members only

2026: The comeback of software stocks?

Software stocks got crushed in 2025 while the NASDAQ kept climbing. 2026 might be the turnaround year, but who are set to benefit most?

As someone who has been investing in software companies for many years and closely tracks the software sector, I’ve seen an interesting dynamic unfold over the past year, especially in the second half of 2025: a major disconnect between the performance of indexes such as the S&P 500 and NASDAQ versus software stocks.

In this article I will cover:

- What caused this disconnect

- What it means for 2026

- The best positioned software businesses for 2026

- What I personally will be doing with respect to my portfolio

Let’s kick off with some context as to what’s going on right now. For the better part of 2025, software stocks have been under pressure across the board. Enterprise software, consumer facing software, large caps, mid cap and small caps alike.

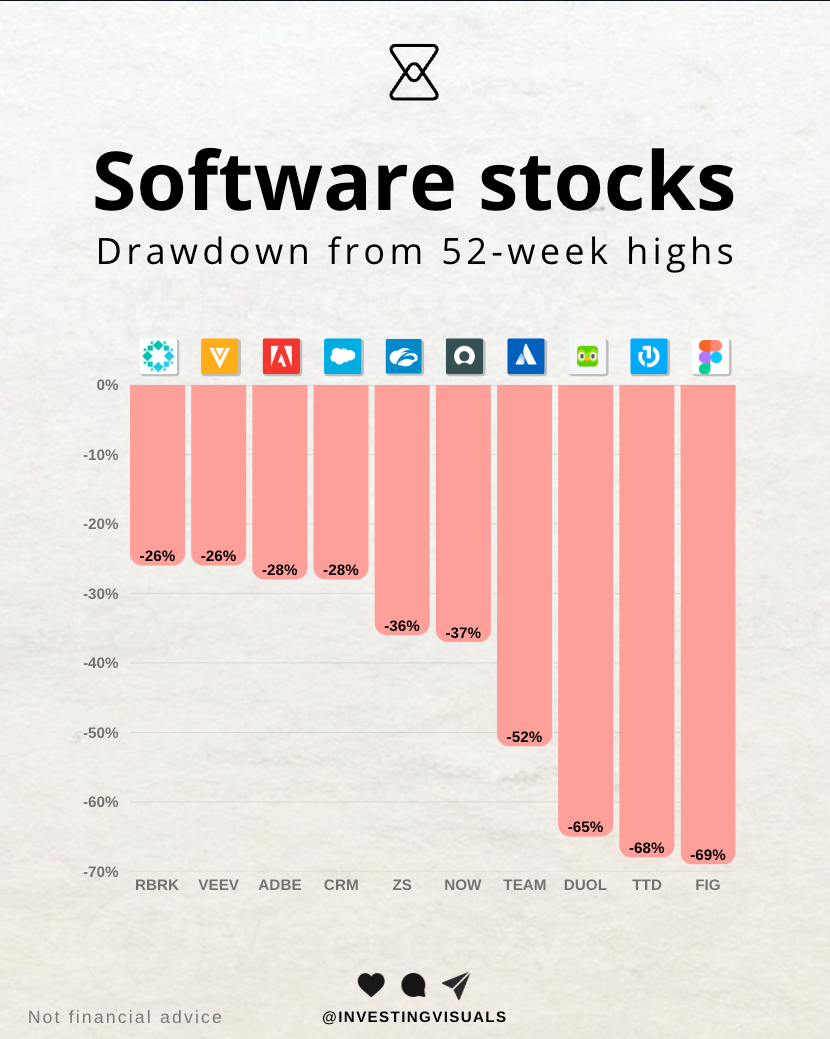

To give you an idea, this is what the current drawdown of many software names looks like:

The contrast gets even bigger when comparing it to the 52 week performance of the tech heavy NASDAQ, which is up 18% over that same period. Meaning names like Figma, The Trade Desk and Duolingo have underperformed the market by 87%, 86% and 83% respectively.

1 - What caused this drawdown?

When I step back and cross check my own experience with what research firms, CIO level reporting, and market commentary share about this, the selloff comes down to three drivers. They reinforced each other, which is why the selloff has been so brutal.

1.1 - Uncertainty around interest rates

The stock market is forward looking, and the same goes for SaaS (software as a service) businesses, with cash flows that generally sit further out in the future. That works beautifully when long term yields drift lower and investors feel good about paying up for future cash flows. But in 2025, that tailwind was unreliable. Higher long term yields were repeatedly flagged as a headwind for equities and for longer duration segments in particular.

The opposite was true back in 2021 to 2022, which was the other end of the spectrum. Many software names reached parabolic heights when interest rates dropped to a multi year low, combined with extra software spend during the COVID period.

As rates went back up in 2023, software names sold off hard again, erasing many of the gains they made during the 2021 to 2022 craze. In the years after, the sector had a great run up until 2025.

2.2 - Consolidation mode

CIOs were dealing with meaningful SaaS price increases, especially on mission critical categories. CIO.com described how SaaS price hikes put budgets in a bind and tied it directly to vendor consolidation and shifting pricing approaches.

InformationWeek referenced survey data showing rising enterprise software costs and highlighted tool sprawl as a core issue buyers were trying to fix.

Similarly, Gartner flagged that CIOs were focusing budget increases on price hikes in recurrent spending, which implicitly leaves less room for net new projects and add ons.

With the rise of AI, there is also less room for so called point solutions 1 in favor of platforms 2. From what I have experienced, this is a dynamic that has been going on for several years now, and AI accelerated that process. Businesses prefer bundled capabilities instead of a fragmented software landscape. Names like Monday and Asana fit into this category and are now down around 50% as consolidation pressures them.

💡

1 A point solution is usually focused on a single use case or workflow. Like a standalone tool for email security, contract signing, employee surveys, or monitoring one part of your systems.

💡

2 A platform bundles multiple related capabilities into one broader product suite, so customers can cover more needs with fewer vendors.

3.3 - AI spending: Infrastructure over software

2025 was an AI year, but not all layers of the stack were treated equally. The market rewarded the parts that captured dollars first. Data centers, compute and infrastructure. With stocks like Nebius, Iren, AMD and NVIDIA leading because that is where the real revenue growth was visible.

Gartner’s 2025 forecasts highlighted that IT spending growth was being led by AI infrastructure, and also pointed to an uncertainty driven pause on some new software initiatives.

Morningstar captured the equity market version of the same story, arguing that software stocks lagged AI linked areas for much of 2025 and were being treated like the wrong part of the trade.

Then you have a second order fear. Not just "when do software companies monetize AI", but "does AI change the economics of certain software categories". Jefferies commentary reported in Barron’s reflected that negative sentiment around application software and pointed to how small AI revenue still was for some companies relative to expectations.

In 2025, the market rewarded those where revenue growth was visible, at the expense of those where there was less visibility or a clear signal that AI can or will boost revenue. This is a very important point, because it is only part of the puzzle and misses some crucial context, which is especially important for 2026 and beyond. More on that in the next chapter.

Bottom line

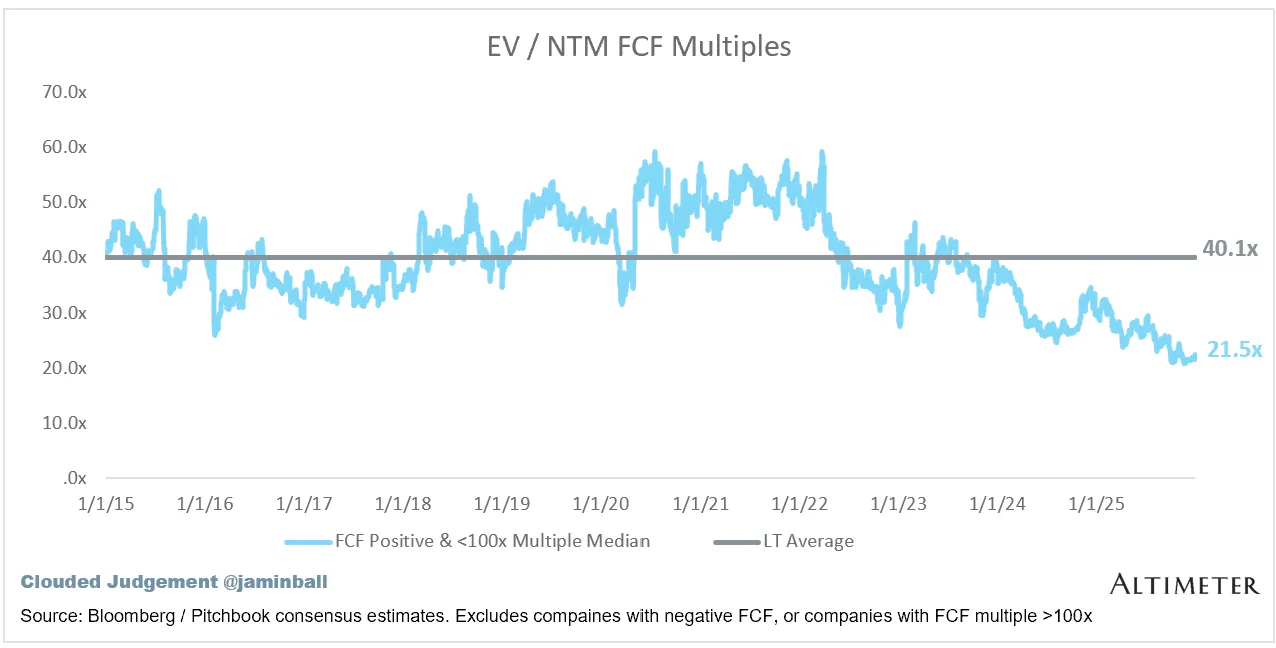

When combining these three forces, this selloff in the software sector makes sense: an unfavorable rates environment, sector consolidation and infrastructure spend being prioritized. Fundamentals stayed strong across the year for most platform names, but this mix caused multiples to compress significantly, as shown in the visual below.

2 - What this means for 2026

For many software businesses, 2025 was a year of experimenting, building and verifying product market fit for their AI powered solutions. I think 2026 could be the year where the hard work done in 2025 starts to translate into meaningful new revenue streams for software businesses, in particular software platforms.

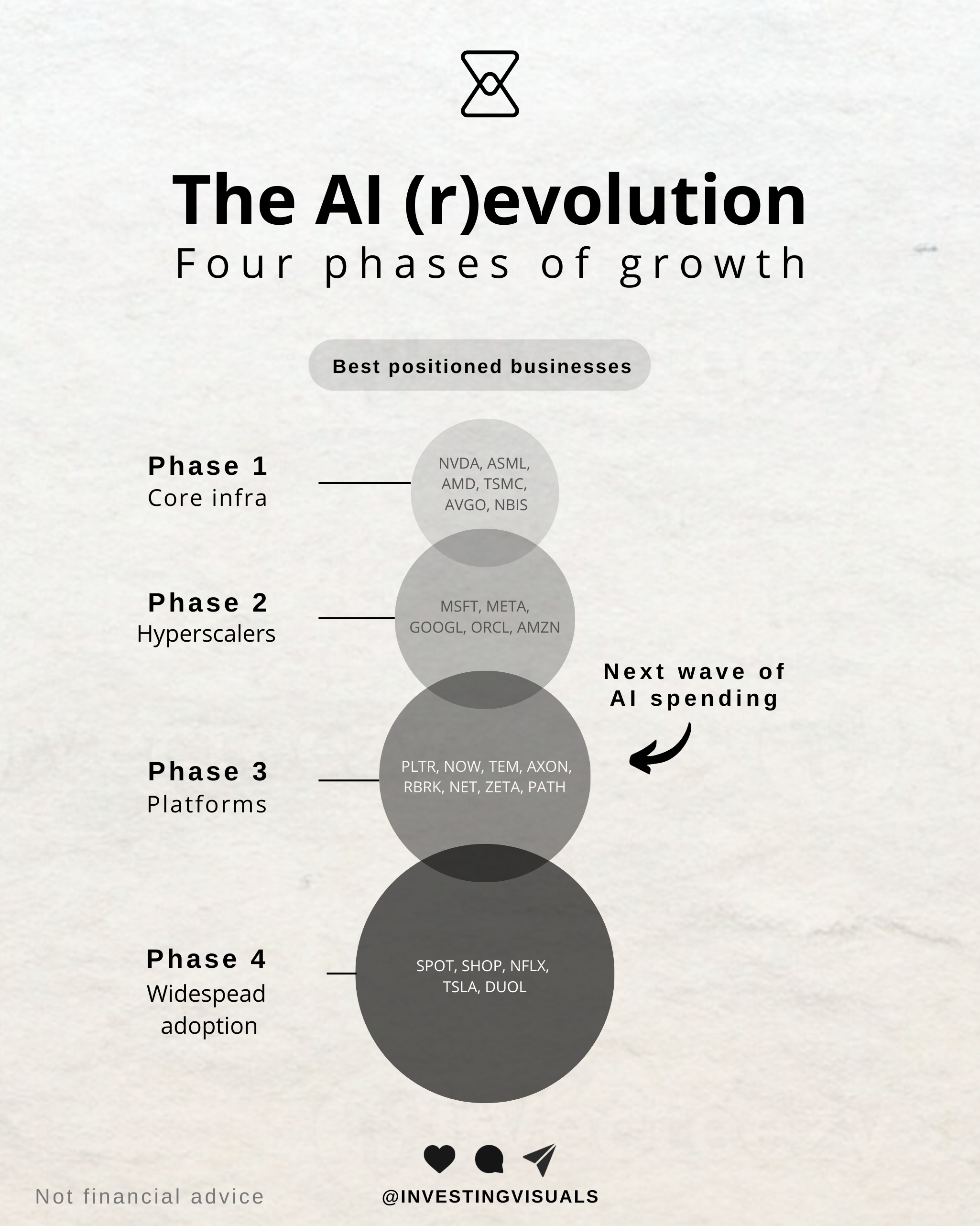

When looking at AI, I like to think of it as four phases of growth:

- Phase 1 - Core infrastructure: the businesses that win here sell the underlying AI infrastructure stack and benefit directly from rising capacity and efficiency demands

- Phase 2 - Hyperscalers: those who productize that infrastructure into easy to consume services, so companies can build and deploy AI without stitching everything together from scratch

- Phase 3 - Platforms: where AI gets embedded into real workflows, focused on outcomes. Meaning time saved, better decisions, fewer incidents and higher conversion, leading to new revenue streams

- Phase 4 - Widespread adoption: finally, the biggest value is concentrated in applications that package AI into products people use every day, often with proprietary data, strong distribution, and clear willingness to pay. This layer can scale fastest once the lower layers are mature enough.

Looking back, 2022 until today has been all about the AI infrastructure buildout. At some point in time, this buildout will mature. I believe that gradually, dollars previously spent on infrastructure will move to the platform layer. I do not think it is an either or situation, but rather a shift in focus.

2026 might be the year where we will see that shift gain more traction, with foundational platforms 3 being the main beneficiaries. For many software businesses, 2025 was a year of experimenting, building and verifying product market fit for their AI powered solutions.

As these solutions get more traction, they can translate into meaningful new revenue streams, which can be a strong catalyst for a rerating of the software sector as a whole.

💡

3 Foundational platforms are those that are mission critical for other businesses. In such a way that these businesses would be seriously impacted if that platform would suddenly be shut down.

3 - Best positioned businesses for 2026

I don't think all software businesses will benefit equally when there is a rerating. So let’s have a look at the top 5 businesses who I believe are best positioned to benefit disproportionately and move on to what I'll be doing heading into 2026.

#5 - Zeta: The operating system of marketing

Zeta is built for Phase 3 because it sits directly inside the day to day workflow of marketing teams, using proprietary consumer signals and an AI powered platform to automate targeting, personalization, and omnichannel activation at scale.

It also benefits from Phase 4 dynamics because those workflows ultimately translate into better consumer facing experiences and measurable outcomes across channels, which is exactly where AI driven personalization tends to shine.

This post is only for subscribers on the

Premium and Supporter tiers

Subscribe to continue reading

Written by