Duolingo Q3 2025 earnings review

Duolingo recently released their Q3 2025 numbers and the stock dropped 26% despite strong numbers. So what is going on here and is the stock drop an opportunity or a value trap?

In this review I'll share:

- Key numbers

- Earnings call nuggets

- Reasons for the stock sell off

- My verdict

1 - Introduction

Duolingo (DUOL) is a consumer subscription business focused on helping people learn. It started out by primarily focusing on languages and gradually added more categories to the mix.

They use a "freemium" model that uses a free product with smart gamification to drive daily engagement, convert the most motivated users into paid plans, resulting in a scalable, high margin business model that improves as content and personalization get better over time.

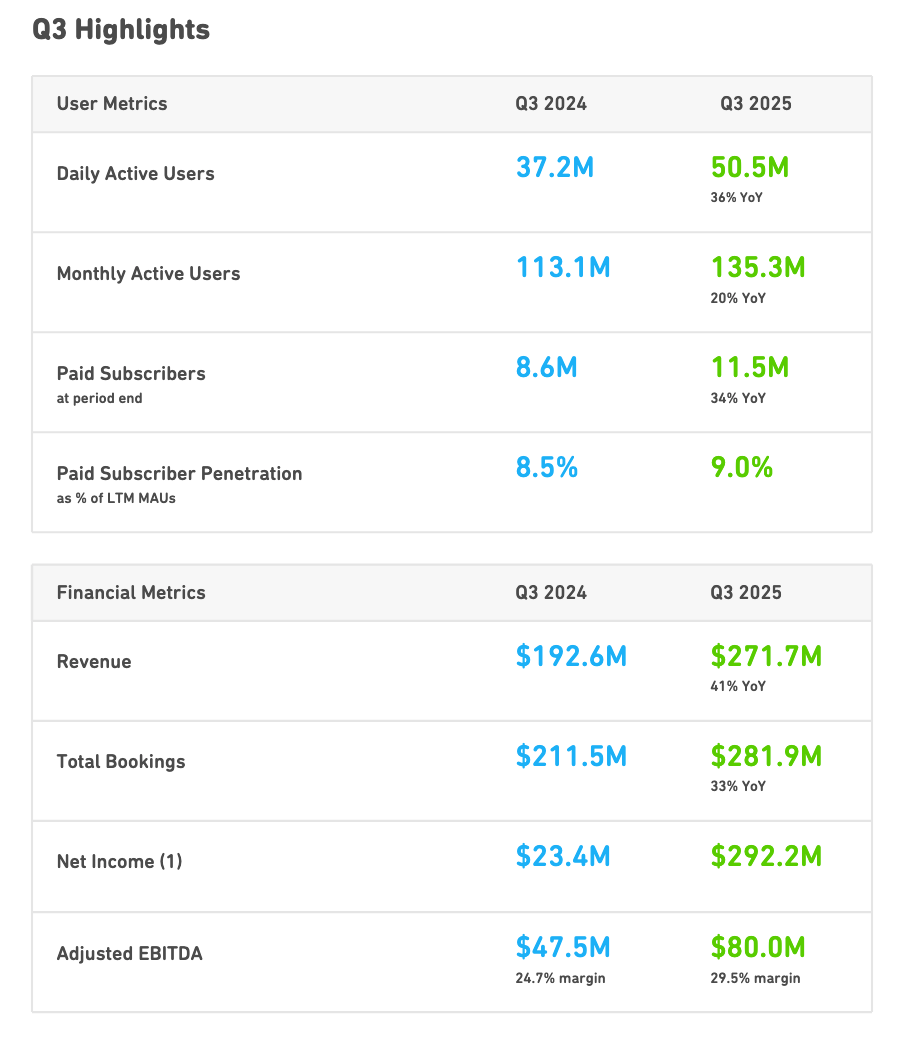

2 - Key numbers

Q4 guidance vs Street

- Q4 bookings guide was $329.5M to $335.5M vs about $343.6M expected (miss).

- Q4 revenue guide was $273M to $277M

Full year guide

- FY 2025 bookings at the midpoint to $1,151M to $1,157M.

- FY 2025 revenue guide was $1,027.5M to $1,031.5M.

- FY 2025 adjusted EBITDA margin guide was about 29% at the midpoint

2 - Earnings nuggets

Duolingo & AI

Duolingo’s AI story is mostly about two things. Max adoption and teaching efficacy. A quote from Luis von Ahn that captures their strategy shift towards AI:

“We believe AI will fundamentally transform education, and we have line of sight to building a product that teaches better than ever before.”

Max performance

Their relatively new Max subscription tier is down well, but it actually under performed management expectations:

“Max is now 9% of our subscribers. It doubled in Q3 year over year in terms of bookings. It’s clearly doing well in that regard. It’s underperforming our lofty expectations for it, though.”

Moving forward, they expect guided Video Calls to be a big driver of future Max tier plan conversion.

AI costs

With AI, the cost of revenue has gone up, linked to inference and infrastructure costs. Luis von Ahn on this topic:

“Most of our AI features, at least the ones that cost the most money, are behind Duolingo Max. And because the price of that is high enough that for us, the usage of AI is anyways profitable.”

3 - Possible reasons for the sell off

3.1 - User growth over monetization

In Q3, management announced a strategic shift: prioritizing long-term user growth over short-term monetization. Previously, Duolingo focused on converting free users into paying subscribers. Something they’ve executed exceptionally well.

Now, the focus shifts to expanding the overall user base, especially as AI opens new opportunities. As management put it, “We think we’ll become a much bigger business in the long term.”

3.2 - Subscription booking growth slowing

Bookings are an important part of the equation. They represent paid subscriptions for future months, while revenue is recognized gradually over time. Bookings growth is expected to slow to 22% in Q4, down from 36% this quarter. This deceleration, combined with the new strategic focus, likely explains the sharp stock drop.

The key question is whether the slowdown is simply a byproduct of this shift or a sign of deeper fundamental weakness. The next few quarters should answer that.

If daily active users (DAU) and monthly active users (MAU) reaccelerate, the shift will be validated. If not, that’s when cracks could start to show. So far, Duolingo's track record in converting free users to paid ones has been outstanding, so I see no reason to doubt their ability to execute for now.

3.3 - Guidance

Management guided for 31% revenue growth in Q4, down from 41% in Q3. They are known for conservative forecasts, so ~35% growth seems more realistic. Still, it’s worth keeping an eye on.

4 - Management highlights

Taking the long view is now their main strategy. “In Q3 we decided to shift the balance towards longer term initiatives.”

Luis explained the why: If AI helps them teach like a tutor and stay more engaging, they think they can move from hundreds of millions of users to billions over time.

Product velocity across new subjects is picking up

Chess is already “the fastest growing course” they have launched, and they are rolling out player versus player. They also laid out a packed Q4 roadmap including flashcards, guided video calls, Year in Review, and the New Year promo.

5 - My verdict

Management is clearly playing the long game, trading short-term profitability for user growth. If this strategy drives stronger engagement and future monetization, this sell-off could turn out to be a great opportunity rather than a value trap.

However, if bookings continue to slow meaningfully without a clear reacceleration in DAU and MAU, that might signal real cracks in the long-term story. The next quarter will be key in determining which scenario plays out.

What I'll be doing

What I love to see as an investor is that Duolingo has a long-term mindset and is doing everything it can to improve the lifetime value of its users. With a great product, revenue ultimately follows as loyal customers reward you over time.

My take is that management sees a clear opportunity ahead and wants to act on it. The narrative they’ve presented is that they’re sacrificing short-term profit for long-term gains. Given their track record, I have no reason to believe otherwise.

However, there are some key points to track to see if that narrative plays out. DAU and MAU should show meaningful growth, and bookings shouldn’t drop too much. If DAU and MAU fail to grow meaningfully while bookings continue to slow, that’s when cracks could start to appear in the thesis. It would signal that their strategy isn’t working and that deeper fundamental issues might be emerging.

So, does this warrant a 20%+ stock drop? In my opinion, no. It feels exaggerated. After the drop, Duolingo trades at an all-time low forward FCF multiple of around 20x. To me, much of the “bad news” is already priced in. Whether this becomes a buying opportunity largely depends on your trust in management to execute: sacrificing short-term bookings for long-term growth in DAU, MAU, and ultimately scale. For me, it’s a matter of patience and letting the story unfold.

As always, none of this is financial advice. Always do your own due diligence before making an investment decision that fits your own risk tolerance and time horizon.

Written by

Sign-up

And receive the latest visuals and articles straight to your inbox

Member discussion