Nvidia earnings recap Q4 2025

Time to unpack yet another great quarter of NVIDIA, covering the numbers, business highlights and what Mr Jensen had to say.

Before diving in the numbers, let's start off with a quote from Jensen on the state of AI:

From an industrial level, because all of our companies are powered by software, and the cloud companies are powered by software, and if the new software requires tokens to be generated and the tokens are monetized, then it stands to reason that their data center build out directly drives their revenues.

He continues:

Compute drives revenues. I think they all understand that. I think people are increasingly starting to understand that as well. Lastly, you know, the benefits that AI produces for the world ultimately has to generate revenues. We’re seeing right in front, being developed, as we stand here, agentic AI has turned an inflection point, and it literally happened in the last couple of two, three months.

In short: businesses use software to generate revenue > Next Gen software requires tokens > Tokens require compute > Massive data center demand (very bullish for names like Nebius by the way).

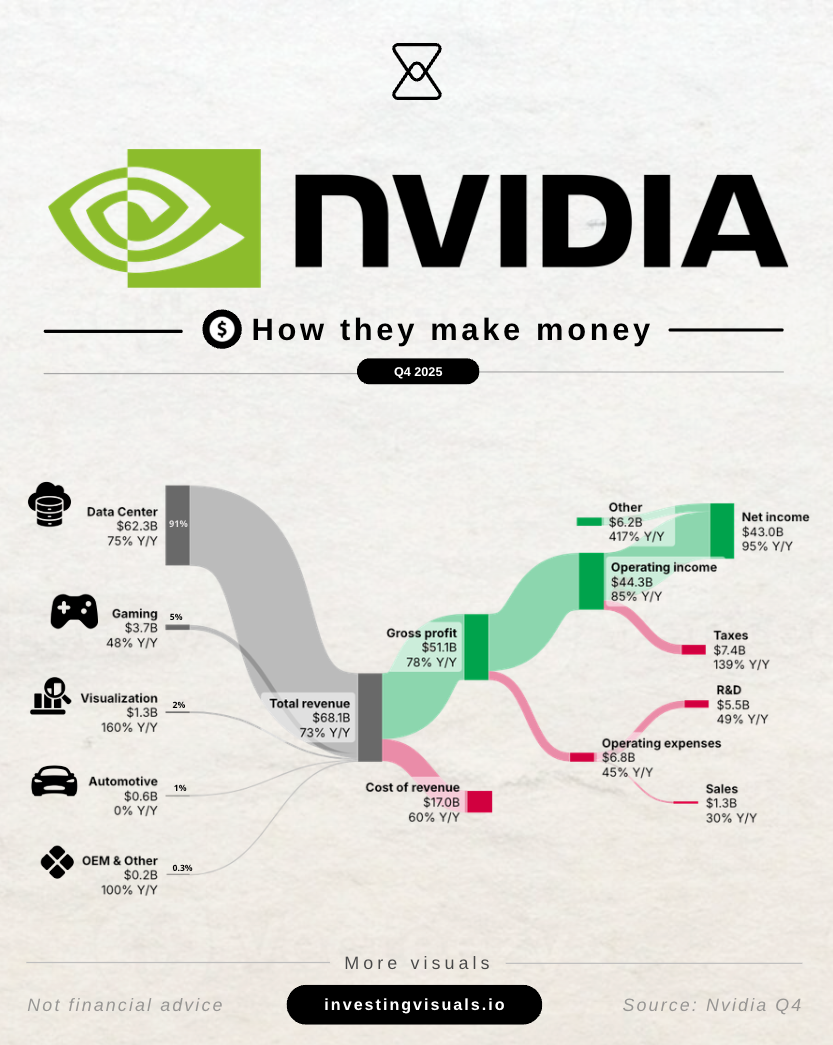

1 - Key numbers

Q4 2025

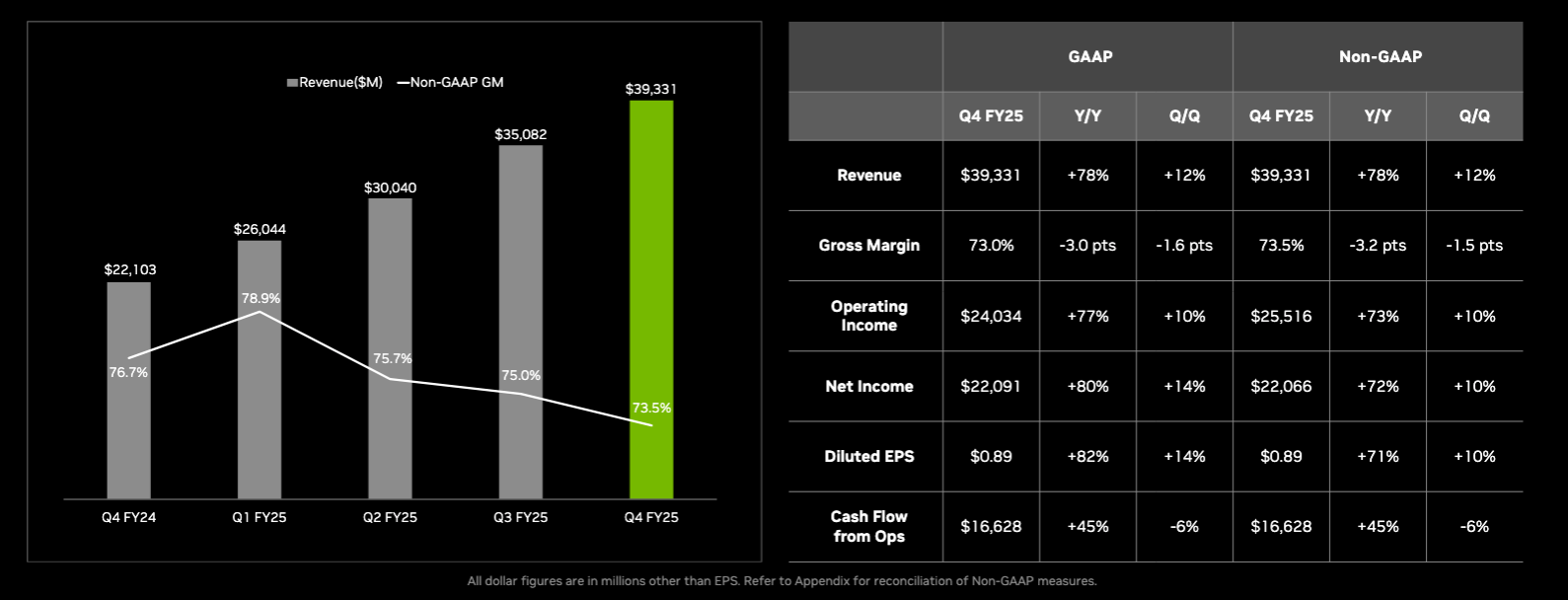

- Q4 revenue: $68.1B, up 20% quarter over quarter and up 73% year over year

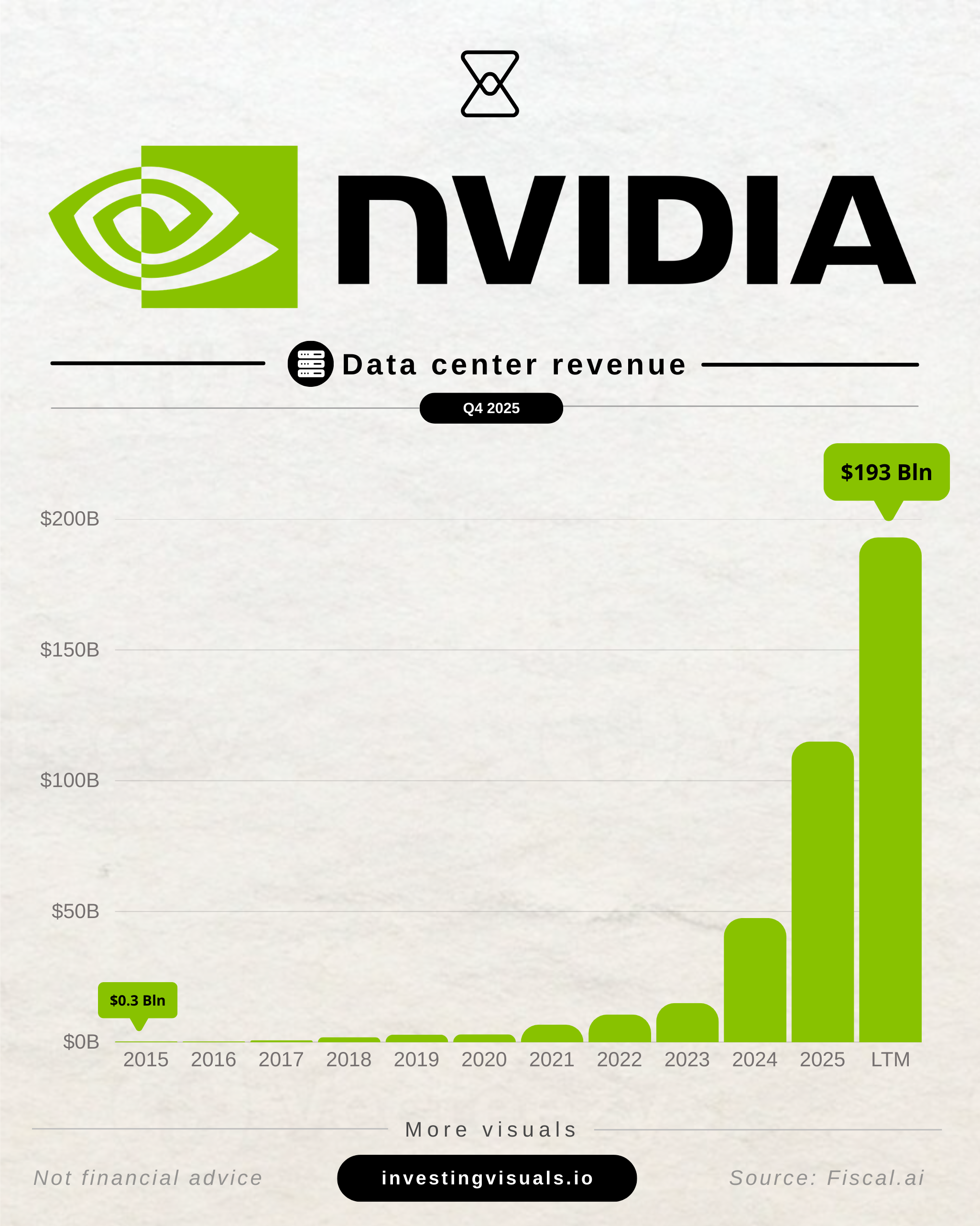

- Q4 Data Center revenue: $62.3B, up 22% quarter over quarter and up 75% year over year

- Q4 GAAP gross margin: 75.0%

- Q4 GAAP diluted EPS: $1.76, up 98% year over year

- Q4 free cash flow: $34.9B

Full years

- FY revenue: $215.9B, up 65% year over year

- FY Data Center revenue: $193.7B, up 68% year over year

- FY GAAP diluted EPS: $4.90

- FY free cash flow: $96.6B

- FY capital returned to shareholders: $41.1B, with $58.5B remaining on repurchase authorization

2 - Guidance

NVIDIA explicitly says the outlook “does not assume any Data Center compute revenue from China.” This is an important nugget because it reduces ambiguity around whether any upside from China is embedded in the guide. They are telling their base case excludes it.

Q1 2026 guidance

- Revenue: $78.0B, plus or minus 2%

- FY tax rate assumption: for FY27, non GAAP tax rates expected to be 17.0% to 19.0% excluding discrete items and material tax environment changes

NVIDIA did not specifically guide for the full year, but CFO Colette Kress did say this on the earnings call:

We look ahead, we expect sequential revenue growth throughout calendar 2026, exceeding what was included in the $500 billion Blackwell and Rubin revenue opportunity we shared last year.

Let that sink in for a bit: "exceeding (...) the $500 billion Blackwell and Rubin revenue opportunity". It already was huge when they announced it, and it's likely to even exceed that. Incredible.

3 - Business highlights

Data center

Data Center revenue was $62.3B, up 22% quarter over quarter and up 75% year over year, driven by continued strength in Blackwell and the Blackwell Ultra ramp.

Management also emphasized broad based demand across cloud providers, hyperscalers, AI model builders, enterprises, and sovereign nations, with supply commitments now extending into calendar 2027.

Networking

Networking produced $11B of revenue in Q4, up more than 3.5x year over year, supported by NVLink, Spectrum X Ethernet, and InfiniBand as customers scale up AI factories.

Jensen reinforced that NVIDIA is increasingly shipping rack scale systems rather than standalone nodes, which naturally pulls more networking into the platform mix.

Gaming

Gaming revenue was $3.7B, up 47% year over year, reflecting strong demand for GeForce RTX 50 Series GPUs and improving supply compared to earlier periods.

Management cautioned that supply constraints are expected to be a headwind for gaming in Q1 and beyond, even with healthy channel inventory.

Pro Visualization

Pro Visualization reached a record $1.3B, up 159% year over year, crossing $1B for the first time as workstation demand benefited from the Blackwell generation.

The quarter included new RTX PRO Blackwell workstation launches, positioning Pro Viz as a meaningful beneficiary of AI enabled creator and engineering workflows.

Automotive and Physical AI

Automotive revenue was $604M, up 6% year over year, with management continuing to frame the segment as an early stage ramp tied to longer cycle design wins.

They also highlighted physical AI as a fast growing category, stating physical AI contributed north of $6B in FY26 revenue and positioning it as the next major inflection beyond agentic AI.

4 - Management commentary

Jensen on inference:

The number of tokens that are being generated has really gone exponential. We need to inference at a much higher speed, and when you’re inferencing at a much higher speed, and each one of those tokens are dollarized, it directly translates into revenues. Inference performance equals revenues for our customers. For the data centers, inference tokens per watt translates directly to revenues.

CFO Colette Kress on data center demand durability:

Q4 data center revenue of $62 billion increased 75% year over year and 22% sequentially, driven primarily by sustained strength in Blackwell and the Blackwell Ultra ramp. With NVIDIA infrastructure in high demand, even Hopper and much of the six year old Ampere based products are sold out in the cloud

It's pretty crazy to see that even six your old Ampere based products are sold out at this point. It really goes to show how much demand there is.

For the full year 2025, we expanded adjusted EBITDA margins by over 200 basis points, achieved the highest free cash flow margin in our history, generated $199 million in net cash provided by operating activities, and turned GAAP net income positive in Q4, demonstrating the profitability of our growth.

CFO Colette Kress on their outlook and pipeline:

We look ahead, we expect sequential revenue growth throughout calendar 2026, exceeding what was included in the $500 billion Blackwell and Rubin revenue opportunity we shared last year. We believe we have inventory and supply commitments in place to address future demand, including shipments extending into calendar 2027

In short: demand is as strong as ever.

5 - Q4 visualized

My take

NVIDIA did what only they can: beat estimates by $2 billion and increase their outlook by just as much. The stock is down 4% at the time of writing this, which I think is mostly because the stock already had a great run and it's just taking a breather right now.

Part of it might also link to the market questioning the durability of hyperscaler CapEx demand. Based on this quarter, CapEx is as strong as ever but it remains to be seen for how long this CapEx cycle lasts.

Which bring me to an important point: 91% of their revenue is now tied to data center revenue and that share is getting higher every quarter. This does increase concentration risks; once data center revenue spend slows, NVIDIA will be directly impacted.

There are no signs that it will in the short run, but I think it's an important factor to take into account.

What to watch from here:

- Data Center sequential growth versus the $78B guide and whether networking continues to scale with it

- Gross margin and free cash flow margin stability. If they compress it might be due to competition increasing

- Any change in the China assumption, since guidance explicitly assumes no Data Center compute revenue from China

All in all: amazing quarter!

As always, none of this is financial advice. This is simply my breakdown of this quarter and my thoughts about it. Always do your own due diligence before making an investment decision that fits your own risk tolerance and time horizon.

Written by

Sign-up

A weekly newsletter for visual learners to help you invest better

Member discussion