Axon earnings recap Q4 2025

Axon delivered an amazing Q4 2025. Let's unpack everything from financials to key business highlights and what the road ahead looks like.

I'd like to start off with a great quote from Rick Smith, Founder and CEO of Axon:

A decade ago, when our SaaS business was gaining momentum, there was real pressure to shed hardware and chase software margins. I disagreed. My conviction was, and remains, that the most important customer problems require integrated solutions, not point products.

This is exactly what makes Axon such a strong business: the sum of parts. Hardware and software. That one quote connects almost everything in the press release, the shareholder letter, the investor deck, and the Q&A.

Axon is very much focused on becoming the operating system for rapid response. Sensors, evidence, workflows, real time operations, and now AI that is directly integrated into those workflows.

With that being said, let's run through the key numbers of Q4 2025.

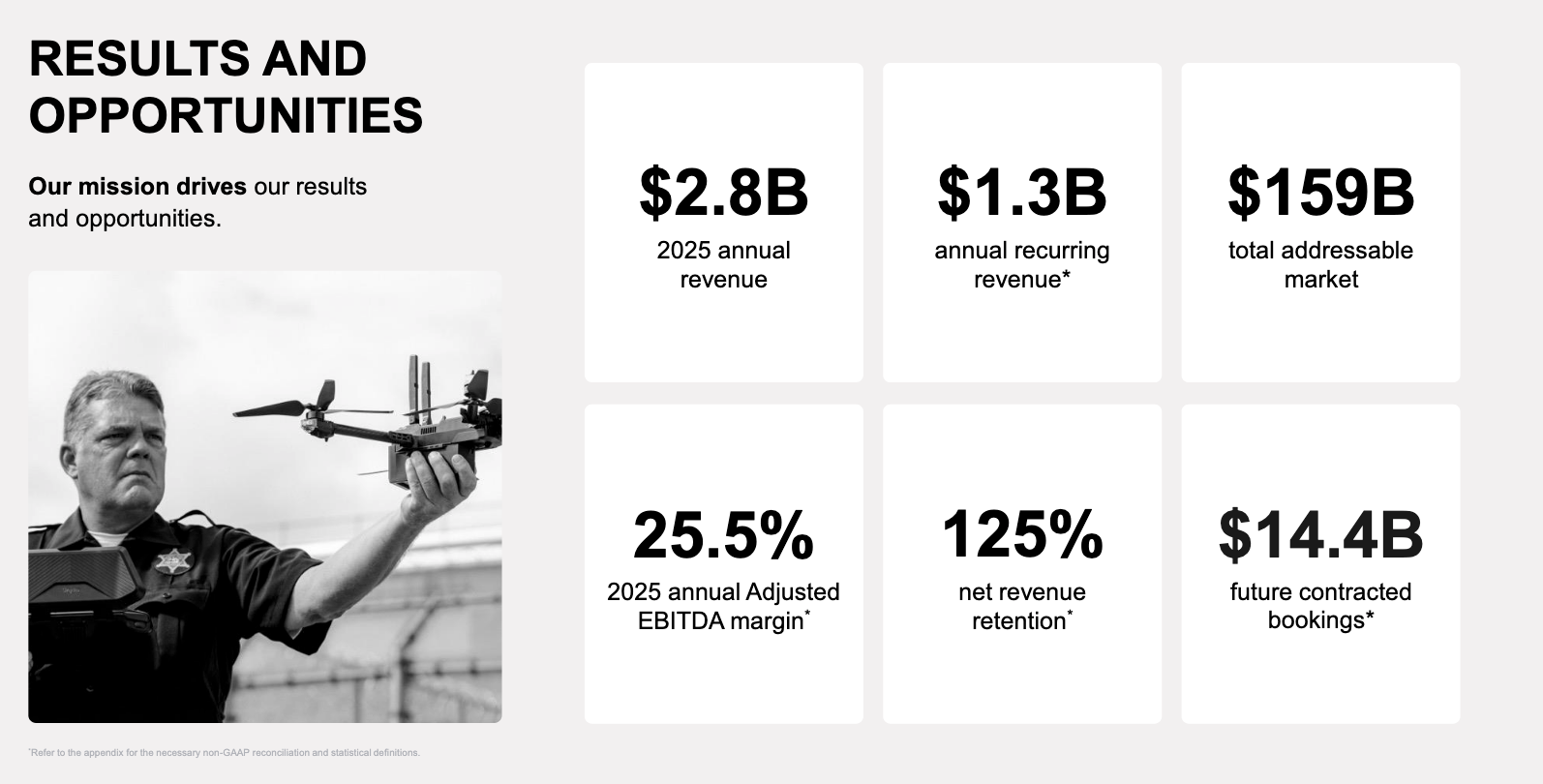

1 - Key numbers

- Q4 revenue grew 39% to $797M, with Software and Services up 40% and Connected Devices up 38%

- ARR reached $1.347B, up 35% YoY, and net revenue retention accelerated to 125% (top notch)

- Management highlighted full year bookings surpassing $7B, up more than 40% from last year

- Future contracted bookings climbed to $14.4B, up 43% YoY, and the company expects to fulfill 20% to 25% over the next 12 months and the rest over roughly the following decade.

2 - Guidance

From their shareholder letter: “Our momentum is accelerating as we enter 2026, supported by disciplined investment, strong product market fit and deep, trusted relationships with our customers.”

Fiscal year 2026

- Revenue growth: 27% to 30% (very likely to be significantly higher)

- Adjusted EBITDA margin: 25.5%

- Stock based comp expense: $590M to $620M

2028 outlook

- $6B in annual revenue ($2.5B today) with 28% adjusted EBITDA margin

- Limit annual dilution from stock based comp to less than 2.5%

Especially this last point is something I love to see. Dilution has been one of my main issues with Axon so far, and it's good to see that they are addressing this. 2.5% still is significant, but manageable.

3 - Business highlights

The shareholder letter lays out the roadmap ahead for Axon. “Introduced major product expansions, including Axon Vehicle Intelligence, Axon Assistant, Axon Body Mini and Axon 911.”

This post is only for subscribers on the

Premium and Supporter tiers

Subscribe to continue reading

Written by