MercadoLibre earnings recap Q4 2025

MercadoLibre posted a great Q4 2025 but the stock dropped nonetheless. Let's find out why that is and if Mr. Market is right or not.

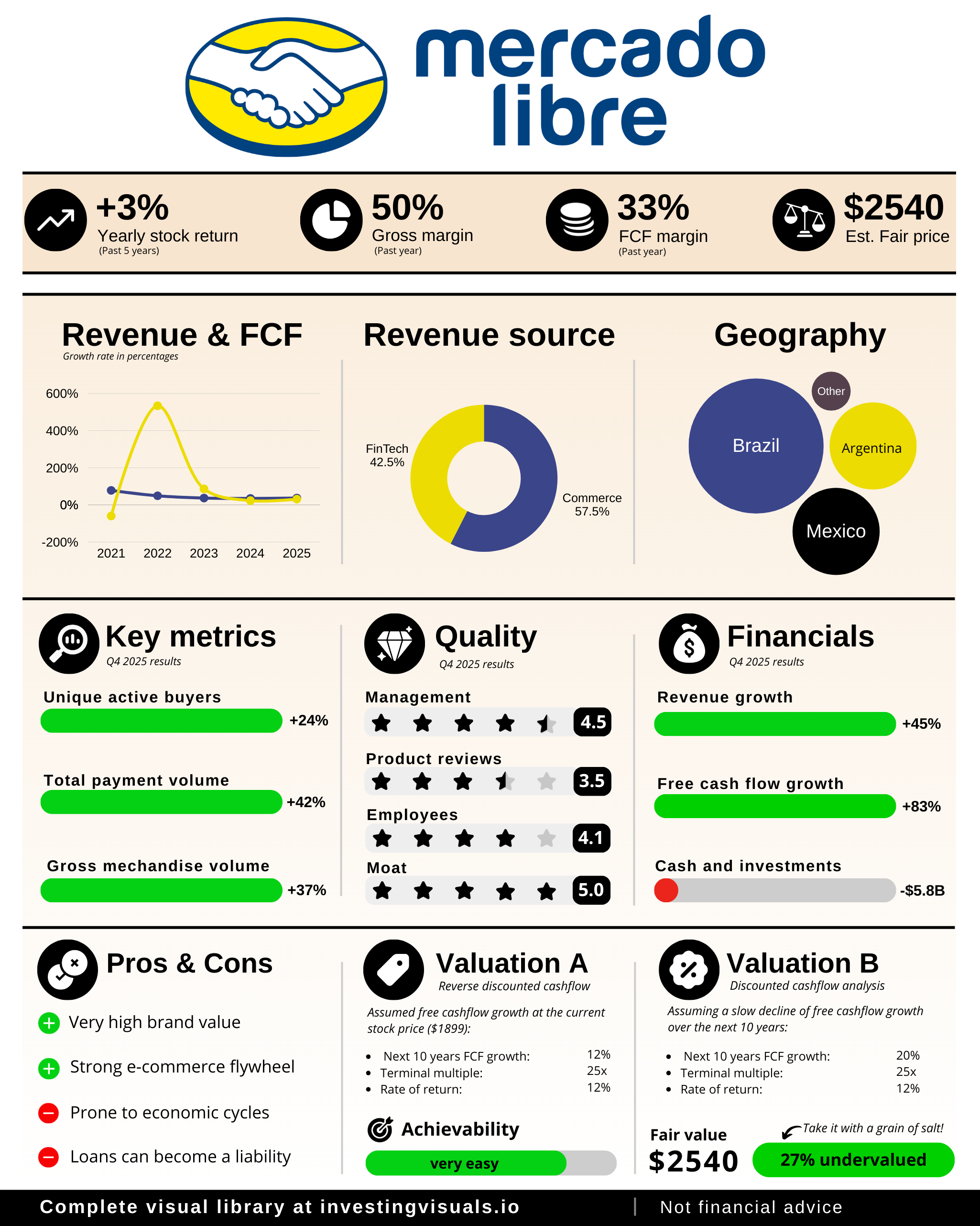

MercedoLibre is one of those businesses that keeps compounding no matter what. The business they are today is more than just E-commerce or FinTech. Each of their business units interlock to create a very strong flywheel.

Management’s message was consistent across the shareholder letter and the earings call. They are seeing opportunities such as structural underpenetration across Latin America, and they are willing to invest ahead of profitability if it strengthens long term scale. “We do not solve for short term margin optimization.”

1 - Key numbers

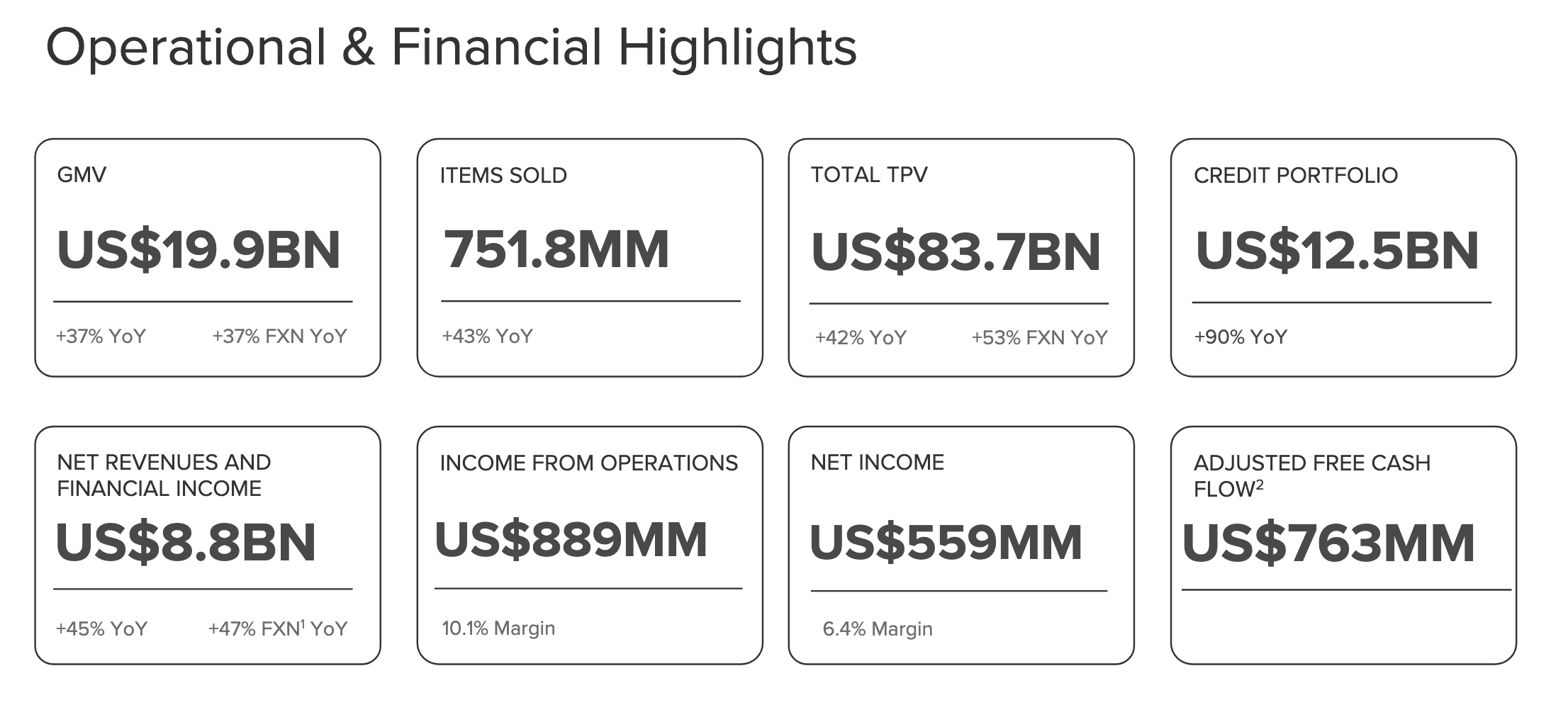

- Net revenues: $8.7B in Q4, up 45% YoY

- Gross profit: $3.784B in Q4, with 43.2% gross margin

- • Adjusted free cash flow: $763M in Q4 and $1.481B in FY 2025

E-Commerce

- Gross merchandise volume : $19.906B in Q4, up 36.8% YoY

- Unique active buyers: 83.2M in Q4, up 23.6% YoY, and 121M in FY 2025

- Items sold: 751.8M in Q4, up 43.1% YoY

Payments

- Total payment volume: $83.694B in Q4, up 42.1% YoY

- Total payment transactions: 4,506M in Q4, up 35.5% YoY

FinTech

- Monthly active users: 77.9M in Q4, up 27.3% YoY

- Assets under management: $18.810B at Q4 end

- Credit portfolio: $12.508B at Q4 end, up 90.3% YoY

- Net interest margin after losses: 23.3% in Q4

2 - Guidance

I can be short in this one: MercedoLibre does not guide, never has :)

But they did gave some forward looking nuggets:

- Investments for 2026: “Our investment plan for 2026 will be consistent with this bold and disciplined approach to investing behind long term growth.”

- Margin tradeoff: “the combined impact of our strategic investments… was equivalent to 5 to 6 percentage points of operating margin in Q4’25.”

- CEO transition: Ariel Szarfsztejn became CEO and founder Marcos Galperin became Executive Chairman, with Marcos “remaining closely engaged on key strategic priorities.”

3 - Business highlights

Commerce

Commerce accelerated with Q4 GMV up 36.8% YoY and items sold up 43.1% YoY, driven by stronger conversion and retention after the lower free shipping threshold in Brazil.

Logistics and selection investments supported that momentum, with same and next day shipments up 29% YoY, Brazil unit shipping costs down 11% in local currency, and cross border GMV up 74% FX neutral as China fulfillment ramps.

Fintech

Fintech kept expanding its role in the ecosystem, with total payment volume up 42.1% YoY and monthly active users up 27.3% YoY to 77.9M. Credit scaled aggressively with the portfolio up 90.3% YoY to $12.508B and nearly 3M credit cards issued in Q4, while profitability remained supported by net interest margin after losses of 23.3%.

Advertising

Advertising revenue grew 67% FX neutral YoY in Q4, reflecting better tooling and a stronger tech stack rather than a single one off driver. It is still early relative to the marketplace opportunity, and management frames it as a something that'll have a long runway for monetization for their e-commerce business.

4 - Management commentary

In the shareholder letter they opened with, “Mercado Libre’s ecosystem is stronger than ever,” and tied that to record Net Promoter Scores (NPS) across Commerce and Fintech in Brazil, Mexico, and Argentina with a strong focus on customer experience.

Management on margin compression: "The margin compression reflects our decision to invest in key long term growth opportunities". They estimate the combined pressure from the lower shipping threshold, cross border, 1P, and credit card was 5-6% points of operating margin in Q4.

5 - Q4 visualized

My take

MercadoLibre is being MercadoLibre: an incredible business firing on all cylinders. My guess is the market is selling the stock due to the margin compression, which management highlighted is driven by their strategic long term investments. In other words, they’re prioritizing long term gains over short term profits.

MELI is in a deliberate reinvestment phase where multiple growth bets are compounding at the same time, and management is choosing to fund that rather than optimize margins for the quarter. That vision is what made MELI the business they are today, so I can fully support it as a shareholder.

My main 'concern' right now is their credit portfolio, which is expanding rapidly. I know they’re being diligent, but it does introduce more credit risk as the portfolio grows. Definitely something to keep an eye on. Also, if margins compress due to competitive pressure on top of the margin compression due to long term investment, the thesis might start to show some cracks, but so far I've not seen any of that materialize.

I’ve been holding MELI since 2021 and this quarter once again confirmed my thesis. My latest buy was back in November at $1960, and I do believe the stock is attractively valued right now. You can view my full buy and sell history in the live dashboard my portfolio.

Thesis on track?

Definitely! MercadoLibre is doing the right things and investing in future growth at the expense of short term margin compression. Nothing I personally worry about given their track record so far. Great business, great quarter.

As always, none of this is financial advice. This is simply my breakdown of this quarter and my thoughts about it. Always do your own due diligence before making an investment decision that fits your own risk tolerance and time horizon.

Written by

Sign-up

Get the latest updates and news in your inbox

Member discussion