Premium and Supporter tiers

Astera Labs Deep Dive - The neural network of AI

Without data centers there's no AI. But there are no data centers without businesses like Astera Labs. This deep dive will help you understand why Astera is such a crucial infrastructure player and if it could be an interesting investment.

Introduction

Astera Labs is one of the clearest ways I know to invest in the physical limits of AI data centers. Most of the narrative still lives with the GPU giants like Nvidia. Yet the systems that decide how fast data actually moves between those chips are just as important. That is exactly the layer where Astera operates.

In simple terms, Astera designs connectivity chips that sit between GPUs, CPUs and memory in cloud and AI data centers. They do not train models, they do not run apps. They build the 'plumbing' and traffic control that lets all of that compute run as efficiently as possible.

In this deep dive I will unpack why I believe Astera is such an interesting company that's worth your attention. I will use analogies, visuals and real world examples so that even if you have no technical background, you can still understand what Astera does, why it matters and how I think about the trade off between quality and price.

With that, let's dive in.

1 - Highlights

If you only remember a few things about Astera Labs, I would pick these:

- Data centers do not function without the technology that Astera provides. Their connectivity 1 chips are essential for the scale-up and scale-out of modern data centers

- They are founder-led, with an engineer-heavy culture, fully focused on cloud and AI infrastructure

- Astera scaled revenue from $79 million in 2022 to $723 million in 2025 with a very healthy balance sheet, positive free cash flow and >30% free cash flow margins.

But: you have to be willing to pay up for this business and be comfortable with quite some volatility. I'd categorize this as a high-risk/high-reward play.

💡

1 Connectivity chips make sure data can travel cleanly and quickly between processors like GPUs, CPUs and memory and storage.

2 - Astera's mission

Astera is a highly specialized, 'fabless' 2 designer with one job: remove data, network and memory bottlenecks in hyperscale cloud and AI environments. You can think of Astera as the provider of the communication lines between the chips powering AI. They are not a 'nice to have'; data centers would not function without them.

Management describes their mission as:

“Innovating and delivering semiconductor-based connectivity solutions that unleash the full potential of cloud and AI infrastructure.”

There are a few important questions to answer though:

- How durable is the problem they solve?

- How defensible is their position?

- How concentrated is their revenue?

- How much of their growth and quality is already priced in?

- Is Astera, all things considered, worth investing in?

This deep dive will cover all these topics and more, but let’s start with their founding story.

💡

2 Fabless means that they design the chips, but do not own the factories that make them. TSMC is the one manufacturing the chips.

3 - Founding story and contrarian thesis

Astera Labs was founded in 2017 by three former Texas Instruments engineers. The CEO, Jitendra Mohan, and his co-founders spent years designing extremely fast chips that can communicate clearly in a very “noisy” environment, to put it in simple terms.

The contrarian bet was that connectivity itself would become a first-class design problem in the cloud era. Instead of treating it as a side effect of CPUs and GPUs, there was room for a standalone company that focused entirely on the communication layer that sits between processing units.

That focus shows up everywhere in their portfolio today. They do not build GPUs. They do not build CPUs. They build products that sit between them and make the whole system work at massive scale.

Astera's timeline

2017

Astera Labs is founded in Santa Clara. From day one the idea is simple. Do not build the big chips. Fix the traffic between them. Modern data centers are drowning in data, so Astera chooses to focus purely on how that data moves.

2018 to 2022

In the next few years, the team ships its first connectivity chips and wins early data center customers. They pick TSMC as their main manufacturing partner and add products that move data reliably over very fast network links inside the data center racks and across the data center. In 2022, Astera raises a large funding round at a multi-billion valuation and leans into “CXL”, a new way to share memory between servers.

2023

They open a large interoperability lab to test Astera chips with hardware from all the major compute and memory vendors (think AMD, NVIDIA, Intel etc.). Revenue passes $100 million and the company starts to look like a real AI infrastructure player, not just a niche startup.

2024

Astera goes public on Nasdaq under the ticker ALAB, launches new generations of its connectivity chips and introduces Scorpio, a “traffic controller” chip for AI servers. It also expands its research and lab footprint closer to key customers.

Today

All four product lines now contribute to revenue, with Aries being the core engine and Leo and Scorpio ramping. Growth is strong, and Astera is becoming a scaled public business. Its memory connectivity chips begin to show up in public cloud offerings, putting the company inside the next generation of AI data centers.

Now that we know the founding story, it's time to take a closer look at the problem they actually solve and the products they've launched to address these.

4 - The problem they solve and why it matters

4.1 - The problem

Modern AI data centers face three related bottlenecks: data, network and memory. The simple analogy here is a busy airport. In this analogy:

- GPUs are the planes

- Data and memory are the passengers and luggage

- Connectivity chips are the runways, gates and taxiways

You can buy more planes. But if the runways are short, the taxiways are congested and the gates cannot handle the flow, the overall system still underperforms.

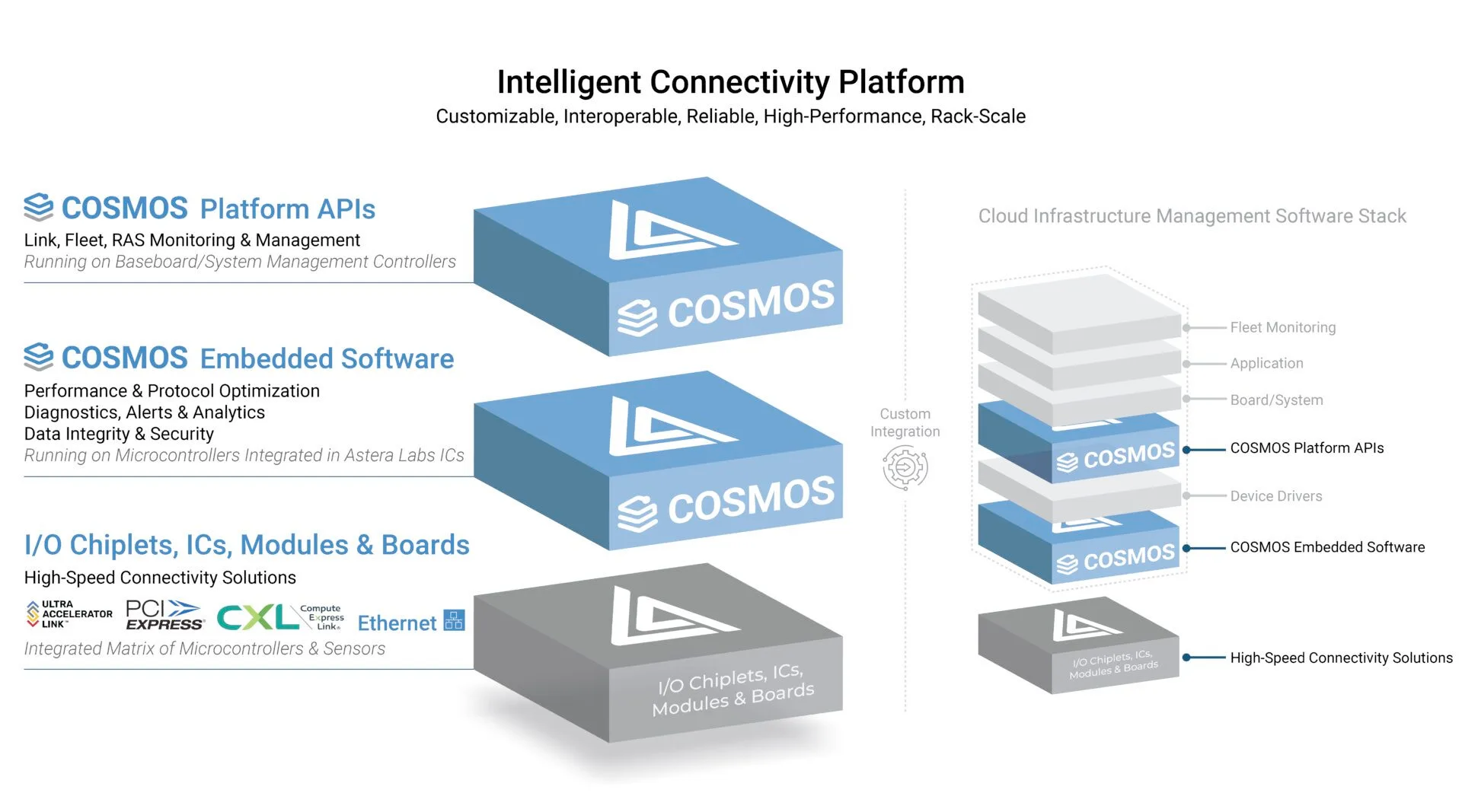

Astera positions its “Intelligent Connectivity Platform” precisely at these pain points. The platform combines high speed connectivity products with an embedded software suite (COSMOS) that configures, monitors and optimizes those links in real time.

Astera is focused on designing, building and running the entire airport ground infrastructure and control system, connecting all these different parts to make sure they operate as effectively as possible.

4.2 - Why it matters

Imagine you’re a CEO and you’ve decided to spend billions on creating an AI cluster, but you only get 70% of the theoretical performance because of bottlenecks. This dramatically increases the cost per unit of compute, directly eating into your margins.

With their product line-up, Astera sells a way to maximize the returns on these AI expenditures. That is a very strategic value proposition in this current AI cycle which is characterized by its massive investments.

Another important topic is vendor lock-in. If you can deploy vendor-neutral connectivity that works across GPUs, CPUs and accelerators from different suppliers, you reduce lock-in and increase negotiating power. Which in a world where NVIDIA has sky-high margins, is definitely worth consideration.

With that being said, let us take a closer look at what their product line-up is exactly.

4.3 - A closer look at their products

Normally I would rank the product line-up based on the revenue split per line. Since Astera does not disclose revenue by product line, the ranking below reflects my best judgment based on filings and management commentary.

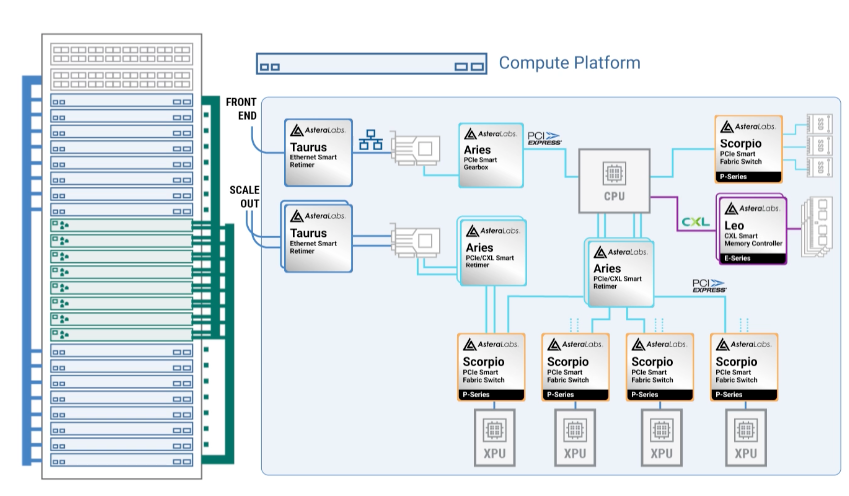

1 - Aries

It’s the core engine in Astera’s product line. This family of chips is tasked with solving an important problem: when processors communicate with speeds pushed higher and distances longer, the signal starts to fall apart. It’s like running a high-speed train on an old track that was never designed for it.

Aries ensures smooth and noise-free traffic. It ensures that GPUs, CPUs and storage can talk at extreme speeds without constant errors so that the AI stack running on these clusters performs as efficiently as possible.

2 - Taurus

Think of Taurus as the smart cables between servers and other modules. The problem that Taurus solves: as you push more traffic through these cables, the signal can get fragile. Taurus is the smart module inside cables that boosts or cleans signals if needed and monitors how healthy a signal is in real time.

Back to the analogy: Taurus is like smart shuttle buses on a large airport that constantly adjust routes and speed to avoid traffic jams and keep a live dashboard for the operations center.

3 - Leo

Leo is all about storage. Today, each server has its own fixed memory, like each gate having its own tiny baggage room which works up to a point. But with AI training and large models there’s a need for more and more memory, and they want to use it flexibly. Leo is basically building large shared storage wings that they can tap into when needed.

It’s still in its early stages and revenue is ramping, but it’s addressing an important memory bottleneck.

4 - Scorpio

At a high level, Scorpio is Astera’s fabric switch for AI servers. A fabric switch is the traffic controller for all the connections inside a server or rack. It’s connecting GPUs as efficiently as possible and making sure there are no bottlenecks.

5 - COSMOS

The software layer that functions as a control room, providing oversight of everything going on. It uses the data from Aries, Taurus, Leo and Scorpio, to track whether their signals are clear, throughput is high and to drill down into problematic connections if needed.

It transforms all the independent chips and wires into something that can operate like a system. It likely does not move the revenue needle on its own but adds great value through the visibility it provides to operators, making the overall product suite more stickier as a whole.

In short

Aries and Taurus are about keeping individual links clean, Leo is about shared memory, and Scorpio plus COSMOS are about orchestrating everything as one system.

On their website, Astera has a neat visual representation of how all these parts work together, which is worth a look as well.

Now that we have an idea of what Astera does and what they provide, it’s interesting to look at how they position themselves against competitors. A topic that is especially relevant for Astera.

5 - Industry positioning and ecosystem map

5.1 - Where Astera sits in the stack

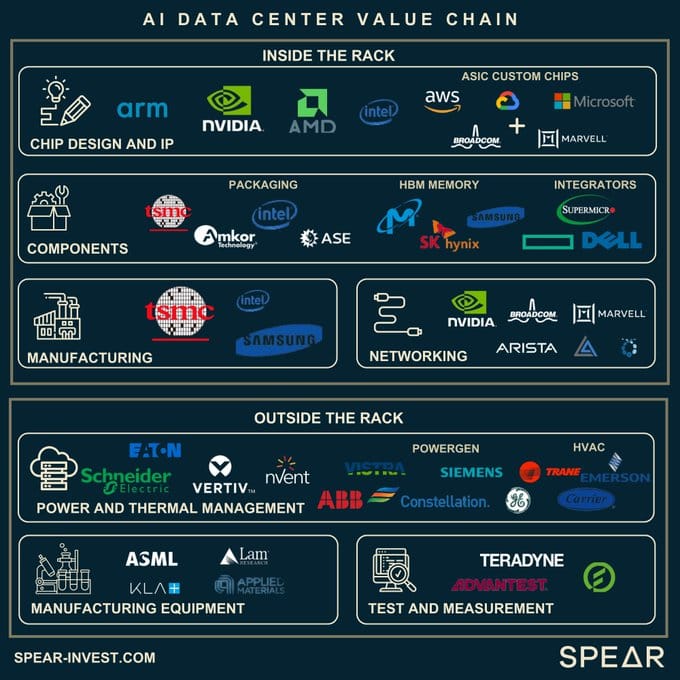

If you look at the visual below, there’s a distinction between those inside and outside the rack 3.

Inside the rack you find companies like NVIDIA, AMD and Intel for the compute. Micron and SK Hynix for memory. And NVIDIA, Broadcom and Credo in networking.

Outside the rack you have companies like ASML and TSMC that build the tools and manufacture the chips.

Astera sits snugly inside the rack that connects all this together. They are the connectivity glue so that GPUs, CPUs, memory and networks from all those logos can actually run at full throttle together.

💡

3 When referring to ‘rack’, it simply means a tall metal cabinet that holds all the data center gear. You can picture it like a bookshelf for computers. With a data center being a library, filled with hundreds if not thousands of these bookshelves.

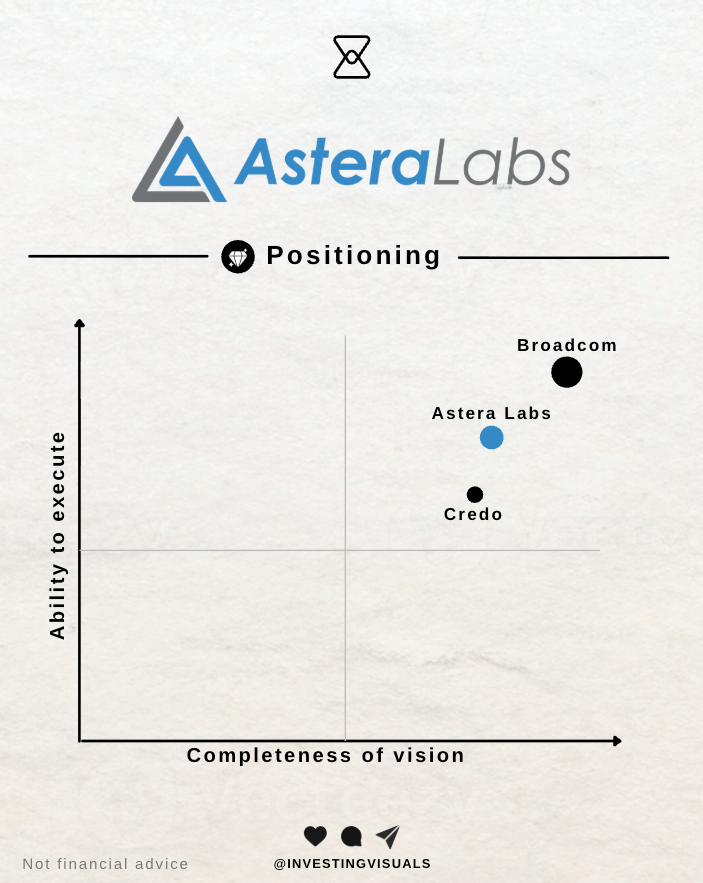

5.2 - Core competitors and relative positioning

A great way to assess competitors is Gartner's Magic Quadrant. Because Astera doesn’t show up in any of the quadrants due to their relatively small scale, my rough placement would be as follows:

I’d place Broadcom in the top right corner as the incumbent with massive scale and proven execution. Credo builds chips and smart cables that keep data signals clean as they travel between servers and between racks. Astera does that too, but combines it with memory connectivity and a control layer on top through products like Scorpio and COSMOS.

When comparing Astera and Credo to Broadcom, it is good to note that they are playing different games.

Astera and Credo are the specialists, basically the nervous system inside the AI rack, very close to the GPUs. Astera is the one with a more complete product portfolio compared to Credo. Broadcom on the other hand is the widely diversified connectivity giant.

In this large and expanding market, I believe there is room for all three players to do well, but more on that in section 9 - Total addressable market. Before we go there, it's important to first discuss a vital part of Astera's value proposition: their partner network.

5.3 - Partnership network

A strong partner network isn’t just a nice to have when you’re creating products that must be interoperable 4 between multiple vendors.

💡

4 Interoperability in this context means that data can flow between different systems with minimal effort.

According to their 10-Q, Astera has “trusted relationships with the leading hyperscalers” such as Microsoft, Amazon, Google and NVIDIA. Astera has very tight integrations with both CPU and GPU vendors and their Scorpio “Operator software suite” is, for example, plugged into NVIDIA’s NVLink.

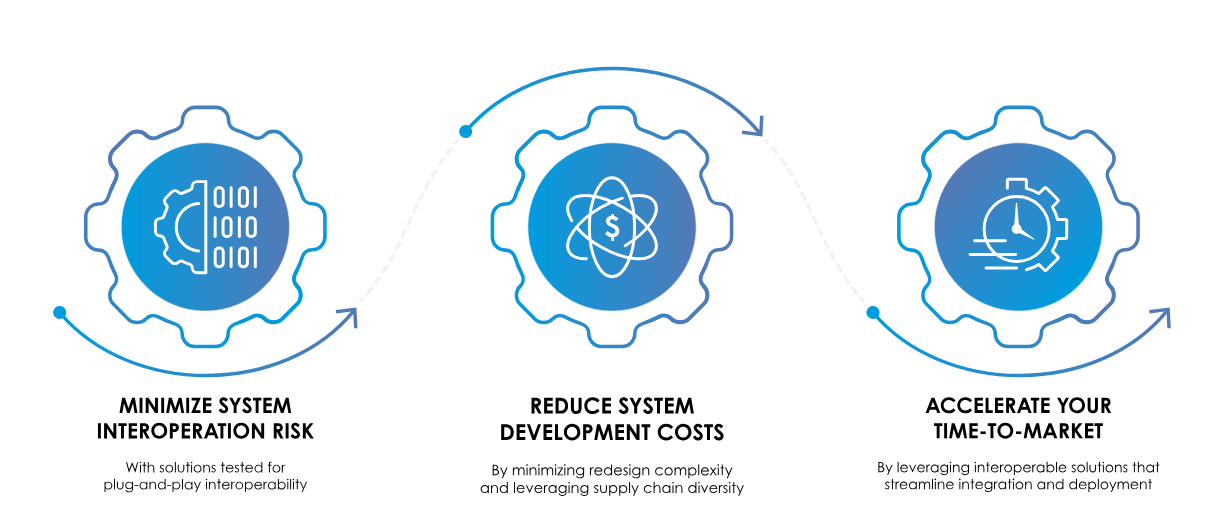

If you want to be the player that ties it all together, you’ve got to make sure your products are compatible with all these vendors. This is where their “Interop Lab” comes in, short for “Interoperability” (how creative!).

With the ever-growing complexities in AI, their Interop Lab ensures seamless integration and scalability across different vendors. Astera highlights the three key benefits below, which I will touch upon again when discussing their competitive advantages.

6 - Moat: how they stay ahead

Because Astera operates in a competitive environment versus major players like Broadcom, it's important to assess how they can stay ahead. I'd like to do so by using the Morningstar economic moat framework.

When looking at the main sources of a moat, I would rank them as follows, from strongest to weakest:

6.1 - Switching costs (high)

This is the most important one for Astera so I'll cover it in some more detail. Once a connectivity solution is designed into an AI platform or server architecture, switching vendors is painful. Let's get back to the airport analogy here:

Once you design a connectivity stack like Astera into an AI platform, it is a bit like choosing the entire ground system for a major airport.

It's like standardizing:

- The way planes dock at the gates

- How luggage moves through tunnels and conveyor belts

If you later decide to switch vendors, you are not swapping a single component. You are basically:

- Retesting every taxi route, gate connection and baggage tunnel to make sure nothing breaks at peak traffic

- Potentially rebuilding parts of the terminal layout, moving belts, doors and loading zones to fit the new equipment

And you have to rebuild it while the airport is still open because any downtime is extremely costly. That is what switching costs look like here. Once an AI “airport” is built around a specific connectivity solution, changing it will be very expensive and time consuming. For hyperscalers running mission critical AI workloads, the risk of swapping out a proven connectivity solution is substantial.

That does not mean they cannot qualify multiple vendors. But Astera’s “first in and deeply integrated” position in several GPU platforms gives them strong embedded switching costs.

6.2 - Efficient scale (medium-high)

The market for high-end AI connectivity silicon is large in dollar terms but limited in the number of customers. There are only so many hyperscalers and system OEMs 5 at the very high end. That naturally limits the number of vendors that can achieve meaningful scale.

Astera, Broadcom and a few others can share the market, but there is not enough room for dozens of profitable players at this level of specialization. That creates an “efficient scale” dynamic where players with strong relationships and IP are protected from excessive fragmentation.

Once you have reached meaningful scale with a handful of very large customers, this structure supports high returns on invested capital.

💡

5 OEM stands for "Original Equipment Manufacturer". They are the companies that build the full servers and boxes that end up in data centers such as Dell, Supermicro, HP etc.

6.3 - Intangible assets and brand (medium)

Astera has built a brand as an innovation leader in PCIe 6, Ethernet and CXL 7 connectivity. They have a portfolio of patents and have demonstrated first-to-market products multiple times, including the Aries smart retimers.

In the long run, that matters because it builds a track record of dependable execution across several design cycles, leading to trust.

💡

6 PCIe is short for Peripheral Component Interconnect Express. It is the main high speed connection inside a server that links GPUs, CPUs, storage and other components so data can move quickly between them.

💡

7 CXL is short for Compute Express Link and is a newer standard that runs on top of PCIe and lets servers share and use memory more flexibly.

6.4 - Cost advantage (medium-low)

As a fabless company, Astera does not control fabs. However, it can benefit from:

- Process node choices optimized for mixed signal performance and cost

- Learning curve effects as volumes ramp in the same product family

I would not call this a structural cost moat yet. It is more an operational skill that can support margins.

6.5 - Network effects (low)

There are weak network effects via ecosystem participation in their Cloud Scale Interop Lab and support for multiple hosts and endpoints. But this is not a classic network effect business in the software platform sense so I do not assign much moat strength here.

7 - Employee view and culture

I find culture an underappreciated and often overlooked part of investing. Ultimately, it’s the people who make the business. When looking at Glassdoor, reviews are consistently strong, which I love to see. As of the time of writing, Astera has:

- An overall rating around 4.6 out of 5

- High scores on culture and values, career opportunities and compensation

- Around 9/10 employees who would recommend the company to a friend

- 93% approval rate of the CEO and co-founder Jitendra Mohan, which is a top-notch score

Themes in the written reviews:

- Smart, driven colleagues

- High expectations and workload due to hypergrowth

- Fast moving environment with lots of learning

There are some reviews that mention workload and stress, which is typical in hyper growth startups. I do not see those as structural red flags at this stage, but it is something to keep an eye on as Astera scales.

All in all, the reviews fit into the picture of a focused, engineering-heavy culture that is still in the earlier scaling phase with high quality management steering the ship in the right direction.

But who exactly is the leadership team? Let's take a closer look.

8 - Leadership & ownership

Astera is a founder-led story that never really left engineering mode. At the center of the business is Jitendra Mohan, co-founder and CEO. He is the one carrying the vision and long term view on what connectivity needs to look like for AI scale data centers.

Around him sit his two fellow co-founders. Sanjay Gajendra, President and COO, who runs the commercial and operational engine. Casey Morrison, Chief Product Officer, is the one behind the portfolio, responsible for turning all those bottlenecks into solutions the big cloud players can deploy at scale.

The rest of the leadership team is built to support the founder's core:

- Mike Tate as CFO is a veteran finance leader across semis and infrastructure and brings the discipline needed for a company that grew up fast and then stepped into public markets

- Thad Omura as Chief Business Officer has more than 25 years experience in marketing and business leadership across startups and large chip companies

- Philip Mazzara as General Counsel and Secretary handles the complexity that comes with global customers, IP and public reporting.

On the board, independent chair Manuel Alba adds deep semiconductor and connectivity experience, and the recent addition of Craig Barratt brings another seasoned operator who has scaled networking and chip companies before.

In short

Astera has a seasoned leadership team, built around three founders that sit at the heart of the business. A mix that I love to see because it combines founder depth and vision with seasoned operators in finance, legal and go-to-market strategies.

Ownership

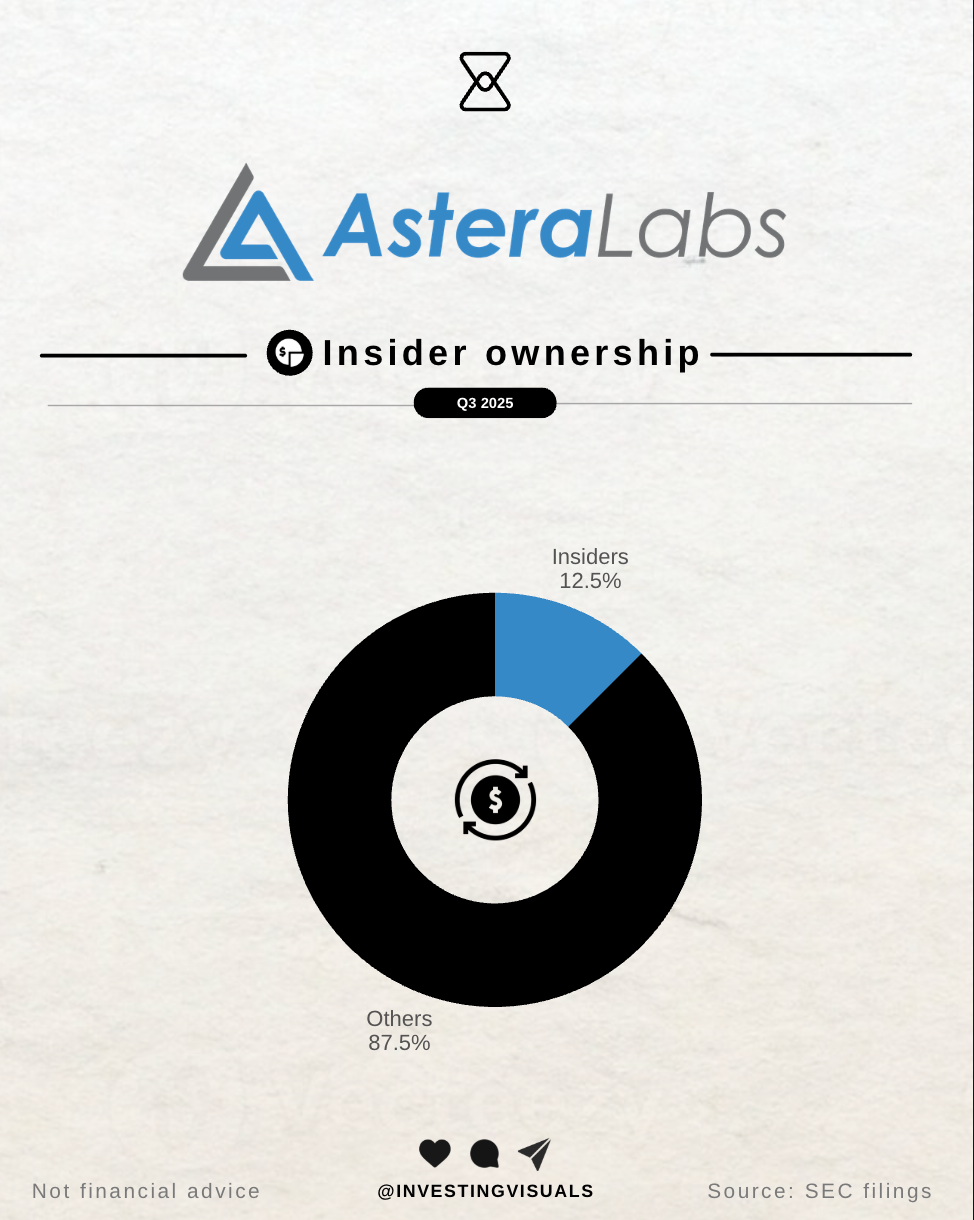

Unlike many modern tech IPOs, Astera chose a single-class common stock structure. Every share carries one vote. There are no "super-voting founder shares" giving the founder extra voting power. Meaning Astera is a founder-led, but not founder-controlled business. Insiders own ~12.5% of all outstanding shares with Jitendra and Sanjay each holding mid single-digit stakes.

9 - Total addressable market and optionality

Earlier, I touched upon the large market Astera is operating in. Their S-1 filings and subsequent communications provide two useful TAM reference points:

- Around 17.2 billion dollar TAM in their IPO materials for the wired connectivity and CXL memory connectivity markets they targeted at the time (2024)

- Around 27.4 billion dollar projected TAM by 2027 as they expand their coverage across PCIe, Ethernet and CXL based solutions

If Astera reaches $1 billion annual revenue by 2027, that's a 3.6% market share, leaving a lot of room to grow alongside other players in the space. I treat these company-provided numbers with the usual caution, but the direction is more important than the exact figure.

Beyond the current product family, I see three main adjacencies:

- Deeper memory connectivity

- Building more features into Scorpio style switches, for example telemetry, congestion management and integration with open fabrics

- Optics to supporting the massive bandwidth needs of scale-up systems with hundreds of AI accelerators.

Especially this last one is interesting because it directly links to an important recent acquisition Astera has done.

10 - An important recent acquisition

On October 22 2025, Astera announced they will acquire aiXscale Photonics, a German company that makes very precise optical coupling technology: essentially the “glass bridges” that move light cleanly between photonic chips and fiber.

From Astera's statement:

"As the AI industry prepares for the next wave of infrastructure requirements, optical connectivity is critical to supporting the massive bandwidth needs of scale-up systems with hundreds of AI accelerators."

COO Sanjay Gajendra:

"This acquisition will bring critical talent and advanced photonic technology that, when combined with our fabric switch and signal conditioning expertise, will unleash the full potential of rack-scale AI deployments."

I think this is a smart move by Astera because aiXscale brings them deeper into optical connectivity, which increases their value proposition beyond copper cables.

The airport analogy

To help you fully understand why this matters, let's use the airport analogy again to explain why optics are so important: today, most of Astera’s world is still electrical. Think of copper links as busy ground roads around the airport. Aries, Taurus and Scorpio are the traffic systems that keep those roads flowing.

As traffic explodes, you eventually cannot just add more buses and trucks. You need fast, lightweight connections between terminals that do not get stuck in ground congestion. That is optics. A new way of transport as requirements become increasingly demanding as AI infrastructure evolves. With this acquisition, Astera is prepared for a world where light-based links take over once copper reaches its limits.

Astera has not disclosed the purchase price or deal size in any SEC filing or press release I can find. So as of now, there is no reliable public number for the total deal value, which usually means it's a relatively small deal.

11 - Deep dive into the numbers

Having covered the core parts of the story, it’s time to shift from understanding Astera to making a decision.

In the next sections, I’ll break down the financials in more detail, map the risks that matter most, lay out my bull and bear case, and put the current valuation into perspective using a number of scenarios. I’ll close with my personal verdict and what I’ll be doing from here.

As to Astera's financials: these are are nothing short of spectacular, with the headline figures being:

- Revenue: $723 million (last twelve months), up +136% y/y

- Free cash flow: $229 million, up 150% y/y

- Net income: $198 million

- Gross margins: 75%

- Free cash flow margins: 32%

- Net cash: $1.1 billion

This post is only for subscribers on the

Premium and Supporter tiers

Subscribe to continue reading