paid only

Introduction

"The investors chief problem - and even worst enemy - is likely to be himself" ~ Benjamin Graham.

I love this quote because it hits the nail on the head: Investing can, to a large extend, be a battle with yourself. The fear of mission out, panic selling, feeling down or angry when your portfolio gets a hard hit. These are all normal feelings and part of investing, but they can really hurt your returns if you don't know how to deal with them.

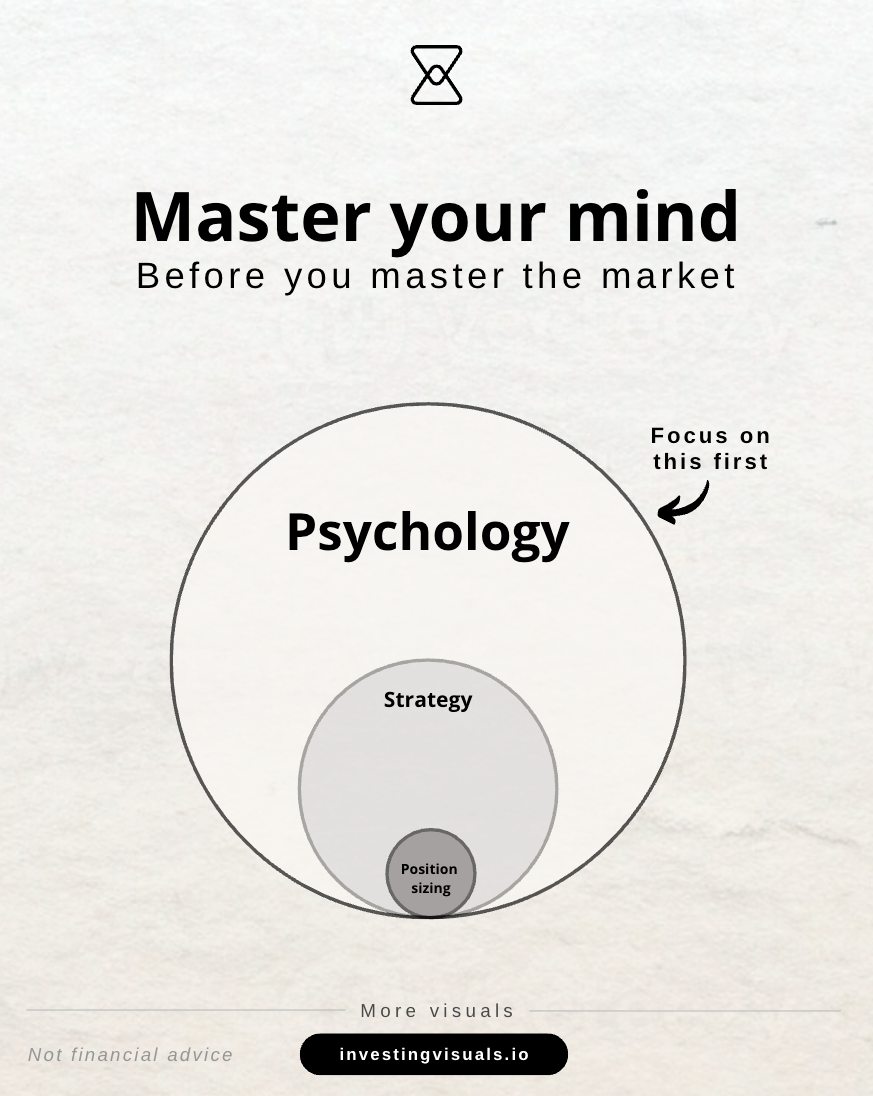

Throughout my investing journey, I learned how important it is to master my mind before mastering the market. Most of us start with the idea that we’ll pick a handful of great businesses (or ETFs), hold them for years, and let time do the heavy lifting as returns compound.

But in reality, things are much harder.

In this article, I’ll cover biases we can easily fall prey to, what they look like in practice and how to fight them, so you know what to do when they show up (and trust me, they will).

1. Confirmation bias

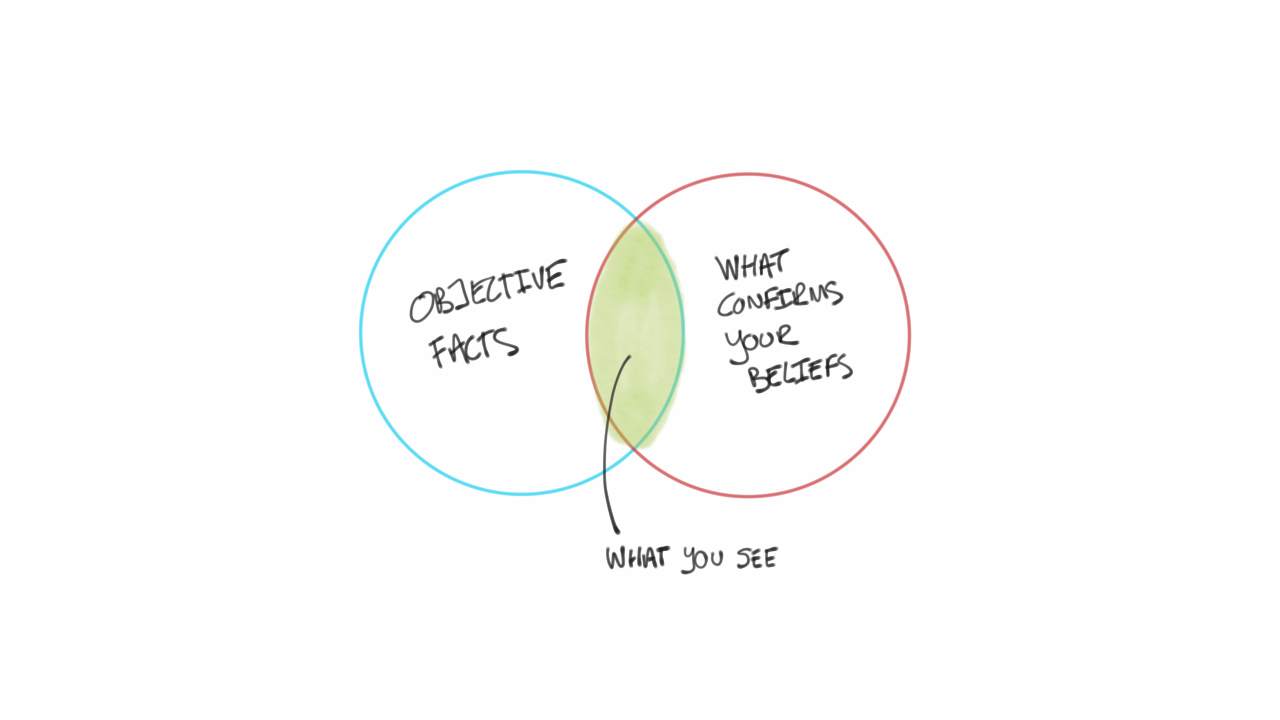

Confirmation bias is the habit of protecting your current belief instead of testing it. You interpret new information as supportive, even when it’s not. You seek out voices that agree with you and avoid the ones that challenge you.

It tends to show up right after you buy. A good test is to ask yourself whether you’re thinking differently about a business after you hit the buy button than you did before.

It’s a very common pattern. You feel excited about the thesis. You want it to work. So when the first crack appears, you might not ask yourself: what changed? This is where you end up with a position deep in the red and still cling on to it, even though the original thesis is busted.

How to prevent it

Something that works for me is to write a bear case before I buy, while I’m still emotionally neutral. Nowadays I always think about what can go wrong before I invest. And it’s perfectly fine if an investment doesn’t work out the way you thought it would. We’re not all knowing and we can’t predict the future. It shows true character when you’re able to admit mistakes and move on.

Thinking about what could happen that would make you reconsider your investment helps you move swiftly when things don’t turn out as expected. Remain open minded to other perspectives, even if they might not align with your view.

2. Bandwagon effect

The bandwagon effect is when the crowd becomes your primary source of information and drives how you feel about an investment. You buy because others are buying. You hold because others are holding.

It’s especially dangerous in bull markets, when feeds get flooded with bullish charts and portfolio screenshots. Then things flip and the market or drops significantly. The same crowd that made you feel safe disappears right when you need independent thinking most.

A quote I often come back to is Buffett’s reminder to “be fearful when others are greedy and greedy when others are fearful.” It’s important to remember that crowd emotion is not grounded analysis.

How to prevent it

When you feel urgency to act (usually out of emotion), pause. A rule of thumb I personally use is to wait at least two days after a significant event before I act.

It helps me step back and put things into perspective. It also helps to start with a smaller position and add as the business proves itself. Track business metrics, not what your social media feed is telling you, which can be extremely narrative driven instead of being grounded in facts. If the business is fine, it’s much easier to stay on track even when the crowd is saying otherwise.

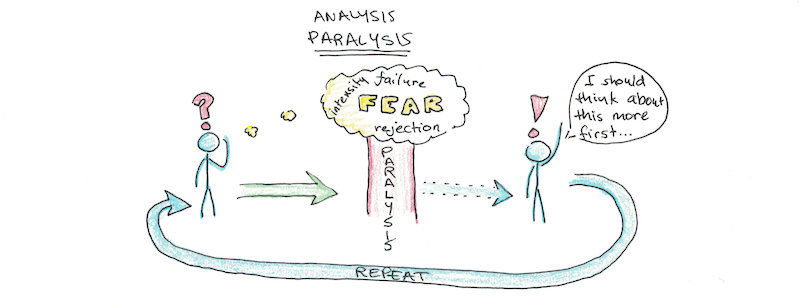

3. Information bias

Information bias is when you believe more information automatically leads to better decisions. In reality, it often leads to more certainty without more accuracy.

You read everything, watch every clip and stay on top of everything. But then someone asks what would make you wrong and you might not have a clear answer. You have a lot of information, but you haven’t made it actionable.

How to prevent it

Limit inputs to the ones that really matter to you. Inputs I personally use are company fillings, quarterly reports and earnings calls for example. It helps to convert that into a thesis, key metrics, risks, valuation ranges, and what might change my mind.

4. Incentive caused bias

Incentive caused bias is when you underestimate how much incentives shape behavior, including your own. Like following advice without understanding the business model behind it. Or listening to management without separating what they’re saying from why they’re saying it.

A lot of market content isn’t designed to help you. It’s designed to get attention, build a brand, or sell a product. That doesn’t make it useless, but it does mean you should ask one question before you let it shape your portfolio. What is the incentive?

You can ask that question about my Investing Visuals content as well. I started my brand because I genuinely love creating visuals and helping other investors in the process. But I can only do this full time if there are ways to monetize it too.

That’s the incentive I have as a creator: to find ways where readers, like yourself, are willing to pay for valuable content, which in turn allows me to put more time and effort into something I love doing and create more valuable content.

How to prevent it

For every opinion you come across, ask: does this person get paid for it? If not, what other incentive could they have? I personally prefer people who are open and transparent about their decision making over time, and who own their mistakes when they make them.

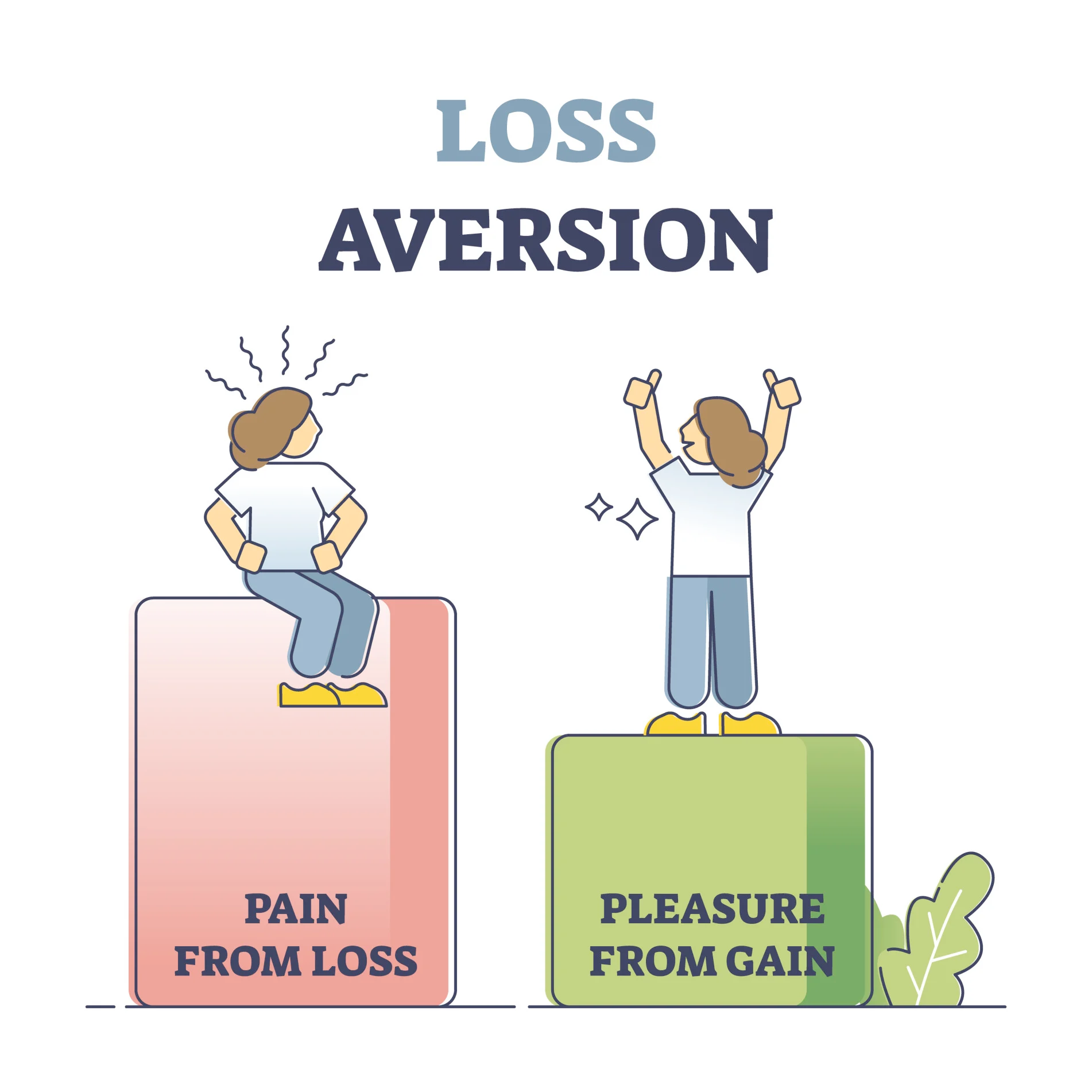

5. Loss aversion

We feel the pain of losing money more strongly than the joy of making the same amount. That’s why a small loss can feel like a disaster, even when it’s normal volatility.

It’s a psychological phenomenon that’s most dangerous in bear markets. It can trigger you to sell at a steep loss to avoid the pain, only to see the stock run hard when the market flips (and sometimes you end up buying it back higher).

How to prevent it

Decide in advance what would make you sell or add, and write it down while you’re calm. Zoom out to probabilities and position sizing so a single move doesn’t hijack your decision making.

That’s why I always include "thesis breakers" in the deep dives I create. It helps me prepare for situations where I need to act. It also helps separate price action from fundamentals. A stock down 30% can be fine. A deteriorating business is not.

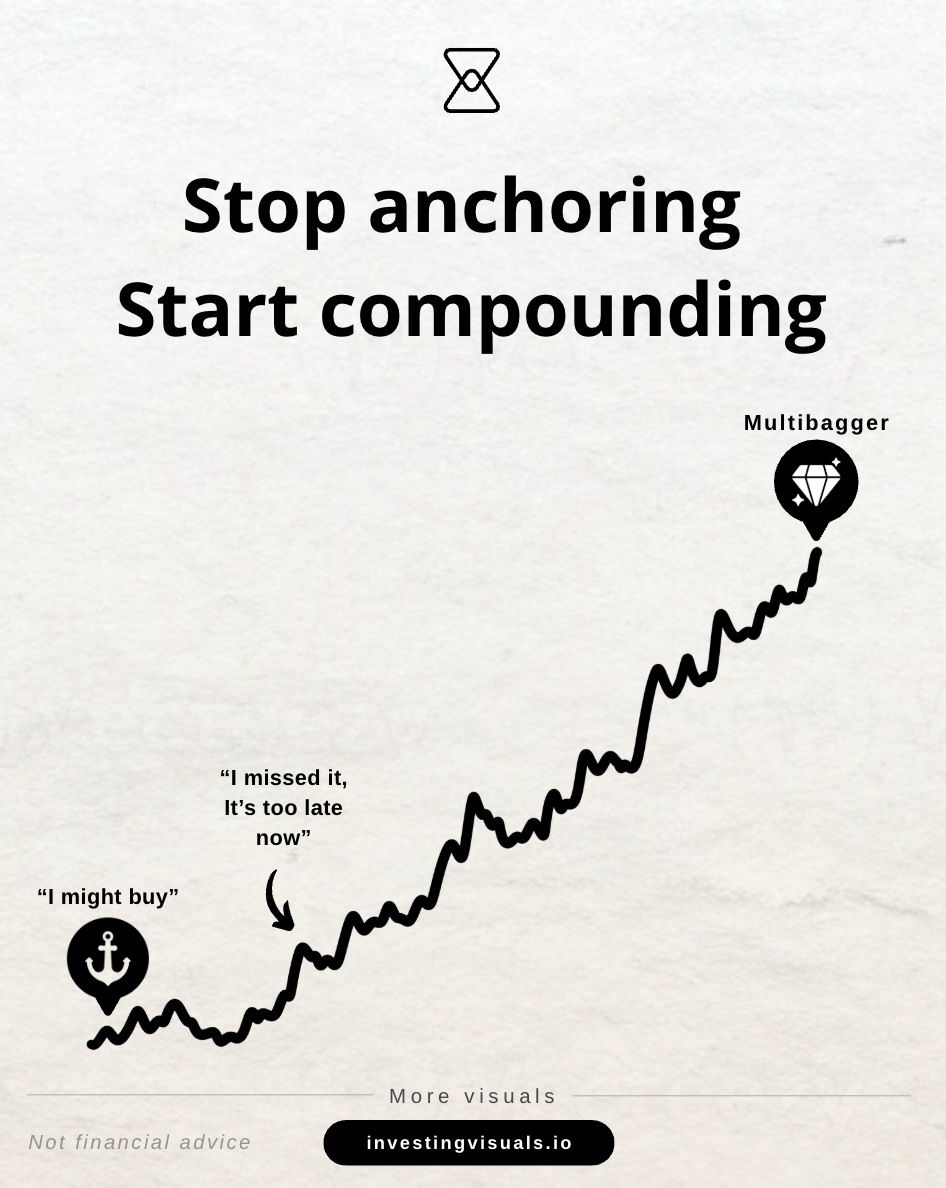

6. Anchoring bias

We get stuck on one number, usually our buy price or a recent high. It makes us think a stock is “cheap” just because it’s down from that anchor.

I’ve done it in the past, and it’s still something that’s easy to fall for. It can make us decide not to invest because “it will get back to prior lows,” when in reality it might never get there again as the business keeps executing.

The other way around happens too, especially for positions that have sold off: “it will reach my entry price again so I can recoup my losses.” But it might never get there.

How to prevent it

Replace the anchor with a question: what is the business worth today based on realistic forward assumptions? Use ranges, not a single price, and update your view when the facts change. I do this all the time, which you'll also see in my portfolio updates.

I buy and verify. Is my thesis still on track based on quarterly earnings and the news that matters for the long term?

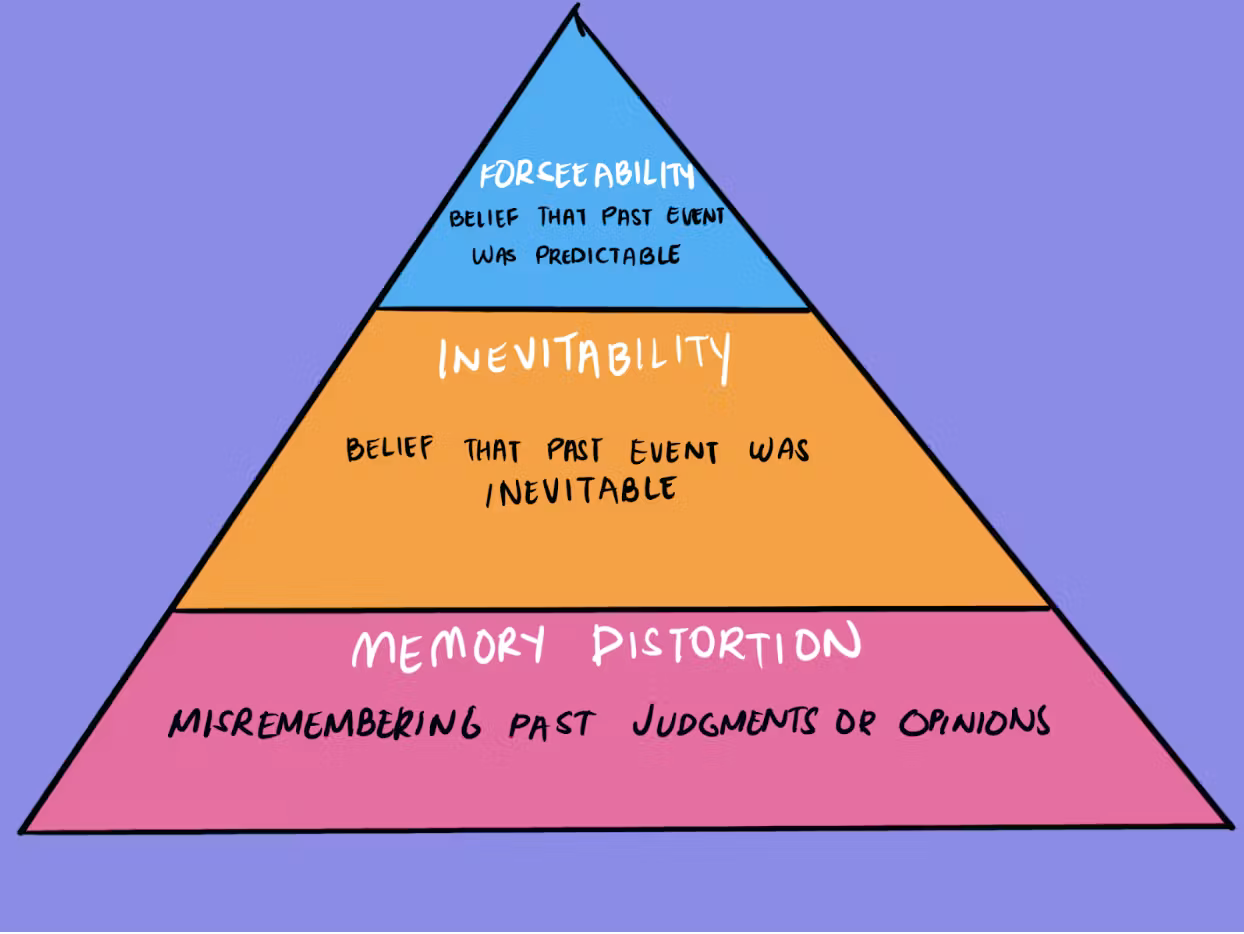

7. Hindsight bias

After something happens, it suddenly feels obvious. We rewrite the story in our head and forget how uncertain it really was in the moment. It has three layers, from top to bottom:

- Foreseeability: The ending now looks obvious, so we tell ourselves we saw it coming. But most of that clarity is hindsight, not skill. Typical quote: “I called this months ago.”

- Inevitability: Once the outcome is known, it suddenly feels like it had to happen. We forget that, in real time, there were multiple paths and the future was still wide open. Typical quote: “Yeah, this was always the most likely outcome.”

- Memory distortion: After something happens, our brain cleans up the past. We start “remembering” that we felt way more certain than we actually did. Typical quote: “Honestly, I was thinking this all along.”

How to prevent it

Capture your thinking before the outcome is known. Write down what you believe, why you believe it, and what would prove you wrong. Include 2 to 3 other realistic scenarios and rough probabilities, so you don’t treat one path as “the obvious one” later.

Then review your notes after the fact and grade the process, not the result. If you do this consistently, it becomes much harder for your brain to rewrite history and tell you that you knew it all along.

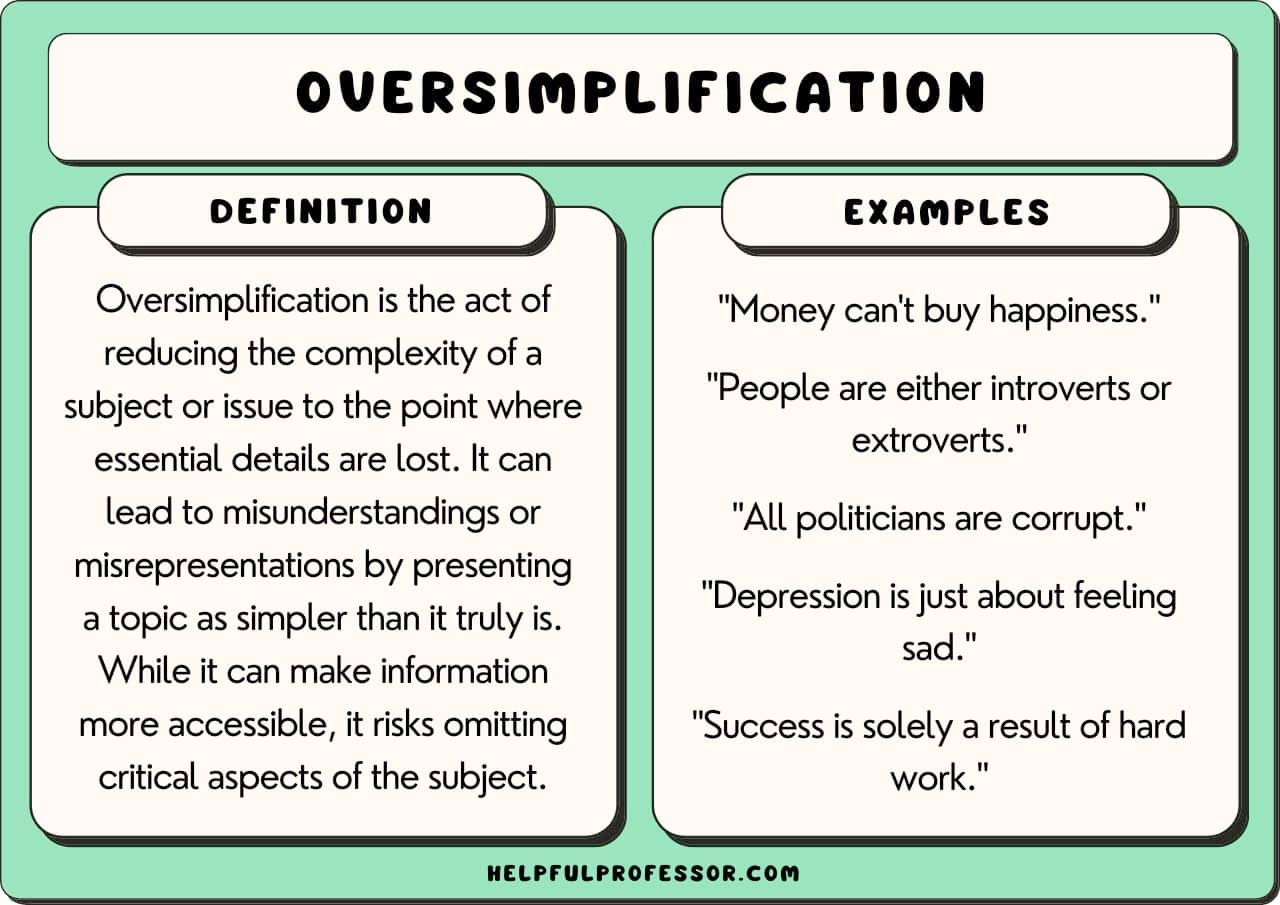

8. Oversimplification

We take something messy and complex and compress it into one clean explanation. It feels satisfying because it creates certainty, but it usually ignores the real drivers that move outcomes.

In investing, it shows up as one metric, one headline, or one narrative becoming the reason a stock will win or lose. The danger is that you stop looking once you’ve found a story that sounds right.

How to prevent it

I force myself to list 3 to 5 drivers, then rank them by what matters most over the next 6 to 24 months. In my deep dives, this shows up in the metrics to watch and the bear case section. And I keep one clear check: what new data would make my story wrong, and how quickly would I notice it?

9. Restraint bias

This is when we think we’ll have more self control later than we actually do. In calm moments, we believe we’ll stay rational, stick to the plan, and not get pulled around by emotions. But when a stressful situation arrives, we start to make small exceptions that add up fast over time.

How to prevent it

Put guardrails in place before you need them, with simple rules that remove decision making in the heat of the moment. Create friction for impulsive choices, like a mandatory pause before acting or fewer check ins on whatever triggers you. One of my guardrails is to always wait two days before I act on thesis moving news, to avoid emotional decisions.

Closing remarks

I hope this article helps you arm yourself against yourself. It’s not a matter of if these psychological challenges will show up, but when they will show up. Being aware of them is the first step in facing them head on and become a better investor over time.

To summarize

- Confirmation bias: Once I buy, it’s very easy to start protecting my thesis instead of testing it. That's why I always write down a bear case and clear thesis breakers before I hit the buy button.

- Bandwagon effect: I always try to minimize my dependency on crowd opinions. Which is only possible if I truly know what I own.

- Information bias: More inputs can make me feel like I’m in control, but not necessarily make me right. I limit what I consume, stay selective with sources, and convert it into something actionable: thesis, key metrics, risks, and what would change my mind.

- Incentive caused bias: Most market content is not designed to help me invest better. It’s designed to get attention or sell something. I try to ask one question before I let it influence me: What is the incentive behind this message.

- Loss aversion: volatility is part of the type of portfolio I have. My sell decisions are always tied to business performance and opportunity costs and if I have to sell at a loss, I will.

- Anchoring bias: My entry price and the old highs don’t matter, but my brain has the tendency to still do so. I try to replace that anchor with a question: "What is this business worth today based on realistic forward assumptions?"

- Hindsight bias: After the outcome, things can feel obvious and we might start telling ourselves we “knew it all along.” That’s why I try to capture my thinking before the result is known, including what would make me wrong and a few other realistic scenarios.

- Oversimplification: It’s tempting to turn a complex situation into a clean one liner, but that’s usually where important context gets lost. I force myself to list 3 to 5 drivers, write a bear case and include important details.

- Restraint bias: To prevent impulsive behavior, I put guardrails in place ahead of time, add friction and keep one simple check: If I can’t explain what changed in one clear sentence, I shouldn’t be changing the plan.

Thanks for reading!

~ Jan

As always, none of this is financial advice. Always do your own due diligence before making an investment decision that fits your own risk tolerance and time horizon.

Written by

Sign-up

And receive the latest visuals and articles straight to your inbox

Member discussion