How I think about capital allocation

1 - Introduction

A little while ago, Simon (a community member) and I had a chat about capital allocation. That conversation inspired me to write this article, sharing my thoughts and process around this subject. I’ll cover examples of positions I closed and why, what I bought instead, and mistakes I’ve made in the past.

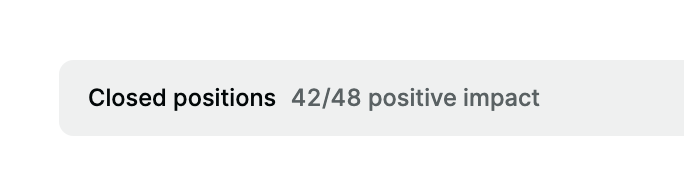

Since I started tracking my portfolio, I’ve owned 61 positions in total. I currently hold 13 and have closed 48. Of those 48 closed positions, 42 had a positive impact on my returns. That means that in 87.5% of the cases where I decided to close a position, it turned out to be the right call because my overall portfolio performed better than the position did after I sold it.

It’s a really neat feature of the platform I use to track my portfolio. You can read more about it here if you’re interested.

2 - My portfolio

I like to think of my portfolio as a way to convert research and patience into returns. And I don’t want it to get clogged with average businesses that could do “fine”.

I want to hold high-quality businesses that I believe are winners in their respective industries, primarily in tech, and that can realistically double their stock price in 3 to 5 years, resulting in a minimum CAGR of 20%.

That’s why my investment framework is so important. It helps me sift out the “best” from the “fine”. It’s not flawless, but it does help me build conviction early on, know what I own, and stick with it (or buy more) when the stock tanks while the underlying business continues to do well.

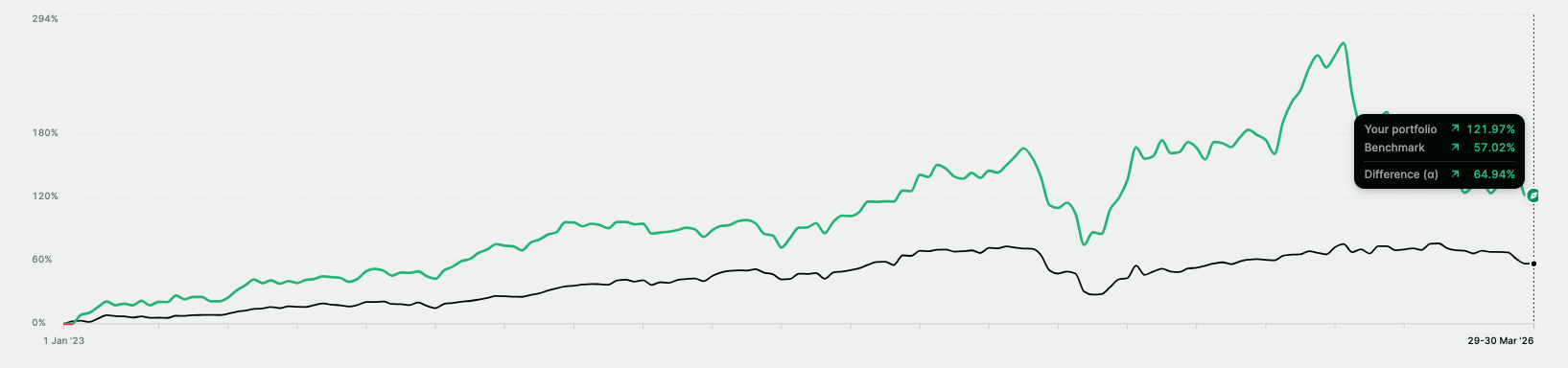

Having a process like this has helped me outperform the broader index by a wide margin, even though many of my current positions are experiencing major drawdowns of more than 30% in the broader tech sell-off over the past months.

3 - My investment philosophy

“Own great companies and hold them as long as they remain great” is my personal investment philosophy.

I use a “buy and verify” approach: craft a thesis after doing thorough research, build a position over time, and verify whether that thesis is playing out or not.

I’m a long-term investor looking to hold positions for years, but that doesn’t mean I’m passive. On the contrary. Long term in this sense is a time horizon, not a loyalty oath to the positions I hold.

As long as the thesis is on track, I’ll hold on to my position and, depending on the size, valuation, and potential of the business, decide whether to increase it over time. Usually up to a total size of around 12% of my portfolio on a cost basis. But there’s one major factor I take into account as well: opportunity cost.

💡

Opportunity cost: the potential benefit, profit, or value lost when choosing one alternative over another.

4 - Opportunity costs

There’s a vast ocean of companies I can invest in, but only so many I actually want to hold. As I learn more about businesses and industries, my investable universe expands and new opportunities arise.

That can mean I come across a business that I believe has more potential than something I already hold in my portfolio. A great example is CrowdStrike versus dLocal.

CrowdStrike is a fantastic business that I’ve held since 2021 at an average cost of $178. But midway through last year, I learned about dLocal (DLO), which checked a lot of boxes for a high-quality business with a lot of potential.

At the same time, CrowdStrike was trading at a very high multiple relative to its growth rate, so I decided to sell my shares at around $504 for a gain of 311% and buy DLO instead. At the time of writing, CrowdStrike is down 27%, while DLO is up 6%, representing 33% alpha.

A question I continuously ask myself is when sifting through the investable universe:

“Does this business deserve the spot more than what I already own?”

If the answer is yes, I will rotate my capital into that new opportunity.

The main takeaway here is that I don’t necessarily need a broken thesis to sell a position. Sometimes I simply see a better opportunity elsewhere.

An important side note is that I only invest in what I truly understand. I’ve been working in the tech industry for over 10 years, so these are the businesses I primarily focus on.

It’s a process I’ve learned to apply over time, because when I first started investing, I basically rotated in and out of positions on gut feeling. I really can’t recommend that, because it caused me to sell some major winners.

5 - Winners I sold too early

Tesla

My biggest mistake was selling Tesla in 2020 for a gain of around 340% after buying it at $20 split-adjusted back in 2019. If I had held that stock until today, it would have been a 23-bagger.

At the time, I thought I was a genius for buying it early and selling it after a big run. But in reality, I missed out on much better returns by not being more patient. The thing is, I sold based on gut feeling, not because the thesis was broken or because I saw a clearly better opportunity elsewhere.

ASML

Another, more recent example is ASML. It was a core position that I held since 2022 at an average cost basis of $680 and sold at an average of $923. My reasoning was that there was still good upside, but not great upside.

Since then, ASML's stock has appreciated another 50%.

The stocks I bought instead were Nebius and dLocal, both of which are down about 10% since I added to those positions. It's worth noting that we're talking about a time frame of roughly six months here, which is extremely short. It will be interesting to see how this plays out two to three years from now.

There are more winners I sold too early, which you can view in my portfolio, but the lessons are the same: let winners run and, if not, at least make a well-considered decision to sell with clear reasoning as to why.

Closing remarks

There's a lot more I could say about this subject, but I don't want to make this too long of a read. So here are a few closing remarks to wrap it up:

- I treat my portfolio like it has limited seats. That way, a new name has to compete for an existing seat, which makes me extra critical of both my current positions and new opportunities

- I size based on conviction, not symmetry. If I genuinely believe in a business, it should be sized that way

- I let my winners run and let my portfolio concentrate itself. A great example is Nebius, which became a multibagger after I bought it early last year and is now my largest position by a mile

- I take my time. I can love a business and still not buy it. I'll keep it on my watchlist and, once I think the price is right, I'll jump in. I can feel FOMO like everyone else, but I've learned from experience that FOMO can be a very dangerous thing

- Valuation is important but not decisive. Valuation alone is often a poor reason to sell an exceptional business or buy a mediocre one. Great companies usually look expensive on the way up and tend to stay that way as they continue to execute

Thanks for reading!

~ Jan

As always, none of this is financial advice. Always do your own due diligence before making an investment decision that fits your own risk tolerance and time horizon.

Written by

Sign-up

And receive the latest visuals and articles straight to your inbox

Member discussion