Premium and Platinum tiers

A new position: my asymmetric bet on edge data center energy

I recently started this position to get more exposure to the energy sector, particularly around the AI scale out. I landed on this business because it is very under the radar, fundamentally strong, and has a potential AI data center deal in the making that is not yet reflected in the stock.

Introduction

Over the past month, I have been looking to increase my exposure to the energy sector. Why? It is quickly becoming a major constraint, as energy demand is outpacing supply by large margins. The grid simply cannot keep up.

But many energy companies have already re rated accordingly, and I do not want to invest in the obvious names like Bloom Energy, which is trading at a very high multiple. I would rather invest in under the radar businesses with smaller market caps that have more room to run and have not seen the same re rating yet.

That is how I ended up investing in this business:

- Perfectly positioned to land a data center deal soon

- Accelerating revenue growth

- Improving margins

- Free cash flow positive

- Positive net income

- Healthy balance sheet

- Attractive valuation

The asymmetry between the bear case and bull case is meaningful, with downside protection on the low end and multibagger potential on the high end.

It is a very under the radar business that creates on site power solutions and is well positioned for small to mid sized data centers, with a potential 100 MW deal in the pipeline.

Let’s dive in.

The business I am talking about is Capstone Energy+, credits to @Longviewres who shared a very detailed breakdown of the business on X early may. This triggered me to look into the business more deeply and I really liked what I saw.

Aside from the positives, there are a few things to keep in mind:

- It is a micro cap, so expect high volatility. This is not a stock for the faint hearted

- OTCQX listed, so not trading on a major exchange

- Pre data center revenue, so execution is key

If you are in a rush, jump to Section 11 for valuation scenarios and section 12 for the thesis. Otherwise, the full story is worth following.

1 - The problem

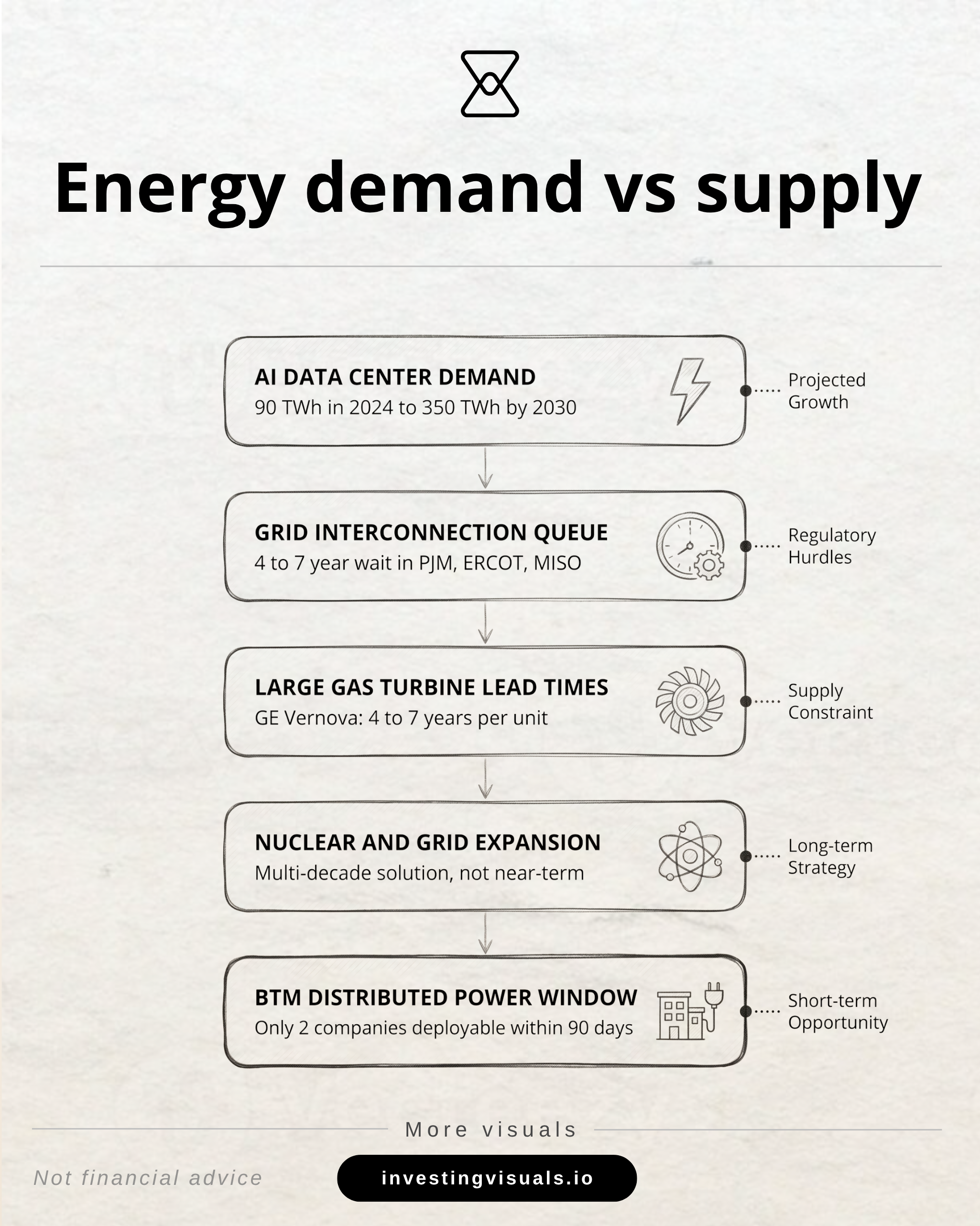

Data center electricity demand surged 17% in 2025, more than five times faster than overall global demand growth of 3%. That is the electricity equivalent of Japan’s entire current consumption. Former Google CEO Eric Schmidt testified before Congress that data centers will need 29 GW of additional power by 2027 and 67 GW more by 2030.

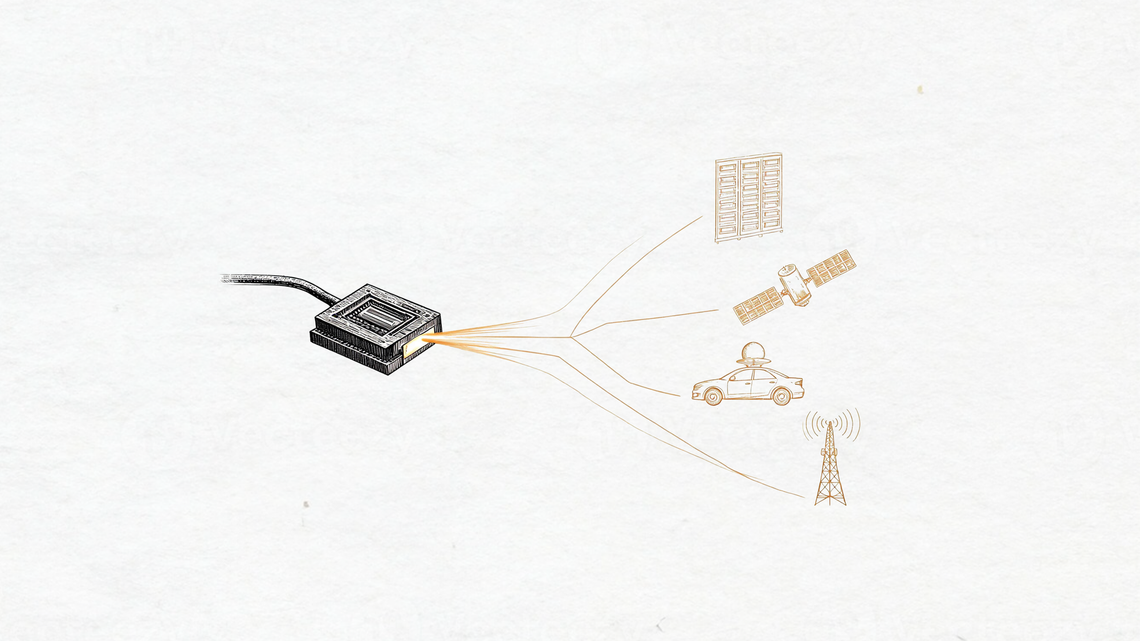

Standard data centers receive electricity from the utility grid through a metering point. Behind the meter (BTM) means generating power on-site, before that meter, so the facility bypasses the grid for some or all of its load. For AI data centers, this means grid interconnection queues in the U.S. now stretch 3 to 7 years, while BTM solutions can be online in months

I like to picture it like a city that triples in population overnight. The roads, the water mains, the power grid, all of it was sized for the old city. The new residents need to move in now, not after a decade of infrastructure expansion.

That is what is happening inside AI infrastructure. The new residents are GPU racks. The road they need most is power. And the fastest way to get it is to stop waiting for the utility and build your own source at the front door. The Nebius + Bloom energy deal is a clear example of that.

Natural gas is the primary "behnd-the-meter" (BTM) fuel, supplying over 40% of U.S. data center electricity as of 2024. 62% of data centers are already exploring BTM solutions, and 19% have begun deploying them.

Microturbines, fuel cells, reciprocating engines, and aeroderivative turbines are all competing for this market. But they differ in scale, lead time, emissions, efficiency, and total cost of ownership.

This is the industry context that CGEH is operating in, in particular the microturbines segment.

2 - From bankruptcy to recapitalization: A corporate timeline

This is crucial context to be aware of: Capstone went through Chapter 11, a legal process that allows a struggling business to stay open and keep operating while it reorganizes its finances.

My first instinct would be to stop here and move on. I do not want to invest in businesses that have shaky balance sheets. But I am glad I did not and spent more time on the actual history, because what I found was the opposite of what I expected.

- 1988, the origin: Two former engineers incorporate NoMac Energy Systems in Tarzana, California, backed by NASA, Ford, and eventually Paul Allen and Bill Gates. The Van Nuys manufacturing base they establish is the same factory running today

- 2000, the IPO: Capstone goes public on NASDAQ. Every major Fortune 100 industrial company with a turbine division tries to compete. Every single one eventually exits the microturbine space. Capstone survives because it was built around this technology

- 2009 to 2021: The first 1 MW system ships, establishing the modular architecture that now underpins an important part of the data center thesis. Over the next decade, more than 10,600 units are deployed across 88 countries, logging 90 million cumulative operating hours

- September 2023, Chapter 11: The company had accumulated over $56M in debt and the balance sheet could not support it. The debt load had become structurally unworkable, ultimately leading to Chapter 11

- March 2026, the Monarch recapitalization: Monarch Alternative Capital leads a $112.5M investment. The Goldman Sachs preferred overhang that had sat on the balance sheet since emergence is fully redeemed in a single transaction. A contractual covenant also triggers, requiring a NASDAQ or NYSE listing no later than March 2027

The Monarch recapitalization is what flipped the script for me. They now have their balance sheet cleaned up - albeit at the cost of significant shareholder dilution - no debt overhang and ready for a new chapter.

However; it's important to spend a bit more time zooming in on what led to the Chapter 11.

3 - Chapter 11: Restructuring details

Darren Jamison, who had served as President and CEO for over a decade, resigned in August 2023, just six weeks before the filing. Robert Flexon, the board chair, stepped in as Interim CEO to run the process.

As said, the company had accumulated over $56M in debt and the balance sheet could not support it. The debt load had become structurally unworkable, and servicing it was consuming the company’s financial flexibility at exactly the moment the market was starting to turn.

What Flexon and the team chose was a prepackaged process, meaning the deal with creditors was negotiated before the petition was ever filed. Goldman Sachs supported that restructuring from day one.

The plan converted most of that $56M in pre petition debt down to approximately $25M at emergence, injected $12M of financing to keep operations running, and preserved the operating business intact.

During this period, the business never stopped operating. They did not sell a single patent, and all product lines were kept operational, with customers continuing to receive orders throughout.

The restructuring was all about the capital structure, not the technology itself. That is an important point to keep in mind for the remainder of this deep dive.

Now fast forward to March 2026, where CGEH receives a $112M investment which in my view significantly changes the capital structure for the better.

4 - Monarch investment

Monarch is a fund that manages $15.8B in assets across credit, real estate, and special situations, so it is not just some random fund stepping in.

The $112M transaction details

The $112M CGEH transaction has three layers:

- First: Monarch invested $95M directly. $80M in Series A at $1,000 per share carrying a 5% annual payment-in-kind dividend and $15M in common stock at $4.50 per share

- Second: a concurrent $17.5M private investment in public equity from accredited investors, including several existing shareholders, also priced at $4.50 per share

- Third (and most importantly for the capital structure): $85M of those proceeds went straight out the door to fully redeem the Goldman Sachs preferred equity sitting in the operating subsidiary.

The investment caused the operating subsidiary to now be wholly owned by CGEH for the first time, meaning they now have full strategic control over it.

The Series A preferred stock Monarch holds is essentially a loan that converts into regular shares later. The conversion price is set at $5.00 per share, meaning every $5.00 of preferred value becomes one new common share. If the stock ever trades above $15.00 for a sustained period, that conversion happens automatically.

While Monarch waits, the 5% payment in kind dividend keeps running. Instead of receiving cash dividends, Monarch receives additional preferred shares every year. Those extra shares will also convert to common eventually.

Details on the 5% payment-in-kind

The 5% payment keeps running until the Series A preferred shares are converted into common stock. That can happen one of three ways:

1. Mandatory conversion. If the stock trades above $15.00 per share for a sustained period (the exact threshold is defined in the certificate of designation filed with the 8-K), conversion is automatic

2. Voluntary conversion by Monarch. Monarch can choose to convert at any time at $5.00 per share. They would likely do this if the stock is trading well above $5.00 and they prefer to hold liquid common shares rather than accruing more preferred.

3. Redemption. If CGEH redeems the preferred in cash rather than converting it, the PIK stops at the point of redemption.

Key takeaways

- The overhang is gone: Goldman Sachs is fully bought out and CGEH owns its operating subsidiary outright for the first time. The structural problem that followed the company out of Chapter 11 is resolved

- The NASDAQ listing is contractually required: A covenant with a hard March 2027 deadline and financial penalties if missed. That uplisting opens the door to institutional capital that currently cannot own an OTCQX-listed company

- Use 50M shares, not 35M: this fully diluted share count already reflects Monarch's preferred converting to common. It's this share count I will also use in the bear, base and bull case in the valuation section

- The balance sheet is clean: $112.5M in capital replaced a structurally unworkable debt load. The company now has runway to pursue the data center pivot without financial distress hanging over every decision

- Monarch is aligned, not passive: Two board seats and a 42.1% as-converted stake means the largest shareholder has direct governance influence

I've spend significantly more time on the company history and capital structure then I normally would because I believe it's crucial context to be familiar with before you consider investing in this business.

It shows the path they took to get them where they are today. So let's move forward from here and look at what their management team currently looks like.

5 - Management

Broadly looking at management, most of the key members were appointed early 2025. I think the knife cuts both ways here.

- Pro: it is a deliberate rebuild of the leadership team following Chapter 11, which I like. None of the management team responsible for Chapter 11 are around; they have all been replaced

- Con: there is limited track record and management still has to prove they are up to the task, introducing execution uncertainty. However, the early results are promising, with accelerating revenue growth and improving margins.

Overall, the management team brings a lot of industry expertise to the table, with all the pieces in place. I would like to highlight the CEO, CFO, and VP of engineering in particular because these are, in my view, the most important positions within CGEH.

Vince Canino, President and CEO: President and CEO, sold high efficiency chiller systems to hyperscalers at Trane Technologies and Smardt Chiller Group before joining Capstone.

I believe it is exactly this commercial experience that CGEH now needs to sign potential data center customers and bring this business into its next phase. Canino seems like the right person in the right place for that. His industry expertise gives deep insight into what buyers value, who makes the decisions, and what the contract structure should look like.

John Miller, Interim CFO: Miller is serving as Interim CFO after John Juric resigned in November 2025 due to a strategic disagreement. Juric objected to the board considering financing alternatives that would dilute common shareholders. Ironically, this is exactly what happened with the Monarch recapitalization.

Having an interim CFO is not ideal heading into a potential NASDAQ listing. Institutional investors conducting diligence for a small cap uplisting want a seasoned CFO who has run that process before. Filling that seat is one of the key near term things I will be watching.

Victor Kong, Vice President of Engineering and Technology: In his role, Victor Kong is responsible for shaping Capstone’s engineering and technology activities. He has been part of the Capstone team since 2005, holding roles of increasing responsibility from Development Test to Core Engineering and Compliance.

6 - Data Center: scalability, target customers, and time to market

On the Q2 FY2026 call, Canino noted:

"We are collaborating with several of these companies to co-develop an on-site power-to-chip strategy, a solution designed to meet the evolving demands of AI factories and next-generation data centers".

He also described the data center pipeline as "magnitudes, magnitudes above" the traditional pipeline, and when asked whether the company could see its first data center orders in the next two quarters, responded: "Well, I sure hope so. Yes, there's some good deals out there".

It's clear Capstone has some significant data center deals in the works which could be disclosed in the upcoming quarters. But which market do they actually go for?

6.1 The type of data centers CGEH pursues

I think a lot of commentary on CGEH conflates “data center market” with “hyperscaler market.” These are not the same thing, and getting this wrong changes the deal probability analysis entirely.

Hyperscale facilities, owned and operated by the largest cloud providers, typically draw 20 MW to over 100 MW each and are being built at campus level, exceeding 500 MW to 1 GW. Bloom Energy’s Oracle Project Jupiter deal at 2.45 GW is a clear hyperscale reference point here. Capstone is not trying to compete at hyperscale level, but on edge data centers.

Edge data centers, typically 1 to 10 MW, are the fastest growing segment. They sit close to data consumers, require power that can be installed quickly in distributed locations, and often lack utility grade grid access.

A single C1000S handles 1 MW. Ten units handle 10 MW. This is Capstone's most natural starting point.

Colocation facilities in the 10 to 50 MW range are the middle market opportunity. These operators need power quickly, face the same grid constraints as hyperscalers, and are often the first movers in BTM deployment because the return on BTM investment becomes compelling at this scale.

In my view, CGEH’s realistic near term target is the 10 to 100 MW segment:

- Colocation operators

- Enterprise data center campuses

- Edge AI infrastructure run by companies that do not have the procurement infrastructure of AWS or Microsoft but face identical power constraints

The 100 MW reference case in CGEH’s investor materials sits at the upper end of this range, with the $350M equipment revenue figure anchored there. A signed deal in the 10 to 25 MW range, while smaller, would still be a real proof of concept. And right now, the market is pricing in zero data center deal of any kind.

6.2 How fast can they scale and deploy

I believe it is not an if, but a when before we get a data center deal announced. This is where scaling and deployment become important.

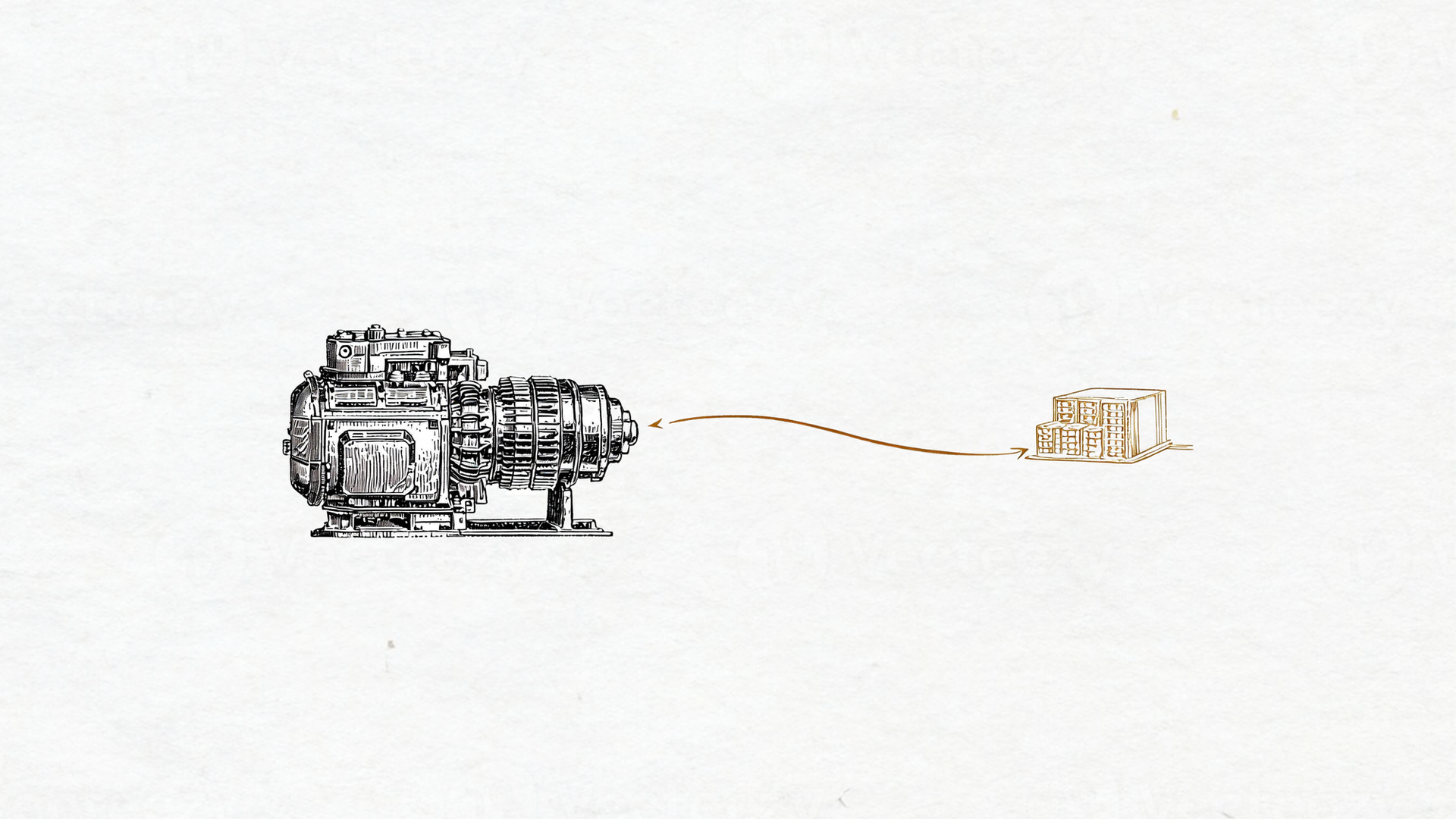

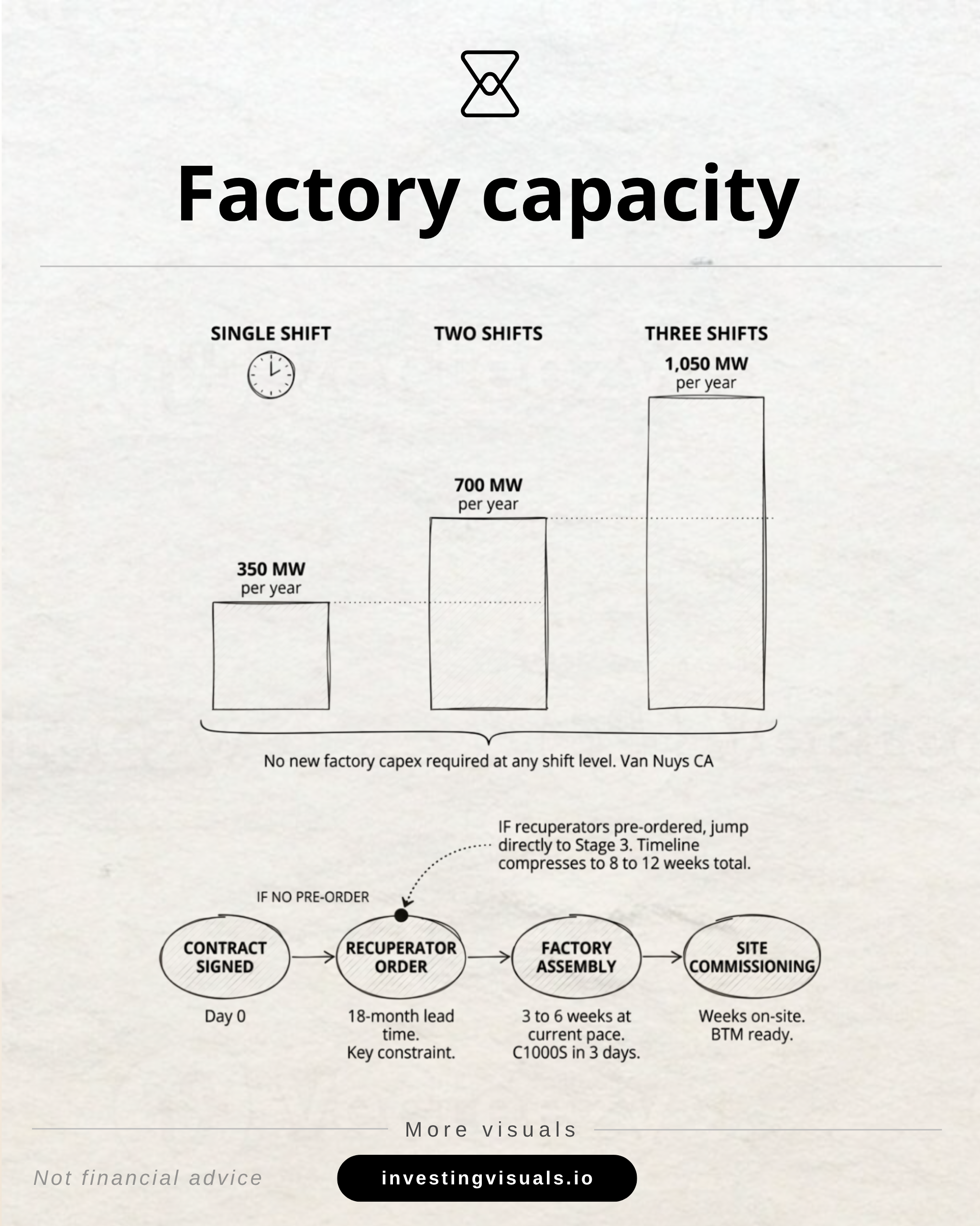

At the unit level, each C1000S ships in a container sized enclosure. A 100 MW order requires 100 units. The Van Nuys factory can produce:

- 350 MW per year on a single shift

- 700 MW per year on two shifts

- 1,050 MW per year on three shifts

With no new building and no new capital expenditure required. At single shift capacity, a 100 MW order could be fulfilled in approximately 3 to 3.5 months of production. On two shifts, about 6 weeks. The factory is not the constraint, the recuperator is.

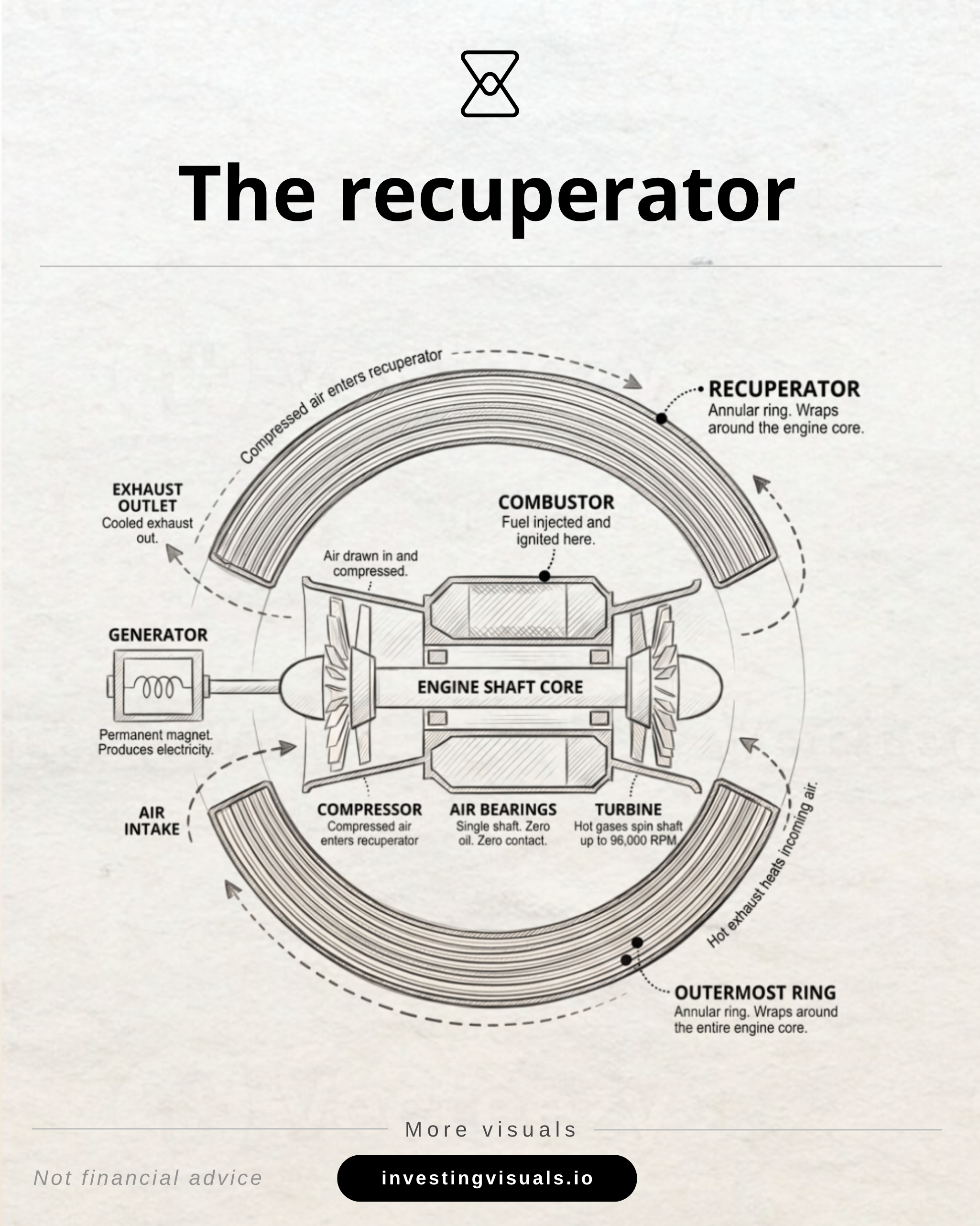

It is a compact heat exchanger that preheats compressed combustion air using exhaust heat, and it has an approximately 18 month manufacturing lead time because it requires precision metalwork from a small number of qualified suppliers.

Management has already conducted dry run sessions with key recuperator suppliers to model supply chain implications of a 100 MW rapid ramp scenario, identifying specific choke points.

But the dry runs do not resolve the problem without a financial commitment. The difficult part here is that pre ordering recuperator inventory before a contract is signed is a capital allocation decision that exposes working capital to a deal that might not close.

The operational implication: from signed contract to first shipment on a large order is likely 18 to 24 months without pre positioned inventory, or as little as 8 to 12 weeks if Capstone has already started pre ordering.

The fact that management is running dry runs suggests they believe a contract is coming. I would not be surprised if they are already pre positioning some inventory by now, given the importance of time to power. But that is a read between the lines interpretation, not a confirmed fact.

Let's have a closer look at what the time-to-market looks like compared to their competitors, which in my view is a crucial factor when a data center needs power as soon as possible.

6.3 Competitor time-to-market comparison

In my view, time to power is the single most important competitive variable in this market right now. Not cost, not efficiency, but speed. Every month of delayed AI compute capacity has a real economic cost for the customer.

This post is only for subscribers on the

Premium and Platinum tiers

Subscribe to continue reading

Written by