Duolingo: the stock the market hates (Q4 earnings recap)

There are very little stocks that have experienced a drawdown like Duolingo is currently going through and Q4 2025 is putting even more pressure on the stock. This earnings recap is aimed to shed light on all the moving pieces and my take as a DUOL shareholder.

If you truly want to understand the business and if it could be an interesting investment, you can read my full deep dive here:

First the key numbers for Q4, which looked excellent:

1 - Key numbers

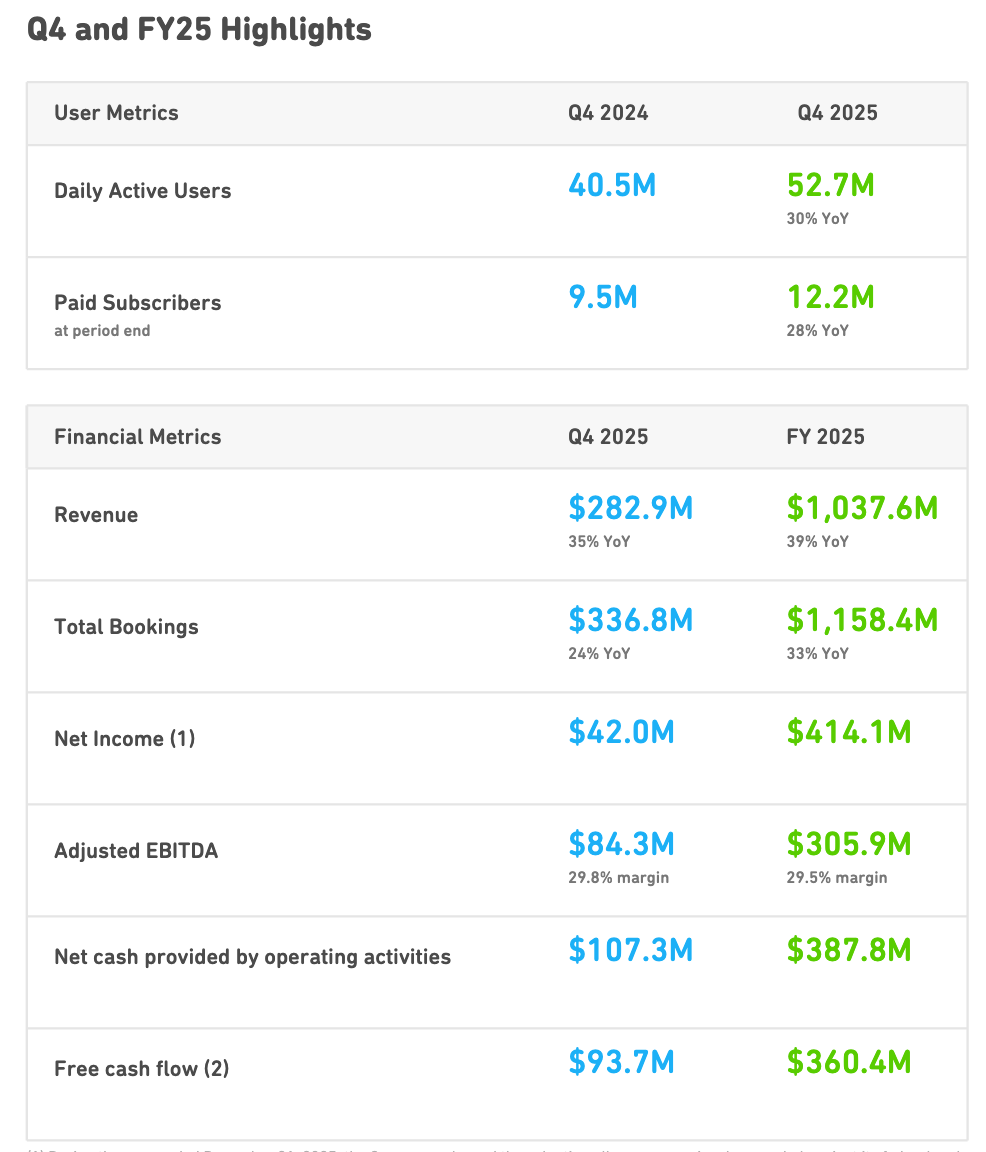

Q4 2025

- DAUs 52.7M, up 30% YoY

- MAUs 133.1M, up 14% YoY

- Paid subscribers 12.2M, up 28% YoY

- Revenue $282.9M, up 35% YoY

- Total bookings $336.8M, up 24% YoY

- Subscription bookings $296.6M, up 25% YoY

- Free cash flow $93.7M, 33.1% margin

- Cash and cash equivalents $1.04B, no debt

- Share repurchase authorization up to $400M

FY 2025

- Revenue $1.0376B, up 39% YoY

- Total bookings $1.1584B, up 33% YoY

- Net income $414.1M, includes a one time income tax benefit of $256.7M

- Adjusted EBITDA $305.9M, 29.5% margin

- Free cash flow $360.4M, 34.7% margin

2 - Outlook

This is where thing went 'sideways':

Q1 2026 guidance

- Bookings $301.5M, about 11% YoY growth

- Revenue $288.5M, about 25% YoY growth

- Adjusted EBITDA $73.6M, 25.5% margin

FY 2026 guidance

- Bookings $1.274B to $1.298B, 10% to 12% YoY growth

- Revenue $1.197B to $1.221B, 15% to 18% YoY growth

- Adjusted EBITDA $299M to $305M, about 25% margin

3 - Business fundamentals

On many objective metrics, DUOL is a business in very good shape. They have $1B in net cash, and 2025 was an amazing year. But we all know the stock tells a very different story. It’s a great example of how the market is forward looking. And it’s exactly in that forward looking dynamic where things look different from what investors are used to seeing from $DUOL.

On the earnings call, management made it very clear they do not want to squeeze every dollar out of their existing user base given the opportunity ahead. Instead, they want to “expand the pie” with the ambitious goal of reaching 100M users by 2028. But that comes at a cost, which is reflected in the bookings guidance. They guided for 12% bookings growth, which is a significant deceleration.

4 - Guidance in more detail

Management on the outlook: “We designed the guidance to do the right thing for our customers and experiment with what works best.”

They emphasize expanding the pie using AI capabilities to unlock a larger opportunity. How they plan to reach 100M users:

- Teach languages better

- Improve the free user experience, based on 15 years of experimentation

- Invest in growth engines like Chess, now at 7M DAU after launching last year

- Increase marketing spend and R&D investments

“If we can get to that DAU and reasonable monetization assumptions, we could be looking at a $2.5B annual revenue business.”

That is 2.5x DUOLs 2025 revenue.

“We are really motivated to go for the bigger prize. In terms of when you are going to see it, we modeled it later in the year, so it will take a little while."

5 - Monetization

Management also mentioned additional monetization opportunities. Only about 10% of users are currently monetized, and they believe they can do much better. Potential levers include:

- Better ads

- Character customization

- New features

- Monetizing additional subjects

6 - Market saturation and competition

CEO and founder Luis von Ahn: “We are not worried about either. We have about 85% of the DAU of learning apps in the world, which has been basically flat for a while now.”

“If we can get to 2% penetration in every country, using the US as a reference, we would double our DAU.”

7 - Is AI eating into user growth?

On whether AI is driving DAU deceleration, Luis noted that AI translation has been nearly perfect for years. Users come to DUOL for two main reasons:

- As a hobby, they genuinely want to learn

- To learn English

From user exit surveys, AI does not show up as a reason for churn. The main reason users leave is that they are busy. In other words, they spend more time on social media.

8 - The bet you must be willing to make

Management is deliberately sacrificing short term revenue growth and margins to chase longer term opportunities tied to a much larger monetizable user base. But user growth must reaccelerate at some point to reach the 100M target. If it does not, the deceleration and margin compression are not justifiable.

On the flip side, if they pull this off, DUOL could be a significantly larger business a few years from now than it is today.

You must be willing to take the long view and trust management to execute. The trajectory is less predictable than it used to be, and the market is repricing that uncertainty.

9 - My take as a shareholder

First, credits to management for being transparent about their plan and its impact on the earnings call. I think many companies could learn from how this team communicates with analysts.

It is clear that DUOL is prioritizing long term growth and user value over short term profits. As a long term investor, I love to see that. If they execute, DUOL could become a much larger business with:

- A: a larger monetizable user base

- B: a more efficient monetization engine

But it introduces uncertainty around how and when this plays out. And if there is one thing the market hates, it is uncertainty. I think that short-term question mark is reflected in the sell off.

As an investor, you have to bet on management execution and think in years, not quarters for this to work. Even though I am holding the DUOL bag I have decided to keep my shares and see how this plays out.

I trust management, given their track record so far, and believe in the long term opportunity. The stock is already repriced for the material bookings slowdown, which in my view limits downside from here.

If management cannot pull this off, I will take the loss. If they can, we might see new highs. But it will take time and patience. Which I have. I would not be a long term investor if I chased quarters.

I hope you found this helpful. Disclaimer: as of the time of writing, I own a 4% position in Duolingo.

Best!

~ Jan

As always, none of this is financial advice. This is simply my breakdown of the quarter and my thoughts on it. Always do your own due diligence before making an investment decision that fits your risk tolerance and time horizon.

Written by

Sign-up

And receive the latest visuals and articles straight to your inbox

Member discussion