My top picks for 2026

Founder led, best in class compounders I believe offer the most upside in 2026.

This is my first “Top picks” article and before diving in, I would like to frame this in the right context. My top picks all share a number of characteristics:

- Benefit from durable growth trends

- Are best in class in their respective sectors

- Fit within my circle of competence

- Have at least 50% upside from today’s stock price

- Are high quality and all founder led (except one)

I will discuss each of my picks and why they made it into the list. I also share the price ranges I believe are reasonable and what has to go right to reach those. I would like to emphasize these are not price targets but rather what I believe are the result of plausible scenarios. A lot can happen in a year, so it will be interesting to review this list when 2026 ends.

Honorable mentions

Before diving into my final list, I would like to start with two honorable mentions, names that did not make the cut but are definitely worth looking into.

TheTradedesk (TTD)

The Trade Desk (TTD) helps advertisers buy and measure digital ads across the open internet, especially in connected TV. It sits right in the shift from traditional TV and manual ad buying toward programmatic, data driven advertising with better measurement.

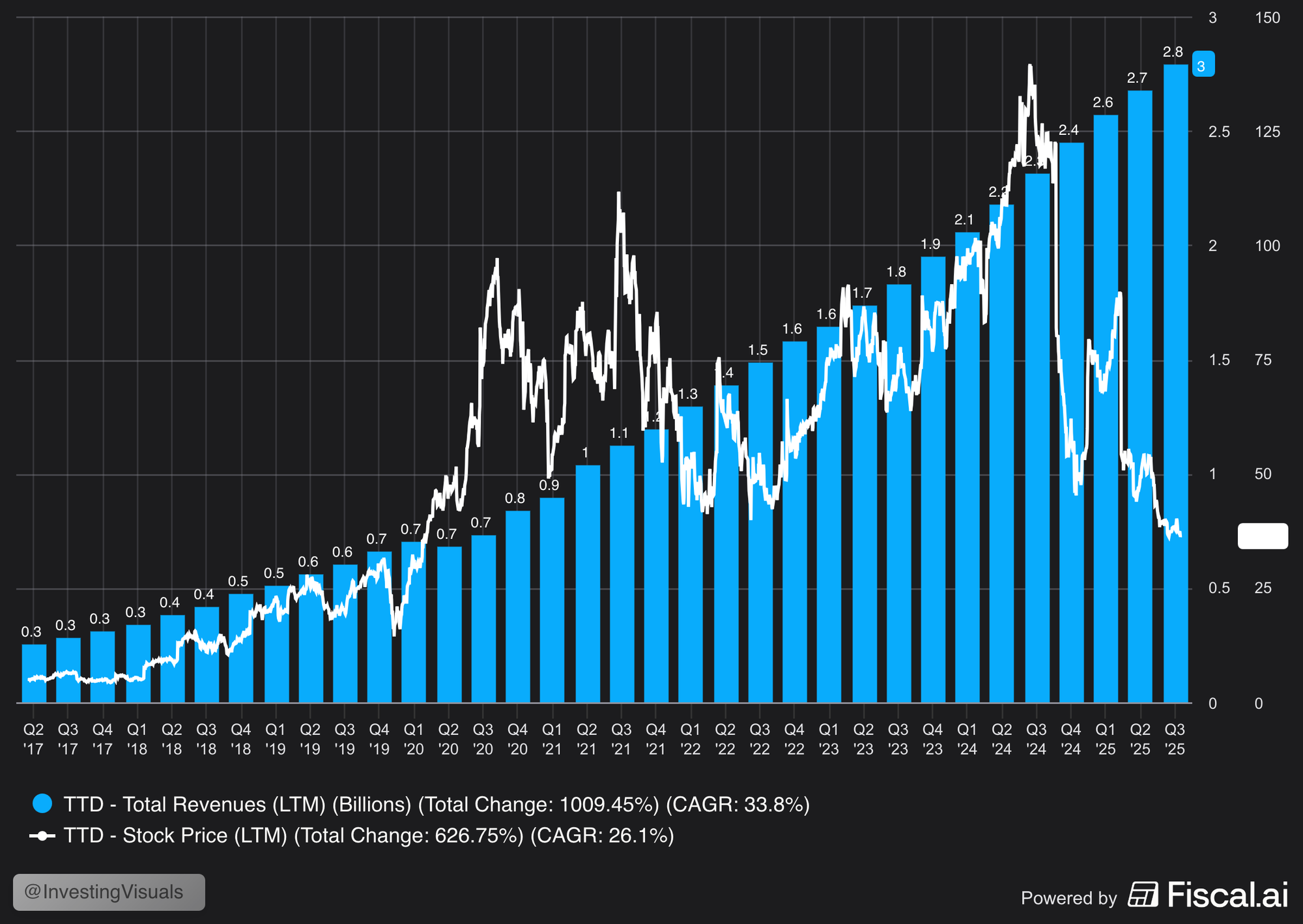

It is also the worst performing stock of the S&P 500 in 2025, down a staggering -68%. So what happened here? Because it looks like a business performing very well based on the chart below with a clear disconnect between stock price and revenue growth.

The stock crash is a combination of factors that caused a perfect storm for TTD.

- Earnings miss: first, TTD got hit for breaking its long running “never miss” reputation when execution issues showed up around the Kokai rollout and near term growth expectations reset.

- Macro pressure: macro pressure, especially during the tariffs, weighed on large brand budgets and added another wave of uncertainty, and a CFO transition did not help sentiment in the moment.

- Kokai 1 rollout: it was bumpier and slower than planned, with migration and execution issues contributing to the rare revenue miss and a sharp confidence reset in near term growth.

- Valuation: TTD traded at 74x forward price to free cash flow before the sell off started, which is high by any standard. Combining the prior three factors with a high valuation is when things get rough and that is what caused the stock crash.

💡

1 Kokai is TTD’s next generation ad buying platform that uses more automation and AI to help advertisers plan, buy and measure campaigns more efficiently across channels like CTV and the open internet.

In short

At today’s price ($36), TTD trades at a 20x price forward free cash flow multiple, which is its lowest valuation ever. They introduced a lot of innovations in the past year, improving their overall product offering. But these innovations need time to ramp.

When they do and revenue re-accelerates, I can see TTD’s stock have a great run from here as sentiment improves, with the stock potentially trading between $50 and $65 (around 60% upside at the midpoint) by the end of the year if they are able to execute. They remain the cleanest way to own the independent “operating system” for the open internet ad market.

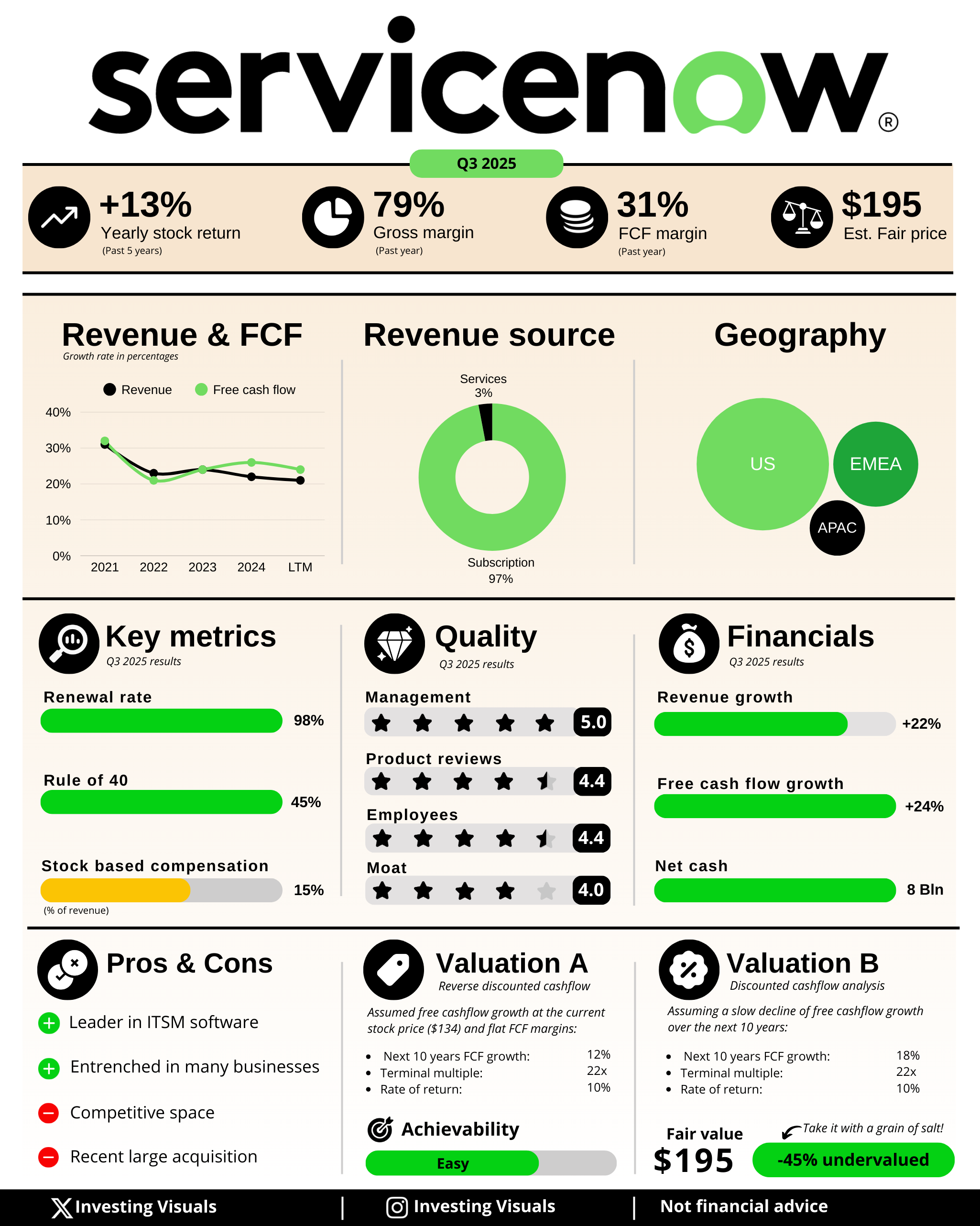

ServiceNow (NOW)

If we are talking about high quality compounders, NOW is definitely one of them. They are the undisputed leader in IT service management and offer a platform that helps large organizations automate workflows across IT and the broader business.

NOW benefits from the long term trend of enterprises standardizing on cloud platforms to digitize processes and drive productivity. They are also very well positioned to benefit from AI, which they can effectively upsell to existing customers.

What I like is their platform economics, huge installed base upsell runway, and a clear path from IT workflows to the entire enterprise, along with AI tailwinds as they become the "control tower of AI" according to CEO Bill McDermott.

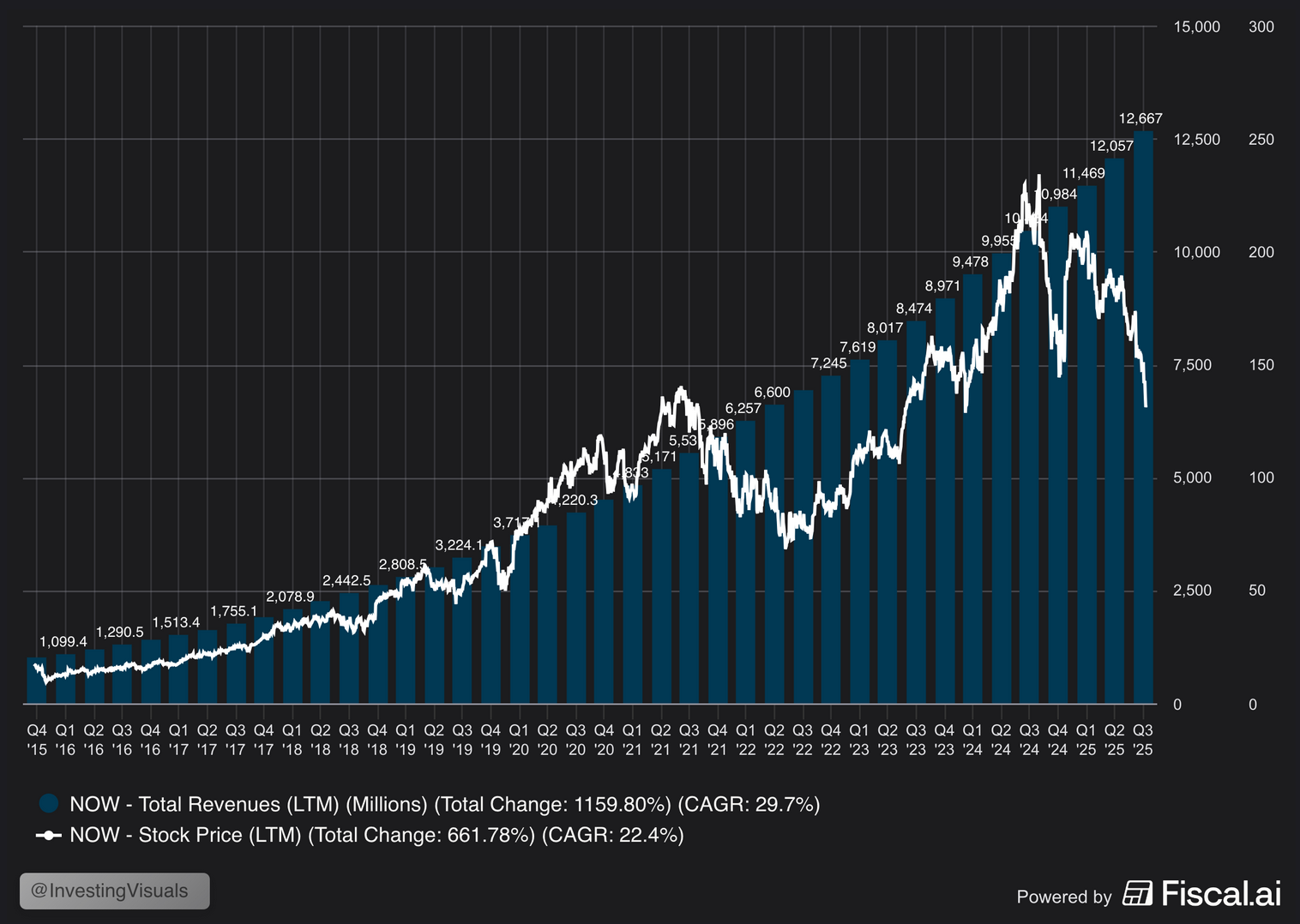

Yet the stock is down nearly 43% from its 52-week highs. So what caused this and is it fundamental or short-term sentiment?

- Expectations reset: A big chunk of the move has been the market repricing ServiceNow after softer forward outlook periods, especially around subscription growth expectations and the pace of AI related upside showing up in near term numbers

- Multiple compression across software: Even when fundamentals stay solid, software has gone through a hard valuation reset. More on that in this article. Investors rotated toward other parts of AI and started discounting the risk that new AI tools could pressure legacy software value capture, which hit premium multiple names like NOW harder

- Narrative and risk overhangs: There have been a couple of confidence overhangs that added fuel to the selloff, including investor concern that ServiceNow might lean more on M&A to sustain growth (Armis acquisition), plus a high severity security issue in its AI platform (now solved).

In short

NOW is a very high quality software business which is dragged down along with the entire software sector. They are however one of the businesses I believe can benefit greatly from AI, instead of being disrupted by it, mainly due to their huge installed base upsell runway.

Right now the risk/reward is very attractive with the business trading near a decade low valuation. With strong execution and new AI features gaining traction, I believe NOW could trade between $190 - $210 by the end of the year, presenting 41% to 56% upside from today's price.

My top 5 picks for 2026

While the two honorable mentions are very high quality businesses, they didn’t make the cut for my top 5. What comes next are the names I believe offer the best risk reward for 2026.

I’ll share why each company earned a spot, the price ranges I personally consider reasonable, what has to go right for the upside to play out, and a one pager summary for each pick so you can grasp the thesis quickly.

I’ll also be transparent about how I’m positioned and what I’m doing with my own portfolio. Let's dive in!

#5 - Duoling (DUOL)

This post is only for subscribers on the

Premium and Supporter tiers

Subscribe to continue reading

Written by