revenue Officer. Jacquemet has been at the company since 2018 and was Senior Vice President of Global Sales since 2023 and with this new role OUST is positioning itself for what Pacala has called its "next growth chapter."

In short

This is a founder-led business with deep technical roots. The recent CFO transition introduces some execution uncertainty, but the core leadership team is long standing and has a proved track record.

2 - Industry context

LiDAR, short for Light Detection and Ranging, is the technology that lets machines see the physical world in three dimensions with precision that cameras and radar cannot match alone.

Where a camera captures light intensity and color, and radar gives coarse distance data, LiDAR emits laser pulses and measures the time they take to return, building a dense point cloud of the environment in real time.

💡

Think of it like echolocation for machines, but using light instead of sound. Where a bat gets a rough outline of the cave, a LiDAR sensor gets a precise, three-dimensional map of everything around it, updated multiple times per second.

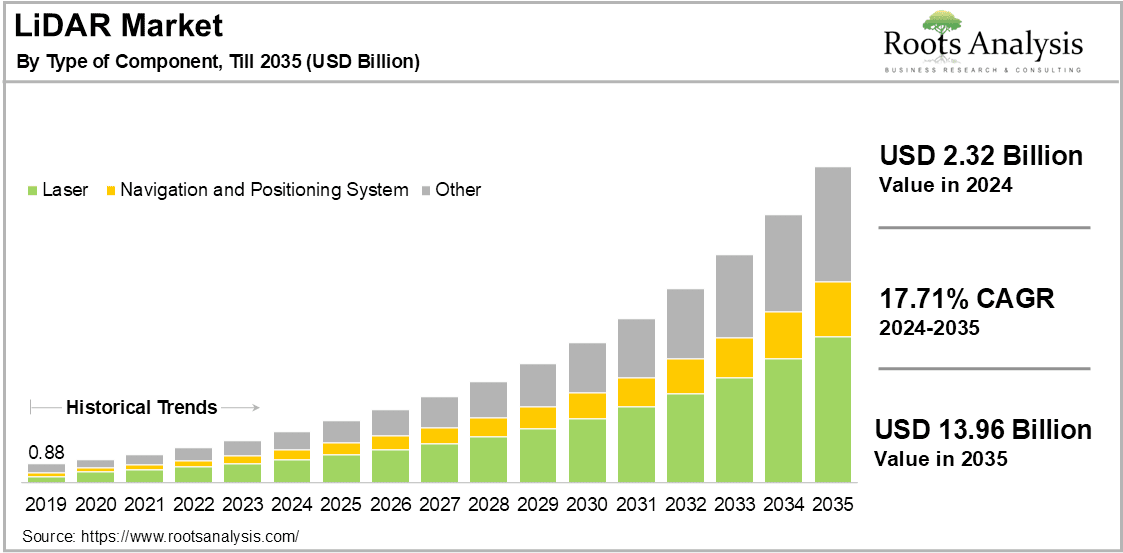

The global LiDAR market was worth roughly $3 billion in 2025 and is forecast to reach $14 billion by 2035, growing at roughly 18% per year. The solid-state segment, which is where Ouster's Chronos chip sit, is growing much faster, with projections of $3.2 billion by 2030 from $500 million in 2025, a 45% CAGR.

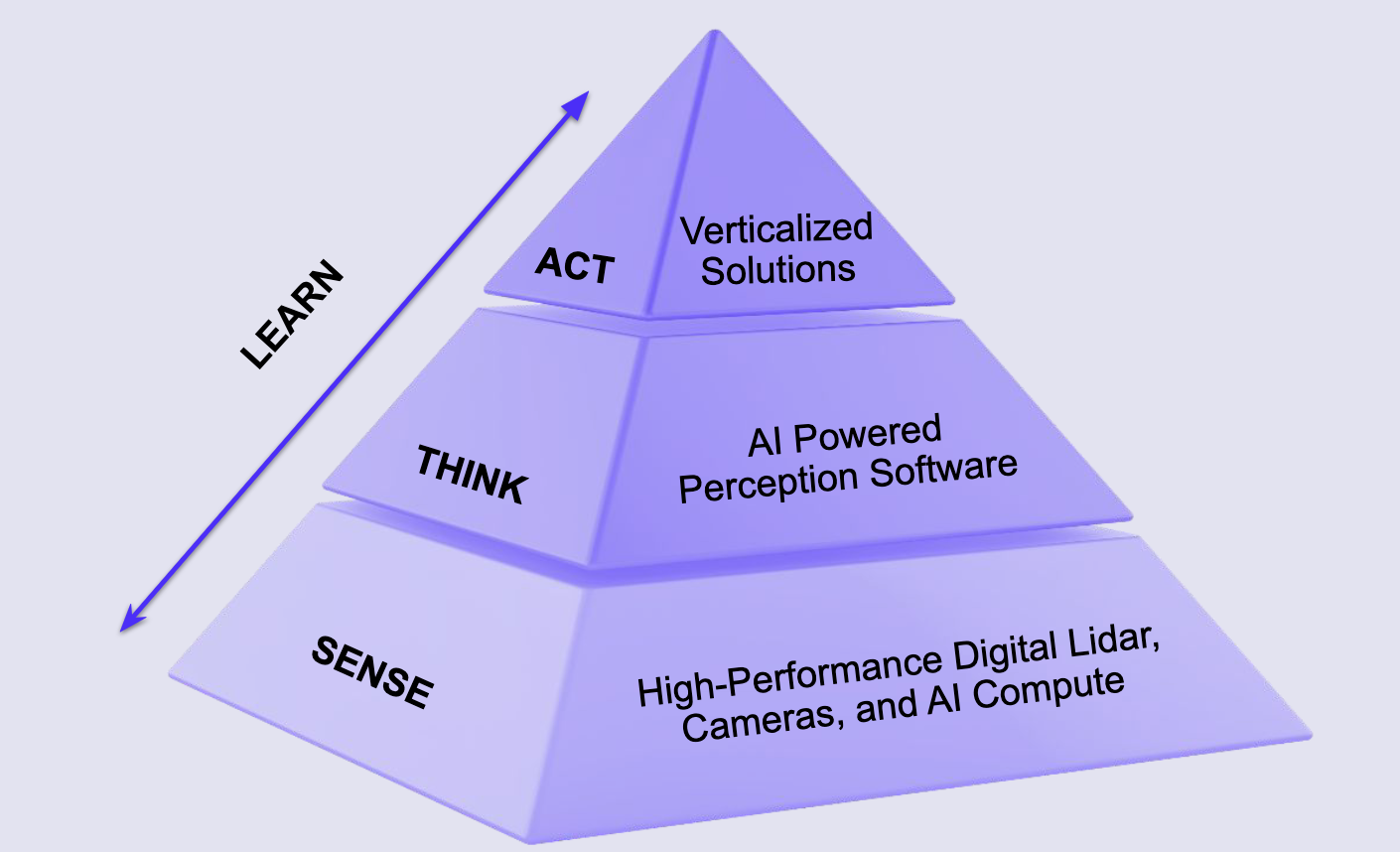

But that's just the hardware part. Where I think it gets extra interesting is the software part of it.

For most of LiDAR's commercial history, the value was in the hardware. You sold a sensor, the customer integrated it, and that was that. What is changing is that the real bottleneck for autonomous system deployments is no longer the sensor. It is perception: the ability to turn raw data into actionable intelligence in real time.

"When you think about us and you want to invest in us, number one is the AI software solutions. It's not just about the hardware, it's the platform." ~ Pacala, August 2025,

The companies that own the software layer will be structurally stickier and higher-margin than pure sensor vendors. It is however good to note that software is not yet a major part of their revenue mix, but it's growing significantly.

"Software-attached bookings more than doubled in 2025 and represented over 15% of our sensors shipped, which is up over 120% year on year."

This is where I see close similarities with Axon. They used to be a hardware business but as of today, their software platform is their core growth driver and nearly 50% of revenue. I can see a similar path for Ouster.

3 - Mission and the problem

Ouster mission is to build a safer and more sustainable future through high-resolution digital lidar sensors for the automotive, industrial, smart infrastructure, and robotics industries.

The core customer pain is not just about sensors. It is about deployment: autonomous systems can only be deployed commercially when the full perception stack, from sensor to software to output, is reliable, certifiable, and cost-effective enough to justify the capital outlay.

The company serves four end markets: automotive, industrial, robotics, and smart infrastructure. Each one has a different adoption curve and a different margin profile. Smart infrastructure and industrial are further along in real deployments today. Automotive is the largest eventual TAM but requires the longest qualification cycles.

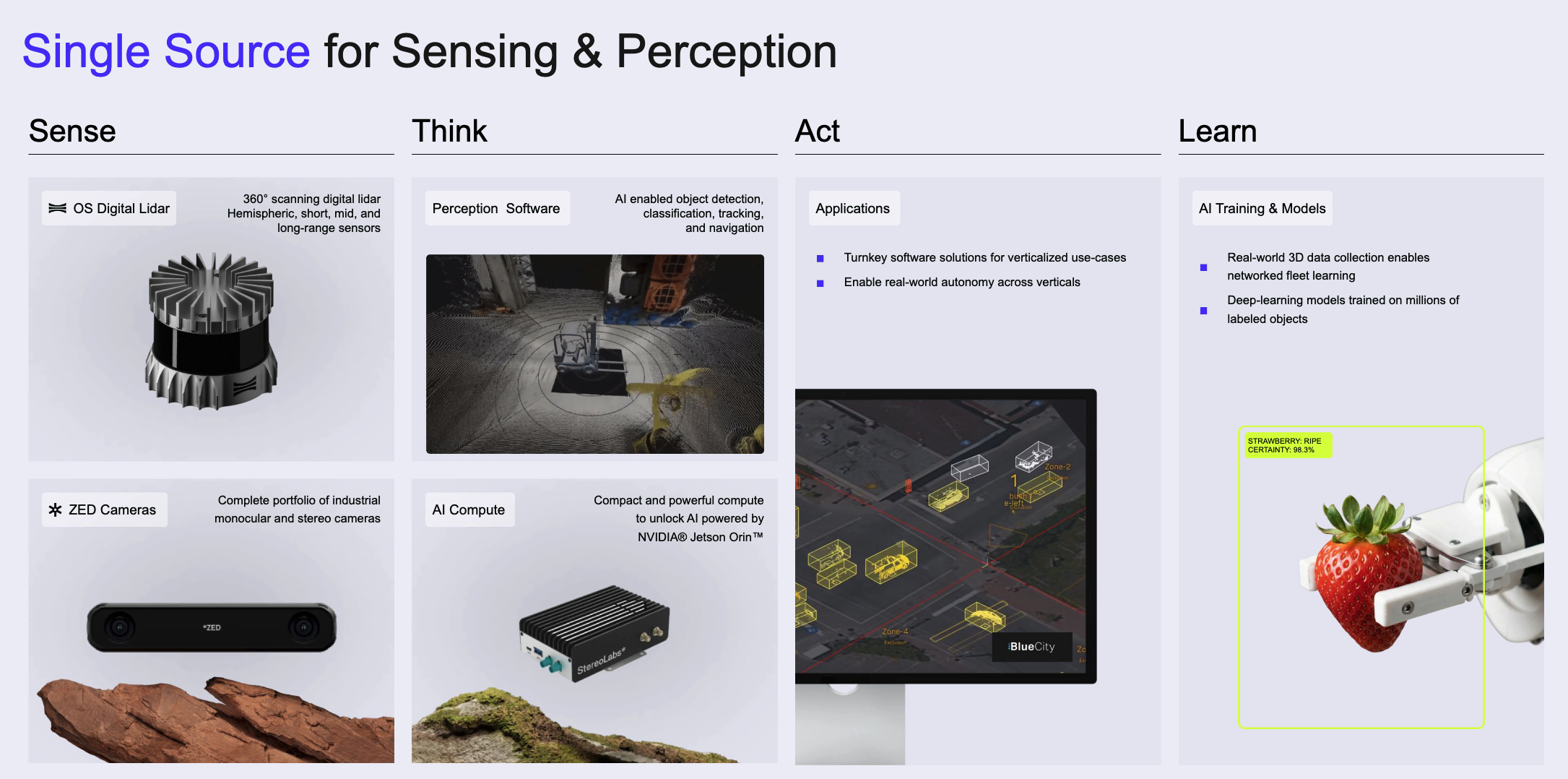

Where Ouster sits in the value chain has been shifting. It started as a sensor manufacturer. With Gemini (its real-time perception engine for object detection and tracking) and Blue City (its data analytics platform for traffic operations and smart infrastructure), it moved toward the platform layer.

They also acquired StereoLabs which adds stereo cameras, AI compute, sensor fusion, and pre-trained AI perception models. The company is now positioning itself as a single-source supplier for the full sensing and perception stack. That is a very different business model from where it started.

What I find particularly interesting with Ouster is that they are exposed to several major tech trends ranging from the robotics buildout, humanoid platforms, smart city investment cycles, autonomous mining and logistics applications.

4 - The technology explained

Traditional LiDAR systems are built from hundreds of discrete analog components: individual emitters, detectors, and signal circuits wired together at high cost and low scalability.

Think of it like an old telephone switchboard. Ouster replaced that entire switchboard with two chips. A custom CMOS System-on-a-Chip with integrated Single Photon Avalanche Diode detectors, and a Vertical Cavity Surface Emitting Laser array (VCSEL). Fun fact: this is the same laser technology in iPhone Face ID.

Building on CMOS silicon means Ouster sits on Moore's Law: each chip generation improves performance at lower unit cost, the same way smartphone cameras compound without the underlying physics changing. The L3 chip powered all REV7 sensors. The Chronos chip is a parallel track designed for solid-state Digital Flash applications targeting automotive and industrial OEMs.

REV8 and the L4 Silicon Generation. On May 4, 2026, Ouster announced the REV8 family powered by L4 Ouster Silicon, delivering double the range and double the resolution of REV7. That some serious technological progression. It's the first commercially available native color LiDAR sensor: color and 3D depth merged through physics at the point of capture.

💡

Native color LiDAR means color and depth data arrive in perfect alignment from a single sensor. No lag, no stitching, no misalignment. For real-time perception models, that is a meaningful step up from post-hoc camera fusion.

The family spans four models:

- The OS1 MAX, 200m range, automotive-grade

- OS1, mid-range, smart infrastructure and AV

- OS0, 90-degree field of view for robotics and warehouses

- OSDome, 180-degree hemispherical for full-surround coverage

The StereoLabs acquisition layered ZED stereo cameras, AI compute, and pre-trained perception models on top of this hardware foundation, across more than 90,000 deployed cameras and 10,000 customers.

The combination of REV8 native color LiDAR and ZED creates what no competitor currently offers at scale: spatially aligned color-depth sensing with AI perception built in. You cannot replicate this stack quickly. Silicon design cycles run two to three years per generation. Safety certifications take longer and customer integrations are sticky from the moment a design is qualified.

5 - Competitive moat and replication risk

Ouster's moat is narrow but widening. A breakdown of the building blocks of their moat:

1. CMOS silicon architecture: Designing and fabricating a custom SPAD SoC is not a weekend project. It requires years of silicon design expertise, a trusted foundry partnership, and the accumulated learning from prior generations of chips. Competitors using analog architectures face a structural cost disadvantage that widens as Ouster moves through silicon generations.

2. Intellectual property and patent position: The royalty income that appeared in Q4 2025, roughly $21 million primarily from long-term IP license contracts, is a direct signal that competitors recognize the IP and have decided to license rather than litigate. The one-time income bumb is now largely in the rearview mirror, but the IP validation remains.

3. Customer qualification cycles: LiDAR sensors embedded in industrial automation, autonomous mining equipment, and traffic management infrastructure require extensive qualification before deployment. Once a LiDAR sensor is integrated into a system design, the switching cost is not the cost of the sensor. It is the cost of the entire re-design, re-integration, and re-certification process.

4. Software ecosystem depth: Gemini and Blue City are platforms that accumulate customer-specific configuration, training data, and operational workflow integrations over time. A city traffic management system running Blue City has years of local data and workflow integration baked in. That is not easily migrated. Further building on this software stack will help increase the moat over time as switching costs get higher.

5. StereoLabs customer base and developer ecosystem: More than 10,000 customers and 90,000 deployed cameras represent a developer community that builds around the products. Developer ecosystems compound over time: the more developers build on the platform, the more use cases are discovered, the more partners integrate, the harder it becomes to leave.

An important risk to flag

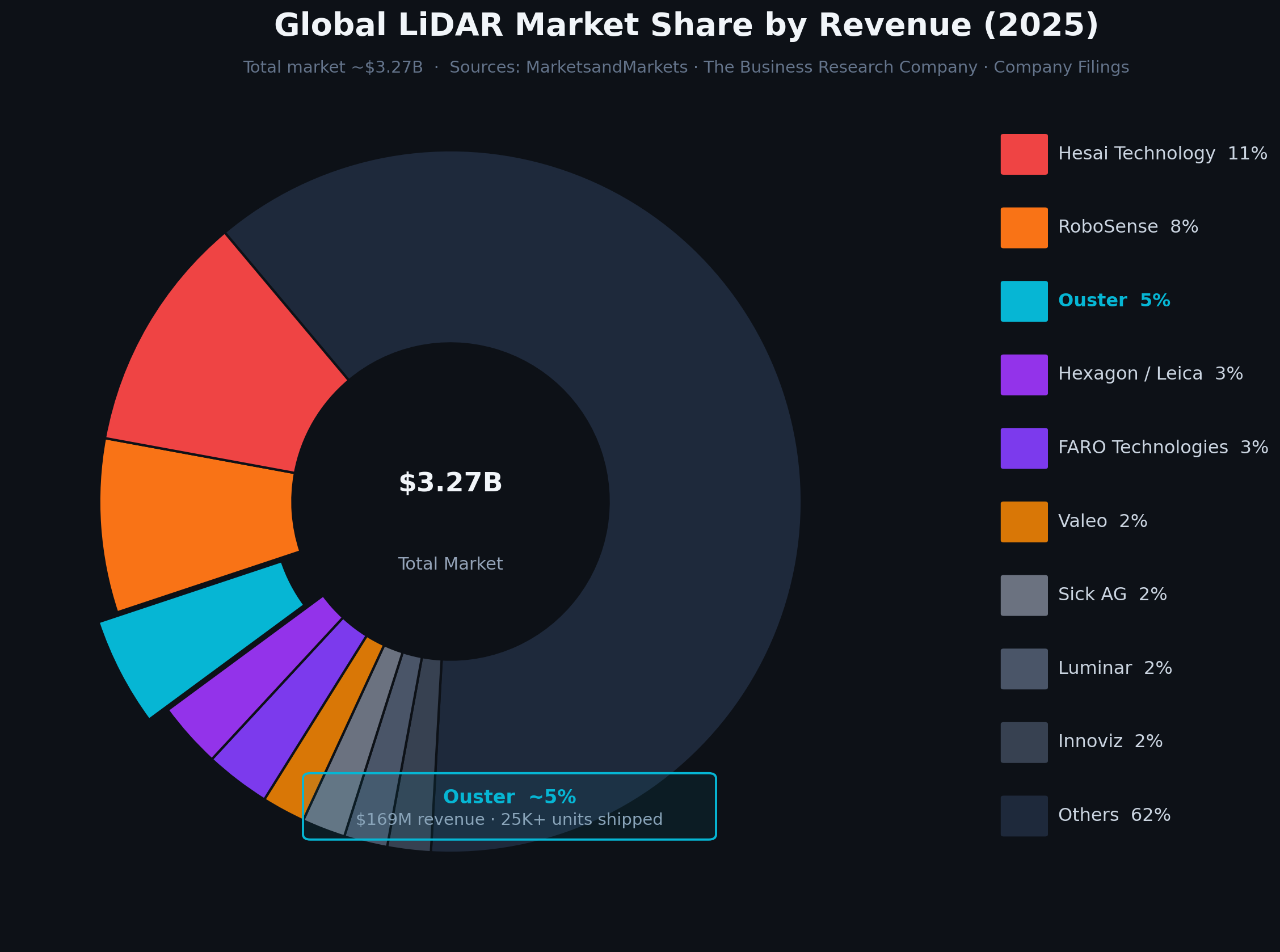

The most credible competitive threat comes from Chinese manufacturers, specifically Hesai Technology and RoboSense, which hold significant market share in automotive LiDAR and have demonstrated the ability to manufacture at lower cost with high volume production.

The Chinese competitors are primarily strong in the automotive segment and less established in the industrial and smart infrastructure verticals where Ouster is currently winning. But if the automotive LiDAR market grows as projected, Hesai's cost structure and production scale could become a more serious threat.

6 - The numbers

Revenue growth is evolving nicely as the revenue mix is shifting from all hardware to a combination of hardware + software. If software becomes a larger part of the mix, margins will likely continue to improve.

Sensor shipments exceeded 25,000 units in 2025, up 47% from approximately 17,000 in 2024. Q1 2026 guidance is $45 to $48 million, which includes roughly seven weeks of consolidated StereoLabs revenue.

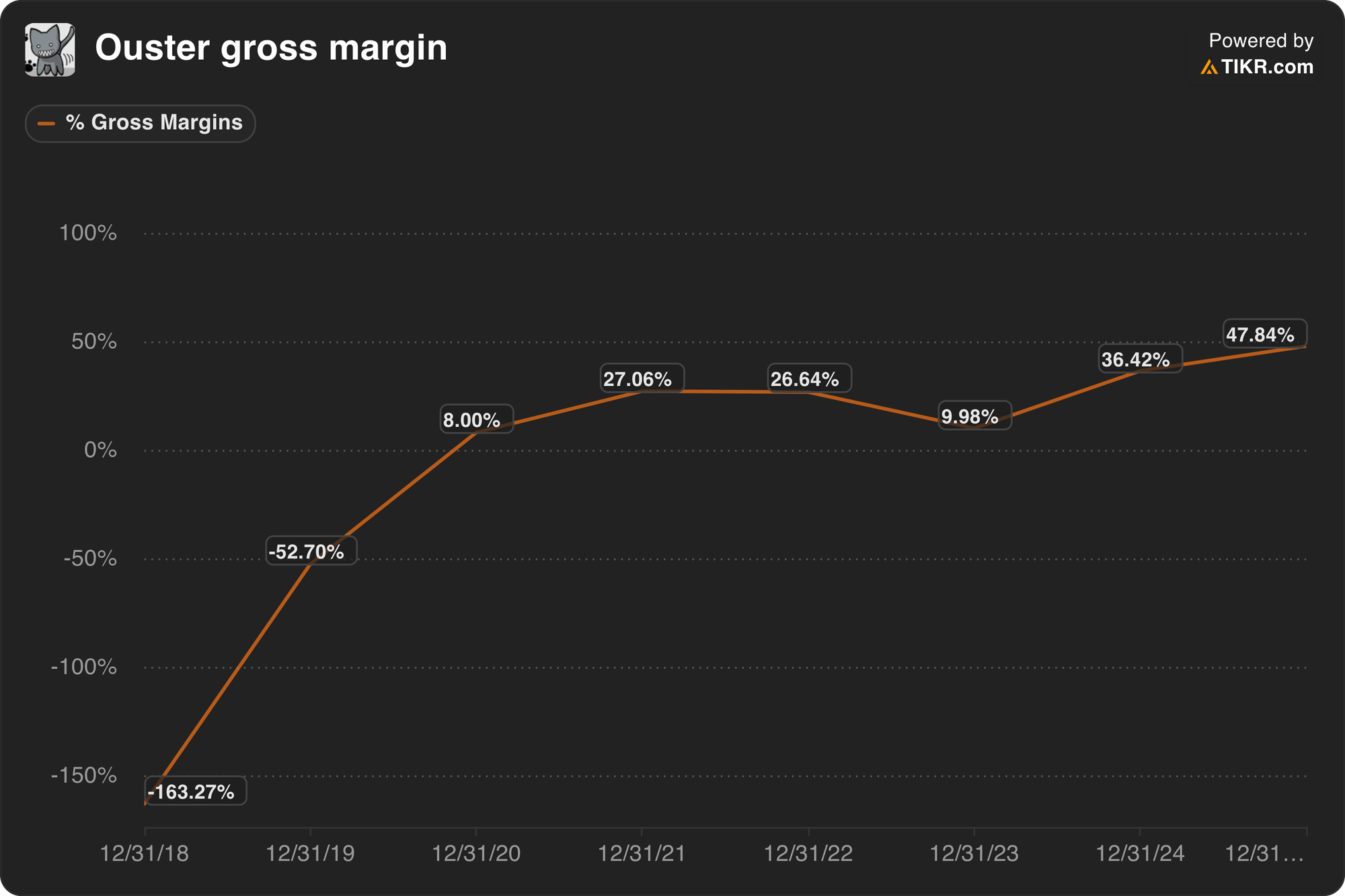

Gross margin: GAAP gross margin expanded from roughly 36% in 2024 to 48% in 2025, driven by volume efficiencies, operating leverage, and the high-margin royalty contributions.

Operating leverage: The business is not yet profitable on a sustained basis. Adjusted EBITDA was positive at $11 million in Q4 2025, but that quarter was structurally inflated by the royalty revenue.

The full-year net loss was $60.4 million on $169 million in revenue. Operating expenses are compressing as revenue scales so operating leverage is moving in the right direction.

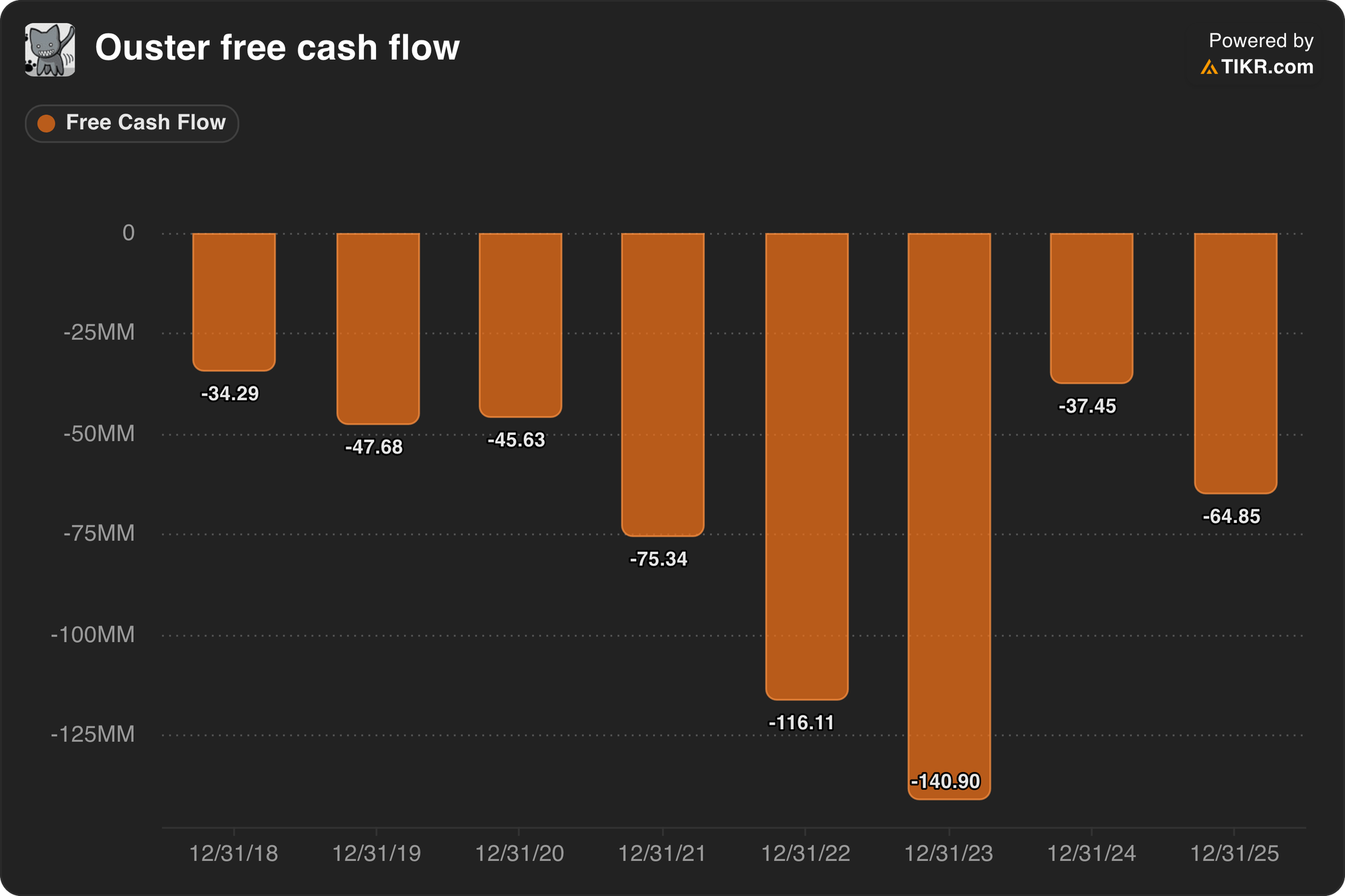

Free cash flow: Negative $64.8 million in FY2025, representing a deterioration from the prior year partially attributable to working capital and growth investment. This is the most significant near-term concern. The business is burning cash even as margins expand so I'd like to see this improve over the next quarters.

Balance sheet: As of Q3 2025, Ouster held $247 million in cash with zero long-term debt. After closing StereoLabs for approximately $35 million in cash in February 2026, the end-of-year 2025 cash position was reported at $211 million. The company carries $0 in long-term debt against equity of $261.7 million. The balance sheet is strong so cash burn is not an immediate concern but definitely something to watch carefully.

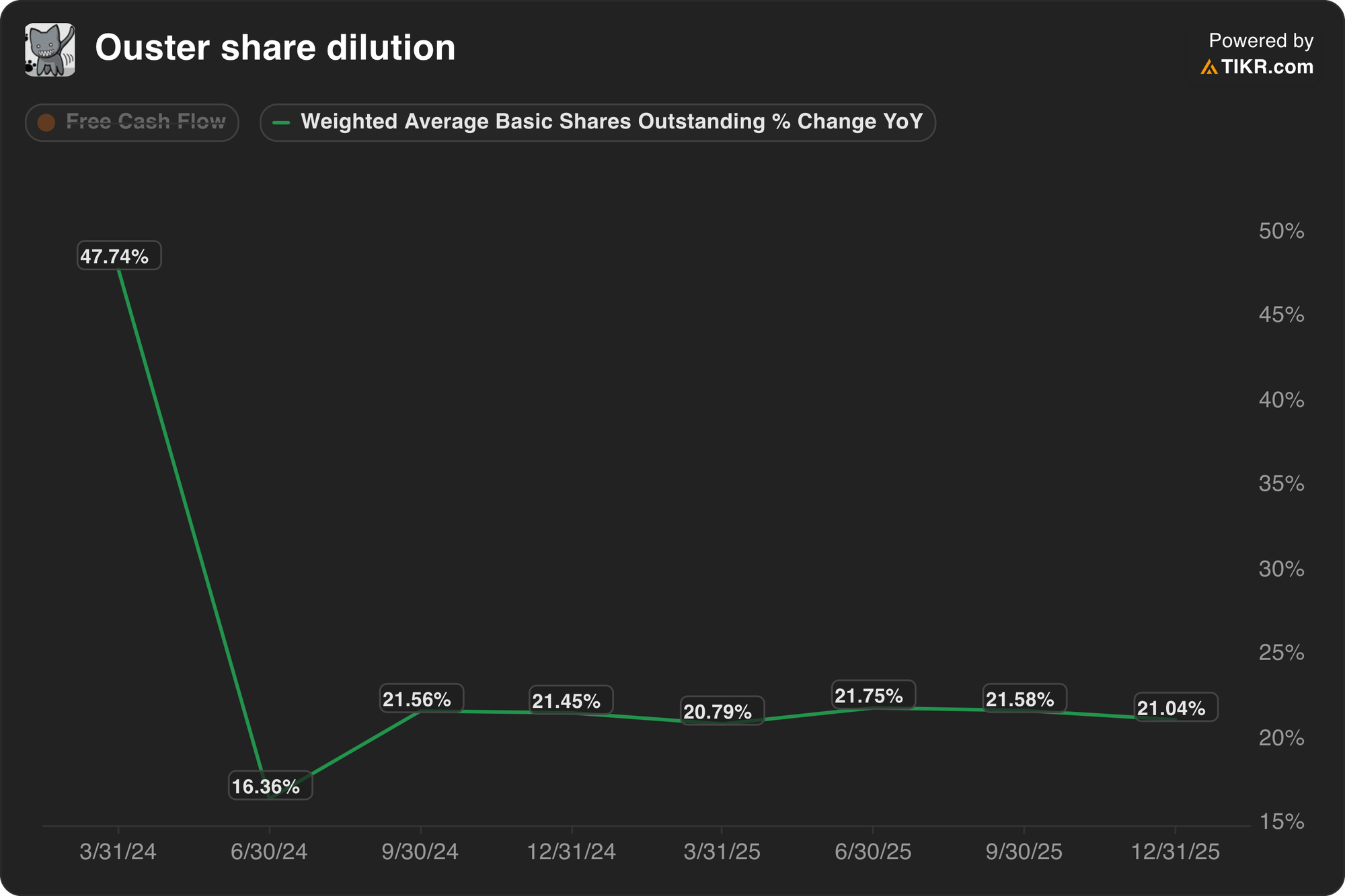

Dilution: Shares outstanding reached 61 million in FY2025, up 21% year over year. The company is also proposing to expand authorized shares from 100 million to 200 million ahead of the June 2026 annual meeting.

At 21% annual share count growth, the dilution is running well above a range I would consider comfortable. This is worth monitoring closely as well. If revenue and profitability do not inflect in 2026 and 2027, the dilution cost can get out of control quickly.

Forward indicators. The company targets 30 to 50% annual revenue growth as its long-term framework. Software bookings doubled in 2025, which is a positive leading indicator for the margin trajectory. Only a small fraction of the 1,000-plus customers are in full-scale production, suggesting meaningful unit volume upside ahead as well.

7 - Risks

Royalty-inflated baseline: The Q4 2025 revenue and margin figures that most investors will anchor to are materially inflated by roughly $21 million in one-time IP royalties. Management has guided that 2026 royalties will be less than $5 million. That means year-over-year comparisons in 2026 will be difficult, and any quarter that looks disappointing relative to Q4 2025 is likely to create volatility even if product revenue continues to grow at 30 to 40%. On the flipside it could mean a nice buy opportunity if the stock gets sold off for the wrong reasons.

Cash burn and dilution compounding: The business burned $64.8 million in free cash flow in 2025 with $211 million in cash on hand. At that rate, the current cash runway is roughly three years. But the StereoLabs integration, the Chronos chip development, and the scaling of software operations all require continued investment.

If the company needs to raise equity before reaching sustainable positive FCF, the 21% annual share dilution isn't what you want to see as an investor. The proposed authorization of 200 million shares is a signal that management is keeping that option open.

Chinese competition on cost and volume: Hesai and RoboSense have demonstrated the ability to produce high-performance LiDAR at lower unit costs by leveraging Chinese manufacturing and supply chain scale. In automotive applications specifically, where unit economics are paramount, cost differences of 20 to 30% are meaningful.

Execution risk on StereoLabs integration: Ouster paid roughly $35 million in cash and stock for a business generating $16 million in revenue. The strategic logic is clear though: add cameras and AI perception to the LiDAR stack and become a full-platform supplier. But there is execution risk: integrating a Paris-based AI vision company into a San Francisco hardware business is a cultural and operational challenge.

Macro sensitivity. Ouster's end markets, industrial automation, smart infrastructure, and robotics, are all capital-intensive investment cycles. In a period of tighter corporate capital budgets or reduced municipal infrastructure spending, deployment timelines can stretch. The company is exposed to cyclicality that does not show up in the product growth record during the current investment cycle.

8 - Valuation context

At a stock price of roughly $26.45, Ouster has a market cap of approximately $1.65 billion and an enterprise value of $1.5 billion. On trailing 2025 revenue of $169 million, that is roughly 8.7x EV/Revenue.

Excluding the one-time royalties, which reduced the recurring revenue base to approximately $146 million, the multiple is closer to 10x. On Q1 2026 guidance midpoint of $46.5 million annualized, the forward revenue multiple is roughly 8x. For a business growing at ~30% that isn't too crazy of a valuation. Not cheap, not expensive either.

What the current valuation is pricing in: revenue growth between 25-30% for the next few years and meaningful gross margin expansion as software and recurring revenue become a larger proportion of the mix.

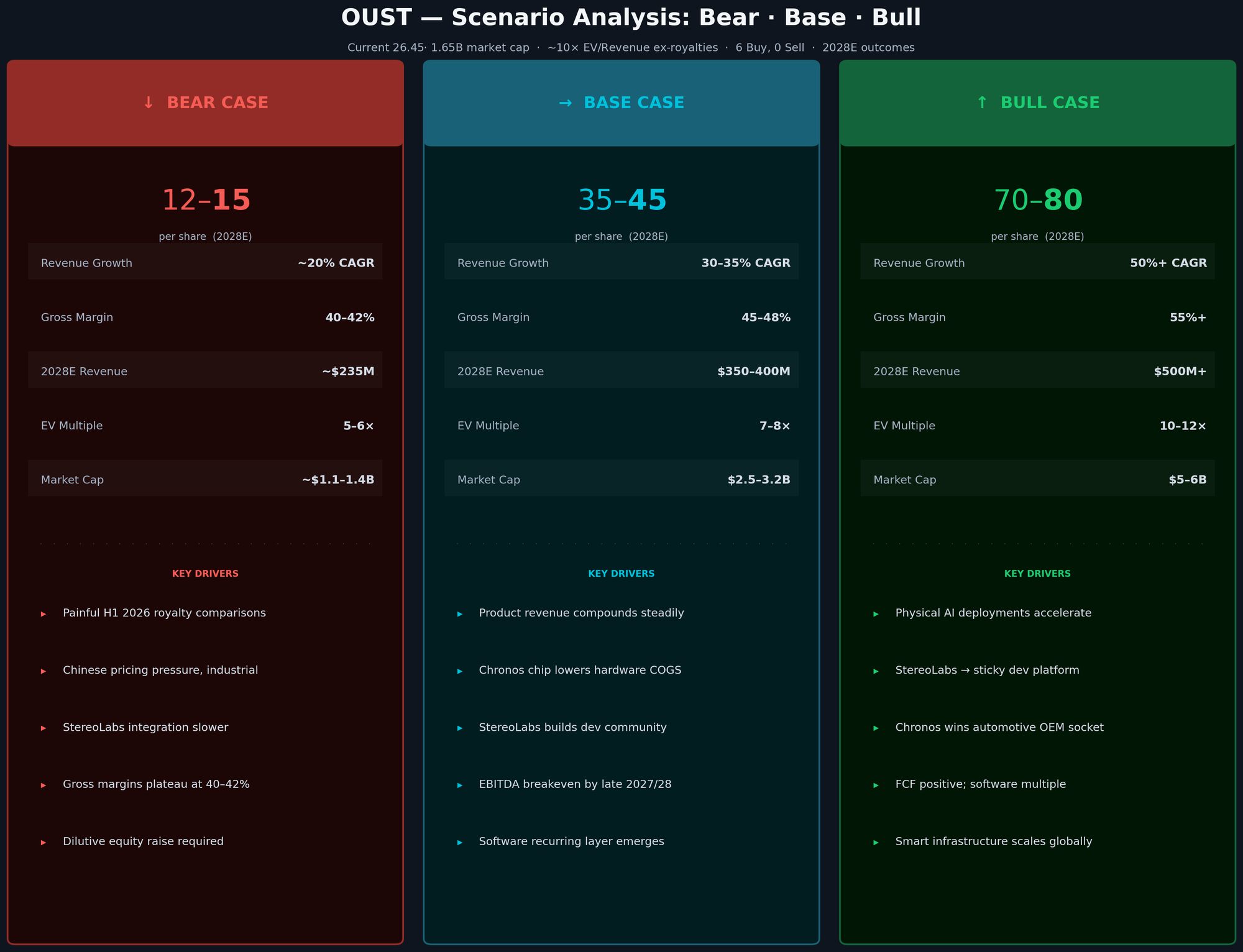

Bear case:

- Product revenue growth decelerates to 20% as Chinese competition pressures pricing in industrial markets.

- StereoLabs integration takes longer than expected.

- Gross margins settle in the 40 to 42% range, not the 50-plus% range that the software-attached thesis implies.

- The company raises equity at dilutive prices to fund continued development. The stock re-rates toward 5 to 6x forward revenue, implying a share price in the $12 to $15 range with a downside of ~45% at today's stock price.

Base case:

- Product revenue continues compounding at 30 to 35% per year.

- Gross margins trend toward 45 to 48% over the next two years as software-attached deployments grow and the Chronos chip reduces hardware COGS.

- StereoLabs adds a meaningful developer community and accelerates software bookings and the company reaches adjusted EBITDA breakeven on a sustained basis by late 2027 or 2028.

- At that point, the stock is valued on a path to profitability with a credible software recurring revenue layer. On a 2028 revenue estimate of roughly $350 to $400 million, the stock could reasonably trade at 7 to 8x revenue, implying a market cap of $2.5 to $3.2 billion, or roughly $35 to $45 per share, which translates to approximately 65% upside. That is broadly consistent with analyst consensus.

Bull case:

- Physical AI deployments in robotics and smart infrastructure accelerate faster than the base case.

- StereoLabs becomes the foundation of a developer platform with a large, sticky community.

- The Chronos chip enters automotive pre-production volumes and Ouster wins a meaningful OEM socket alongside an automotive partner with revenue scaling to $500-plus million by 2028 with gross margins above 55% as software mix increases.

- The company turns FCF positive, and the market re-rates the business toward a software-like multiple of 10 to 12x revenue. That implies a market cap of $5 to $6 billion, or roughly $70 to $80 per share, representing roughly 250% upside, but it does require strong execution on several fronts simultaneously.

9 - Thesis and what to watch

Ouster has built the right hardware to compound performance improvements through multiple generations and it is now layering software and AI perception on top of that hardware foundation while it operates in markets where deployments are beginning to scale.

The combination of recurring software revenue, sticky customer integrations, and a CMOS-based cost reduction roadmap creates a business model that could look very different in three years than it does today.

What makes it durable: the digital LiDAR architecture is defensible at the hardware level, and the StereoLabs acquisition adds a perception layer that hardware-only competitors cannot easily replicate. What makes it somewhat fragile: the company has not yet proven it can generate sustained positive free cash flow.

All in all Ouster is a high quality, founder led businesses that continues to innovate at a very rapid pace. Their fundamental are strong and they operate in a market that is expected to expand rapidly over the years ahead. I think they have a lot of ingredients to do very well over time.

What to watch closely:

- Q1 2026 earnings on May 7, 2026: they posted a great quarter, margins are strong and I think the next generation of Ouster products are becoming extremely valuable for companies that want to train Physical AI models.

- Software bookings trajectory: The company reported doubled software bookings in 2025. Sustained double-digit software booking growth in 2026 would validate the platform thesis.

- Chronos chip production readiness: Any timeline update on when the solid-state Digital Flash sensors powered by Chronos enter customer testing and pilot production.

- StereoLabs integration milestones: Watch for new product announcements that combine LiDAR and camera data in a unified SDK, and for StereoLabs revenue contribution to track against the $16 million 2025 baseline.

- Free cash flow inflection: The key financial milestone is when quarterly FCF turns consistently positive. Any signal that this is tracking ahead of schedule would be a meaningful catalyst.

- Named automotive customer wins: Any announcement of an OEM production design win would shift the perception of Ouster's addressable market meaningfully upward.

How cracks in the thesis show:

- Strong gross margin contraction: If product gross margins decline toward 35% or below for several consecutive quarters, the software-attached thesis is not working

- Revenue growth deceleration below 20% on a product revenue basis in 2026, excluding StereoLabs contribution. That could suggest the core LiDAR business is facing strong ompetitive pricing pressure faster than the platform can compensate

- Key leadership departure: If Angus Pacala, Mark Frichtl, and/or Cyrille Jacquemet exits within the next 12 months, the founder-driven story doesn't hold anymore

- Balance sheet emergency: If the company announces a large equity raise at a material discount to current prices before reaching EBITDA breakeven, the dilution becomes a serious impediment to long-term returns

- StereoLabs talent loss: If the StereoLabs co-founders depart before the four-year equity vesting period concludes, the intellectual capital that made the acquisition attractive may not fully transfer.

10 - What I am doing

Ouster is a high quality company on track to do very well in the years ahead. For that reason I opened a position at $26.90 and scaled it to a 4.5% of my portfolio after it announced the REV8 product line, which I think is a great step forward in terms of competitive positioning for them. My average cost basis as of the time of writing is $27.10.

Depending on execution I will add to my position as well as significant stock sell-offs unrelated to the business fundamentals. For now I'm steadily building my position which I will keep sub 8% on a cost base.

What would cause me to exit: three consecutive quarters of gross margin deterioration, strong deceleration of growth, or a messy departure from one of the founders.

The thesis will take time to play out so I'm leaning back and see how things unfold. I'm very excited for the road ahead for Ouster and I'm looking forward to keep tracking Ouster's progress.

Thank you for reading, I hope you found this write-up helpful!

None of this is financial advice, just my personal view. Always do your own due diligence before making any investment decision that fits your own risk tolerance and time horizon.

Written by

Sign-up

A weekly newsletter for visual learners to help you invest better

Member discussion